For more than a decade the standard piece of UK retirement tax advice was "spend ISAs first, leave the pension untouched". The reason was simple: a defined contribution pension passed outside the estate for inheritance tax, so on death an unused pot could go to children or grandchildren without the 40% IHT charge that hit the rest of the estate. That logic ends on 6 April 2027. From that date, unused DC pension funds and most lump-sum death benefits payable from a registered pension scheme become part of the deceased's estate for IHT - taxable at up to 40% above the available nil-rate bands.

The change was announced by the Chancellor in the Autumn Budget 2024 on 30 October 2024, consulted on through to January 2025, and confirmed in HMRC's consultation response of 21 July 2025. Draft legislation is in Finance Bill 2025-26. Office for Budget Responsibility costings put the gross receipts from the measure at £1.5 billion a year by 2029/30 - the single largest inheritance-tax-base-broadening measure in modern UK fiscal history. This guide is the most detailed UK-only answer on the open web, with the actual maths.

The rules in force until 5 April 2027

Under the rules in place since pension freedoms in April 2015, defined contribution pensions - SIPPs, personal pensions, workplace DC schemes - sit outside your estate for inheritance tax purposes. The reason is technical but important: most modern DC schemes are written on discretionary trusts where the scheme trustees, not the deceased, decide who receives the money. Because the member never "owned" the funds in a way that put them in the estate, inheritance tax never bit. The expression of wish form simply guides trustees toward the intended beneficiary.

The current tax treatment for beneficiaries then depends on the member's age at death:

- Death before age 75: beneficiaries inherit the pot free of income tax and free of IHT, provided the funds are designated within two years. They can take it as a lump sum, draw an income, or buy an annuity - none of it taxable.

- Death at or after age 75: the pot remains outside the estate for IHT, but beneficiaries pay income tax at their own marginal rate on any income or lump sum they withdraw. There is no IHT, but every pound that comes out is taxable as income to the person receiving it.

The asymmetry mattered enormously for higher-net-worth retirees. A pre-75 death could pass hundreds of thousands of pounds to a non-spouse beneficiary with zero tax - a treatment more generous than almost any other UK asset class. Many people structured their drawdown specifically around it: spend ISAs and savings first, leave the pension untouched as the "IHT-free legacy pot". From 6 April 2027 that strategy stops working.

What changes on 6 April 2027

For deaths on or after 6 April 2027, the value of unused DC pension funds and most lump-sum death benefits payable from a registered pension scheme is added to the deceased's estate for inheritance tax. The 40% IHT rate then applies to the total estate above the available nil-rate bands. Three points are worth pinning down:

- What's in scope: unused DC pension funds (SIPPs, personal pensions, workplace DC schemes) and lump-sum death benefits paid from a registered pension scheme. Drawdown funds not yet drawn are in scope. Annuities already in payment (which die with the holder or pay a survivor's income) generally are not.

- What's exempt: transfers to a surviving spouse or civil partner remain fully exempt under the existing spousal exemption. Bequests to registered UK charities remain exempt. Death-in-service benefits paid from a registered pension scheme are excluded from the estate - a change HMRC made in the July 2025 response after pushback in the consultation.

- Who reports and pays: personal representatives, not pension scheme administrators. PRs calculate the IHT due, report it on the IHT400 series of forms, and settle the bill - pension administrators must provide the value of in-scope benefits within four weeks of being notified of the death. PRs can direct the scheme to pay the IHT directly from the pension before passing the residue to beneficiaries.

The income-tax treatment for beneficiaries (pre-75 tax-free, post-75 marginal rate) is being retained in the July 2025 response. That creates a "double charge" on post-75 deaths from April 2027: the pot is hit by IHT at up to 40% before reaching the beneficiary, then any income or lump sum drawn from what remains is taxed at the beneficiary's marginal rate. HMRC has introduced an income-tax credit mechanism to prevent a literal triple-tax outcome on certain paths, but on the headline numbers a higher-rate beneficiary inheriting a post-75 pension can see an effective combined tax rate approaching 64% on the slice above the available nil-rate bands.

Nil-rate bands and exemptions you can still use

Inheritance tax is charged at 40% on the value of your estate above the available allowances. Three allowances do the heavy lifting for most retirees:

- Nil-rate band (NRB): £325,000. Frozen at this level since 2009 and now frozen again until April 2030 under the post-Autumn-Budget-2024 settlement. Available to every individual.

- Residence nil-rate band (RNRB): £175,000. An additional allowance available when you leave your main residence (or proceeds thereof) to direct descendants - children, grandchildren, step-children. Frozen until April 2030. Tapers by £1 for every £2 of estate above £2 million, so a £2.35m estate has no RNRB at all.

- Spousal exemption: unlimited. Transfers between spouses or civil partners are free of IHT, in any amount. Unused NRB and RNRB also transfer to the surviving spouse, so on second death a couple can have up to £1,000,000 of allowances against the joint estate.

On top of these there are the lifetime gifting allowances that still apply: £3,000 a year annual exempt amount (can carry forward one year if unused); £250 small gift exemption per recipient per year (unlimited recipients); wedding gifts of £5,000 to a child, £2,500 to a grandchild or £1,000 to anyone else; normal expenditure out of income (regular gifts paid from surplus income that do not affect your standard of living are immediately exempt); and potentially exempt transfers - any larger gift that becomes fully exempt seven years after the date of the gift, with taper relief on the IHT charge between three and seven years.

How will the April 2027 change affect you?

- 1 Total estate (incl. DC pension) below the £500k single allowance / £1m married allowance→ Probably no IHT to pay, even after April 2027. The pension joining the estate matters administratively, but no tax is due. Most UK estates fall in this band.

- 2 Married or civil-partnered, leaving everything to spouse on first death→ No IHT on the first death - spousal exemption is unchanged. The planning conversation is about the second death, when the combined estate falls to children. Joint allowances of up to £1m help.

- 3 Single, no children, pot above £325k with no qualifying residence→ You only get the £325k NRB (no RNRB without direct descendants). Likely meaningful IHT on the excess from April 2027 - plan now.

- 4 Couple, both pension pots above £500k each, plus a property→ Joint estate likely £1.5m+. After £1m of allowances, the excess attracts 40% IHT on second death. Drawdown strategies, gifting, charity bequests and possibly trust planning all worth modelling.

- 5 Estate above £2m→ The £175k RNRB tapers away by £1 per £2 above £2m - gone entirely at £2.35m. Combined IHT exposure becomes material. Specialist estate-planning advice is usually well worth the fee at this scale.

Pre- vs post-2027: side by side

The simplest way to see the change is to compare three pathways: a death before 75 under the current rules, a death at 75+ under the current rules, and a death at any age from April 2027 under the new rules.

| Treatment | Death before 75 (pre-April 2027) | Death at 75+ (pre-April 2027) | Death at any age (from 6 April 2027) |

|---|---|---|---|

| Tax on inheritance | No income tax, no IHT - fully tax-free | No IHT; beneficiaries pay marginal income tax on withdrawals | IHT at 40% above NRBs; income tax also still applies to beneficiaries on post-75 deaths |

| Probate process | Bypassed - paid via expression of wish to scheme trustees | Bypassed - paid via expression of wish to scheme trustees | Pension reported on IHT400; personal representatives liable for reporting and paying |

| Spousal exemption | Not relevant - pension outside estate | Not relevant - pension outside estate | Yes - full unlimited transfer to spouse or civil partner |

| Beneficiary's pension | Can keep funds in a beneficiary's drawdown - tax-free withdrawals | Beneficiary's drawdown - withdrawals taxed at their marginal rate | Same operationally; IHT taken from the pot before transfer to beneficiary |

| Death-in-service lump sum | Outside estate, tax-free | Outside estate | Excluded from estate (confirmed in HMRC July 2025 response) |

A worked example, step by step

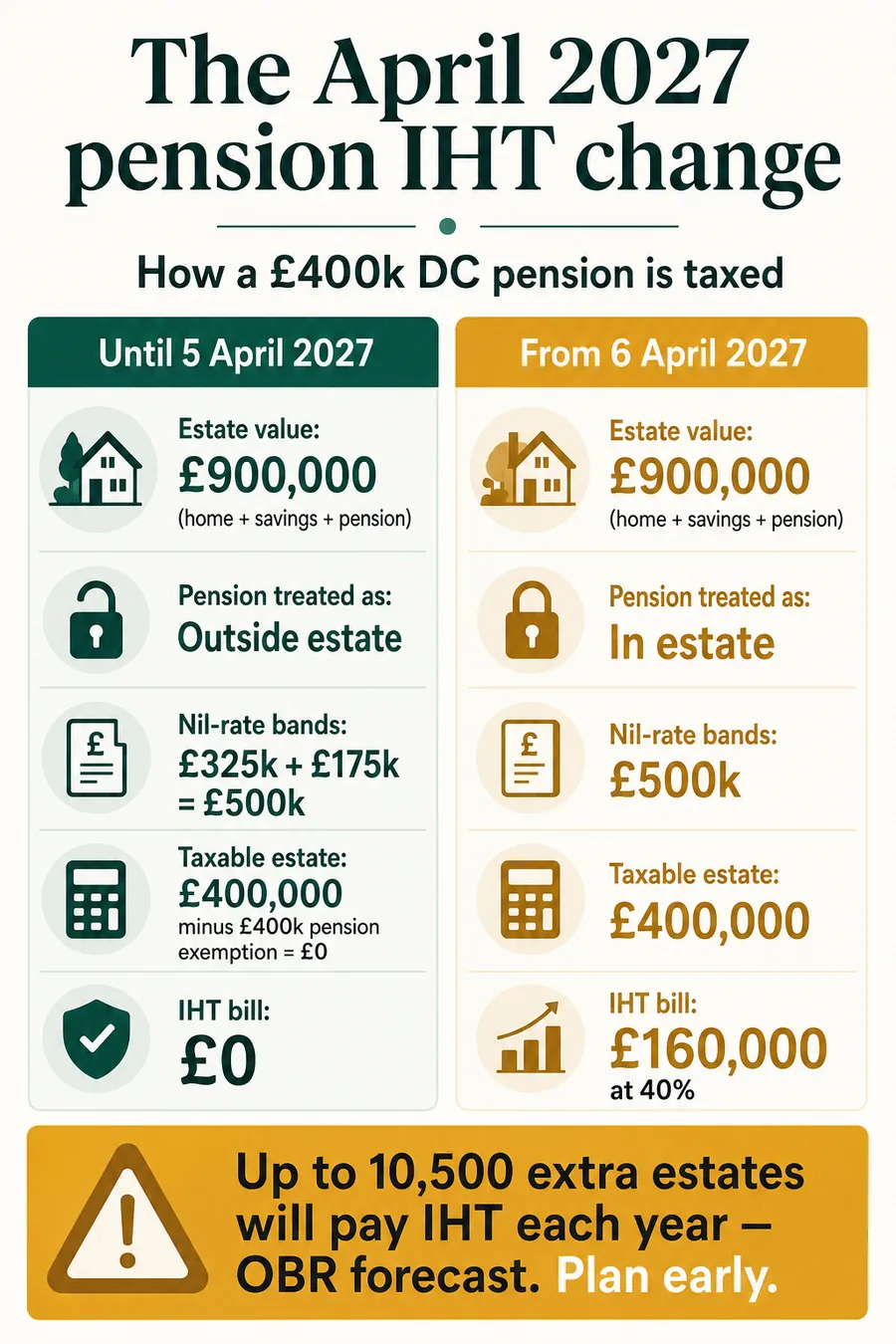

Take a single homeowner with a typical asset mix: a £450,000 home, £50,000 in cash and ISAs, and a £400,000 DC pension pot. Total wealth on paper: £900,000. Here is how the inheritance tax bill looks before and after 6 April 2027.

- Home: £450,000

- DC pension pot: £400,000

- Savings & ISAs: £50,000

- Total wealth: £900,000

- NRB: £325,000

- RNRB (home to direct descendants): £175,000

- Total: £500,000

- Estate for IHT: £500,000 (pension excluded)

- Taxable above £500,000: £0

- IHT due: £0

- Estate for IHT: £900,000 (pension included)

- Taxable above £500,000: £400,000

- IHT due: £160,000

The same person - same house, same savings, same pension - goes from a £0 inheritance tax bill to £160,000 simply because the death falls on or after 6 April 2027 rather than before. The pension, previously outside the estate, is now the thing tipping it over the allowances.

Your post-2027 IHT bill - inline calculator

Plug your own numbers in. The calculator compares the inheritance tax bill on the current rules (DC pension outside estate) with the inheritance tax bill from 6 April 2027 (DC pension included). It uses 2026/27 allowances: £325,000 NRB plus £175,000 RNRB per person, doubled for a married couple inheriting unused bands on second death.

Main residence

Savings, ISAs, investments

SIPPs, personal & workplace DC

Doubles allowances on 2nd death

£160,000 more inheritance tax - driven entirely by the DC pension being pulled into the estate.

Calculation uses 2026/27 nil-rate bands (£325,000 NRB + £175,000 RNRB per person, both frozen until April 2030). Assumes a qualifying residence passed to direct descendants for the RNRB. Married/CP figures assume full transfer of unused NRB and RNRB on second death. Ignores lifetime gifts, business and agricultural relief, and the £2m RNRB taper. Indicative only - get advice for material decisions.

Three named scenarios

Situation: Both retired. Pat has a £350k SIPP from a long professional career. Tom has £250k in a workplace DC scheme. House £700k mortgage-free, £100k of ISAs and cash.

On first death (assume Pat first), everything passes to Tom under the spousal exemption. Pat's nil-rate band and residence nil-rate band transfer to Tom, who now has the full £1,000,000 combined allowance against his estate when he eventually dies.

On second death, the estate is £1,400,000. Tom's allowances cover £1,000,000. The taxable slice is £400,000, taxed at 40% - £160,000 of IHT.

- Pre-April 2027 outcome: the £600k pension sits outside the estate. The remaining £800k of house and savings is below the £1m joint allowance, so IHT is £0.

- Post-April 2027 outcome: the £600k pension is included. Taxable estate £400k × 40% = £160,000.

Closer to £180k once you add some unmodelled drift in the property value. Sensible moves for Pat & Tom: increase their drawdown to spend pensions first, gift the £3,000 annual exempt amount each (so £6,000/year combined), consider a 10% charity bequest on the second death to drop the IHT rate on the rest from 40% to 36%, and review the structure with an adviser by mid-2026.

Situation: Widowed five years ago. Left everything to her late husband's children from a previous marriage in her will. Modest discretionary spending; the pension is the legacy.

Margaret has £325k NRB + £175k RNRB = £500k of allowances. Her property and ISAs together are £400k - comfortably under her allowances. Pre-April 2027, IHT is £0: the pension is outside the estate, everything else is below allowances.

Post-April 2027: the pension joins the estate. Total wealth £800k, less £500k allowances = £300k taxable × 40% = £120,000 IHT. The pension she thought she was leaving to her step-children pays £120k of tax before they see it.

Margaret's options are constrained - she does not have a spouse to inherit, and the step-children do not qualify her for additional RNRB transfer. But she can: take her 25% tax-free cash (£100k) and either gift it within the £3k/year annual allowance over a decade, or as a one-off PET that becomes IHT-exempt after seven years; increase her drawdown above the minimum and gift the surplus as "normal expenditure out of income"; and leave a 10% charity bequest to bring the rate on the rest from 40% to 36%.

Situation: Recently retired senior partner. Hates the idea of paying 40% IHT on a pension he never spent.

John is doing the textbook spend-down. He's taking £40,000 a year of taxable drawdown alongside a slice of his tax-free cash, keeping his total income under the £50,270 higher rate threshold. The taxable £40k attracts roughly £5,500 in income tax at 20% - versus 40% IHT if the same pound stayed in the pot until death.

On top of that he uses every gifting allowance available:

- £3,000 annual exempt amount to his daughter each tax year.

- £250 small gift to each of three grandchildren (£750/year).

- £10,000/year as "normal expenditure out of income" - funded by his drawdown surplus, which is immediately exempt from IHT provided it does not affect his standard of living.

- A one-off £100,000 from his tax-free cash as a PET towards a deposit on his daughter's house. Falls fully out of the estate after seven years, with taper relief between three and seven.

Over a decade John can plausibly shift £200,000+ out of his estate within the rules, turning a hypothetical £80,000 IHT liability into a few thousand pounds of basic-rate income tax. The strategy depends on his health (he needs to survive seven years for the PET) and discipline (each gift must be properly documented and consistent with the "normal expenditure" definition). At this scale a regulated adviser typically pays for themselves several times over.

What you can still do - sensible planning moves

- Increase drawdown. Spend the pension first, in your own basic-rate band, rather than leave it to be hit by 40% IHT later. The classic "spend ISAs first, leave the pension" strategy is dead from April 2027 - reverse it.

- Use the £3,000 annual exempt amount every year (carryable one year if unused), plus small gifts of £250 per recipient. A couple is £6,000/year between them, plus an unlimited number of £250 gifts.

- Gift "out of normal expenditure". Regular gifts paid from income surplus to your needs are immediately exempt - no seven-year wait. Document a pattern.

- Make potentially exempt transfers (PETs). Larger lifetime gifts fall fully out of the estate after seven years, with taper relief between three and seven.

- Charity bequest at 10% or more of the net estate brings the IHT rate on the rest from 40% to 36% - and is itself fully exempt. For a £400k taxable estate, the 4% rate cut saves £16,000 of IHT.

- Leave assets to a spouse or civil partner. Unlimited exemption - still the biggest single tool. Plan for the second death, not the first.

- Take more tax-free cash now while it is your choice and the 25% PCLS rule is still in place. Putting it into an ISA does not solve the IHT issue, but it gives you flexibility to gift, spend, or use it for a PET clock-start.

- Spousal bypass trusts. A discretionary trust set up as the death-benefit nominee on a pension is still being used by some advisers in 2026 - but the technical detail post-April 2027 is unsettled and you need specialist advice. Do not DIY this.

What's not changing in April 2027

- The pre-75 income-tax exemption for beneficiaries: if you die before age 75, beneficiaries continue to take pension income or lump sums free of income tax (HMRC confirmed this in the July 2025 response). The IHT layer applies on top from April 2027 - income tax does not.

- The post-75 marginal-rate income-tax treatment: beneficiaries inheriting on a death at 75+ continue to pay income tax at their own marginal rate on what they draw. The pre-75/post-75 split is unchanged for income-tax purposes; the new IHT layer sits on top of both.

- The spousal/civil-partner exemption: unchanged. Full unlimited transfer to a surviving spouse or civil partner, with unused NRB and RNRB transferring for use on the second death.

- The 25% tax-free cash: the Pension Commencement Lump Sum and the £268,275 Lump Sum Allowance regime introduced from 6 April 2024 are unchanged.

- Annuities in payment: a single-life annuity dies with the holder; a joint-life annuity pays the survivor's pension as income. Neither pays a lump sum inheritance, so neither is in scope of the new IHT charge.

- Death-in-service benefits: excluded from the estate after HMRC's July 2025 response.

Defined benefit (final-salary) pensions are different

Most defined benefit schemes pay a survivor's pension to a spouse or dependant - usually 50% or 67% of the member's pension, paid as taxable income for life. Survivor pensions paid as income are not in scope of the new IHT rules. Where a DB scheme also pays a discretionary lump-sum death benefit (typically a multiple of salary on a "death in service" or a return-of-contributions on early death), HMRC's July 2025 response confirmed that genuinely discretionary lump sums from registered pension schemes - and death-in-service lump sums in particular - are excluded from the estate.

If you have a DB pension and you are worried about IHT, the question is usually different: does the survivor's pension cover your spouse's needs? Could you take a DB-to-DC transfer (usually a poor idea at standard transfer values) to gain the flexibility to draw and spend down? In most cases the answer with DB is: do nothing, the new rules don't apply. The change matters far more for DC (SIPP, personal pension, workplace DC) holders.

Avoidance versus evasion - don't get clever

There is a strong temptation, with the change now fully signalled and almost a year away, to "do something dramatic" before 6 April 2027. Don't. Three reasons:

- The seven-year clock starts at the gift, not the change. A large potentially exempt transfer made in March 2027 needs you to live until March 2034 to fall fully out of the estate. Taper relief kicks in between three and seven years; below three years there is no relief, and the gift is fully back in the estate.

- HMRC's General Anti-Abuse Rule (GAAR) and pre-existing anti-fragmentation rules apply to contrived schemes. Anything that looks like the sole purpose was tax avoidance - particularly schemes promoted as a "loophole" - risks being unwound on enquiry, with penalties.

- Stripping out a large pension in 2026/27 creates an income-tax problem now and a deposit-in-the-estate problem later. £200,000 drawn from a pension in a single year is mostly taxed at 40% and 45%; £200,000 sitting in an ISA on death is in your estate, just like the pension would have been from April 2027.

The sensible playbook is gradual, well-documented, advised: use the gifting allowances every year, draw down at a sustainable rate that uses your basic-rate band, document "normal expenditure out of income", and consider a 10% charity bequest. Anything beyond that - bypass trusts, deed-of-variation strategies, business property relief planning - needs a regulated adviser who can take responsibility for the recommendation.

What HM Treasury actually said

From the GOV.UK policy paper "Inheritance Tax on unused pension funds and death benefits", published 21 July 2025:

"As announced at Autumn Budget 2024, the government will bring unused pension funds and death benefits payable from a pension into a person's estate for Inheritance Tax purposes from 6 April 2027. Personal representatives, rather than pension scheme administrators, will be liable for reporting and paying any Inheritance Tax due on unused pension funds and death benefits from 6 April 2027. All death in service benefits payable from a registered pension scheme will be excluded from the value of an individual's estate for Inheritance Tax purposes from 6 April 2027. Most estates will continue to have no Inheritance Tax liability after 6 April 2027."

Office for Budget Responsibility costings (Spring 2025 supplementary release) put exchequer receipts from the change at £0.6bn in 2027/28, £1.1bn in 2028/29, £1.5bn in 2029/30. HMRC estimates an extra 10,500 estates will fall into IHT for the first time as a result, and a further 38,500 estates already paying IHT will face higher bills averaging £34,000. Total IHT receipts in 2024/25 were £8.2 billion; the OBR forecasts £14.5 billion by 2030/31, a 67% rise driven primarily by frozen thresholds and the pensions change.

Related pages on this site

If you arrived here researching a specific pot size, our pot-size pages cover the same IHT change in the context of actual income modelling:

- £500,000 pension pot: how much retirement income in 2026? - modelling for a £500k DC pot, including the April 2027 IHT impact at that scale.

- Tax-free cash and the Lump Sum Allowance - the £268,275 LSA framework you should understand before taking large tax-free chunks pre-2027.

- Emergency tax on pension withdrawals - how to reclaim over-tax on first taxable withdrawals via P55, P53Z and P50Z.

Frequently asked questions

- Are pensions subject to inheritance tax?

- Not at the moment. Until 5 April 2027, unused defined contribution pension funds (and most lump-sum death benefits) generally sit outside your estate for inheritance tax. From 6 April 2027 that changes - unused DC pension funds and most death benefits become part of the deceased's estate for IHT, charged at up to 40% above the £325,000 nil-rate band and £175,000 residence nil-rate band. The change was announced in the Autumn Budget 2024 on 30 October 2024 and confirmed in HMRC's consultation response on 21 July 2025. Defined benefit (final-salary) pensions and death-in-service benefits are not in scope.

- When does the pension IHT change start?

- Deaths on or after 6 April 2027. The Autumn Budget 2024 announced the change; HMRC consulted between October 2024 and January 2025, then published its formal response on 21 July 2025. Legislation is being introduced in Finance Bill 2025-26. HMRC has confirmed that personal representatives (not pension scheme administrators) will be responsible for reporting and paying the IHT, with scheme administrators required to provide the value of in-scope death benefits within four weeks of being notified of the death.

- How much IHT will I pay on my pension from 2027?

- It depends on the size of your total estate, not just the pension. IHT is charged at 40% on the value of the estate above your nil-rate band (£325,000) plus residence nil-rate band (£175,000 if you leave a qualifying home to direct descendants), giving a single homeowner £500,000 of allowances. A married couple can transfer unused bands, giving up to £1 million on second death. As a worked example, a single homeowner with a £450,000 home, £50,000 in savings and a £400,000 DC pension has an estate of £900,000. Pre-April 2027 their IHT bill is zero (the pension is outside the estate and the rest of the estate is covered by allowances). Post-April 2027 the bill is £160,000 - 40% of the £400,000 above the £500,000 allowance.

- Can I avoid IHT on my pension?

- You cannot wholly avoid it without giving up control of the money. But there are sensible planning moves that are clearly within the rules: (1) increase drawdown so the pot is smaller at death - pay your own marginal income tax rate now (likely 20%) instead of 40% IHT later; (2) use the £3,000 annual gift allowance, small gifts of £250 per recipient, and regular gifts out of normal income (not capital); (3) make potentially exempt transfers (PETs) - these fall outside the estate after 7 years; (4) leave at least 10% of your net estate to charity to qualify for the reduced 36% IHT rate on the rest; (5) leave assets to a spouse or civil partner (still fully exempt); (6) consider a spousal bypass trust on the pension (specialist advice required). Do not attempt to outrun the change with aggressive untested schemes - HMRC has anti-avoidance powers under the General Anti-Abuse Rule.

- Does the spousal exemption apply to pensions?

- Yes. Transfers between spouses and civil partners are fully exempt from inheritance tax - including pension death benefits from 6 April 2027. If you leave your DC pension pot to your spouse, there is no IHT charge on the first death. The IHT issue (if any) only arises on the second death, when the combined estate falls to children, grandchildren or other beneficiaries. This is why couples now plan around the second death rather than the first.

- What happens to my pension when I die before 75?

- Under current (pre-April 2027) rules, if you die before age 75 your beneficiaries can inherit your unused DC pension free of both income tax and IHT, provided the funds are designated within two years. They can take it as a lump sum, draw an income, or buy an annuity - all tax-free at that point. From 6 April 2027 the pre-75 income tax exemption is expected to remain in place (HMRC has indicated it will continue), but the unused fund itself will count towards the deceased's estate for IHT. The combination still treats pre-75 deaths more favourably than post-75 deaths, but the IHT layer applies in both cases from 2027.

- What happens to my pension when I die after 75?

- Under current rules, beneficiaries inheriting a DC pension when the holder dies at 75 or older pay income tax at their marginal rate on whatever they withdraw (or on any annuity income). The pot itself is outside the estate for IHT. From 6 April 2027 there is a "double charge": the pot first attracts IHT at up to 40% as part of the estate, then the beneficiaries pay income tax at their marginal rate on what they take out. HMRC has confirmed that an income-tax credit will be available to prevent triple taxation in extreme cases, but the headline effect is that a higher-rate beneficiary inheriting from a post-75 death could see an effective combined tax rate of around 64% on the slice above the nil-rate bands.

- Will my partner pay IHT on my pension in 2027?

- If you are legally married or in a civil partnership, no - the spousal exemption means your partner inherits your pension free of IHT (and the unused nil-rate bands transfer for use on the second death). If you are cohabiting but not married, yes - there is no IHT exemption for unmarried partners, so from 6 April 2027 the pension passes into the estate and is taxable at 40% above the available nil-rate bands. This is one of the strongest financial arguments for couples in long-term cohabitation to consider formalising their relationship before the change takes effect.

- Does the April 2027 change apply to DB pensions?

- Mostly no. Defined benefit (final-salary) schemes typically pay a survivor's pension to a spouse or dependant rather than a transferable lump sum - and survivor pensions paid as income are not in scope of the new IHT rules. Any DB lump-sum death benefit that is genuinely discretionary (i.e. trustees decide who receives it, you cannot direct it) was outside IHT before 2027 and remains outside under the new rules - HMRC confirmed in July 2025 that "death in service" lump sums from registered schemes are excluded. The change primarily affects defined contribution pots (SIPPs, personal pensions, workplace DC schemes) where there is an unused fund at death.

- Should I take my pension out before April 2027?

- For most people, no - at least not in a way that creates a worse problem. Stripping out a large taxable pension in 2026/27 can push you into the higher (40%) or additional (45%) rate of income tax, and parking the proceeds in your estate just moves the money from one IHT-affected pool to another. The smarter strategies are gradual: increase your drawdown rate modestly so the pot is genuinely smaller by 2027 (paying basic rate now beats 40% IHT later); take the 25% tax-free cash and use it strategically (gifts within allowances, charity bequests, paying down a mortgage); and stop making fresh pension contributions once your pot is comfortably above the nil-rate bands. Take advice - at this size of pot the cost of a regulated adviser is recouped many times over.

Allowances quoted are 2026/27 and are frozen at these levels until April 2030 under current policy; a future Budget could move them. The £2m residence nil-rate band taper is not modelled in the inline calculator above - for estates near or above £2m, your effective allowance is lower than shown. The income-tax credit mechanism HMRC has announced to prevent literal triple-taxation on post-75 deaths is still being finalised in detailed regulations; the headline IHT-then-income-tax framework is settled. Anyone making a decision worth more than the cost of an hour with a regulated adviser should pay for one - at the pot sizes this page is aimed at, the value of correct advice is high.

The April 2027 change lands on whoever administers your estate, so it is worth knowing what that job involves. Our probate and estate hub covers valuing an estate for inheritance tax, executor duties and personal liability, and whether a grant of probate is needed at all - plus a probate cost calculator, since percentage-based probate fees on a large estate can cost more than the tax planning saves.