Pension Drawdown & Retirement Income

Since April 2015's pension freedoms ended compulsory annuitisation, turning a defined contribution pot into a retirement income has become the biggest financial decision most UK retirees ever make. This hub covers the rules, the maths and the trade-offs for the 2026/27 tax year - from the 25% tax-free lump sum to today's annuity rates and the safe withdrawal rate.

- 1 I want a guaranteed income for life with no surprises→ An annuity - even a partial annuitisation covering essentials. May 2026 rates are the strongest since 2008. Compare drawdown vs annuity for the trade-offs.

- 2 I want flexibility and the ability to leave money to family→ Flexi-access drawdown - keep the pot invested, withdraw as needed, pass anything left to beneficiaries (tax-free if you die before 75 under current rules).

- 3 I need one-off cash for a specific goal (debt, mortgage, gift)→ Take the 25% Pension Commencement Lump Sum (PCLS) on its own, or use UFPLS to take slices that are 25% tax-free and 75% taxable each time.

- 4 My pot is under £30,000 - or I just want to empty it→ Small-pots rules and trivial commutation may let you take everything in one go without triggering the MPAA. Worth checking before any other route.

- 5 I'm genuinely unsure→ Book a free Pension Wise appointment with MoneyHelper - a 60-minute phone or video call, government-backed, no products sold. The single best £0 you can spend.

What changed in April 2015 - and why it matters now

Before 6 April 2015, almost everyone with a defined contribution pension was effectively pushed into buying an annuity by the age of 75. George Osborne's pension freedoms ripped that out. From 55 (57 from April 2028) you can now access your pot in four very different ways: a 25% tax-free lump sum followed by drawdown; a full or partial annuity purchase; uncrystallised funds pension lump sums (UFPLS), where each withdrawal is 25% tax-free and 75% taxable; or full encashment. Most people end up doing some combination.

A decade on, the FCA's Retirement Income Market Data 2024/25 shows just how dramatic the shift has been. Of 961,575 plans accessed for the first time in 2024/25, 349,992 went into drawdown (up 25.5% on the year), 88,430 into annuities (up 7.8%), and the balance into UFPLS or full encashment. Total withdrawals across the market reached £70.9 billion. Drawdown is now the default - annuities are coming back into fashion as rates climb, but the freedom genie is firmly out of the bottle.

The 25% tax-free element, explained properly

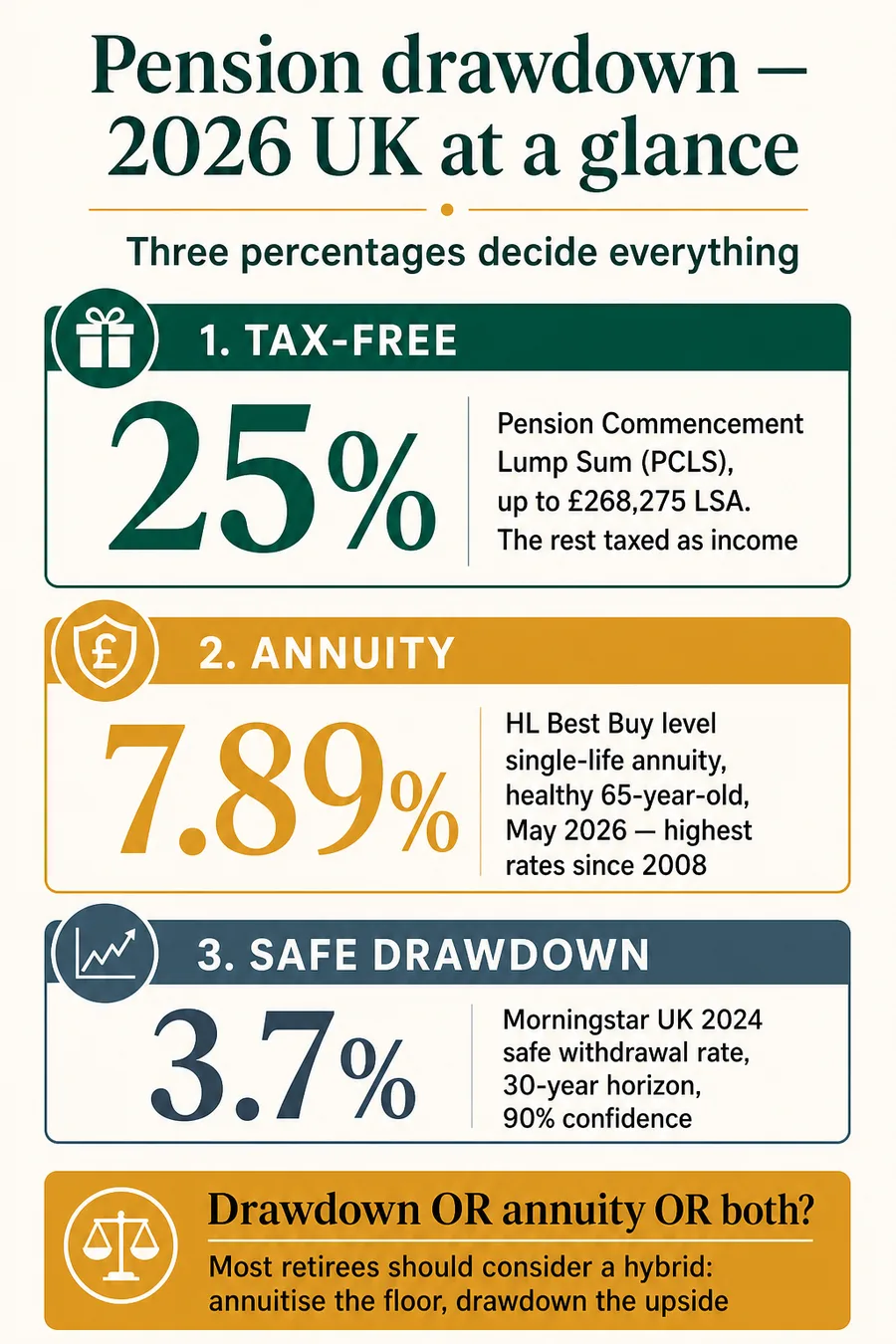

Every defined contribution pension lets you take up to 25% as a tax-free lump sum - formally the Pension Commencement Lump Sum (PCLS). The total is capped across all your pensions by the Lump Sum Allowance of £268,275, in place since April 2024 when it replaced the old Lifetime Allowance. Three different ways to take that 25%:

- PCLS upfront. Take the full 25% in one go at the point you start drawing, with the remaining 75% moving into a drawdown account or buying an annuity. Simple, but you lose tax-sheltered growth on the £25k+ you withdraw.

- Phased PCLS. Crystallise the pot in slices over multiple tax years. Each slice releases its own 25% tax-free, with the remainder going into drawdown. The 75% left inside the pension wrapper keeps growing free of UK income tax and (under current rules) outside your IHT estate.

- UFPLS withdrawals. Each withdrawal is itself 25% tax-free and 75% taxable - effectively a self-mixing cocktail. Useful if you want a steady draw without formally moving into drawdown, but it makes tax forecasting messier.

The default move - take the full £25k upfront because you can - is often the wrong one. The money grows tax-free inside the pension and (today) passes to beneficiaries tax-free on death before 75. Cash sitting in a bank account does neither. See our deeper guide on how much pension you can take tax-free for the worked examples.

Drawdown vs annuity - the trade-off in 2026

For two decades after the 2008 financial crisis, annuity rates were so poor that the choice was almost made for you: drawdown won. That has reversed. The Hargreaves Lansdown best-buy table in May 2026 shows a healthy 65-year-old getting £7,892 a year per £100,000 on a level single-life basis - the strongest rates since 2008. A 70-year-old gets closer to £8,600 a year per £100k. Enhanced annuities (for smokers and qualifying medical conditions) can pay 13-20% more than that.

The trade-off is the same as it has always been, just with different numbers:

- Drawdown keeps you invested, exposes you to sequence-of-returns risk, and gives you a pot to bequeath. Income is not guaranteed; in a bad market run-in you can run out.

- Annuity swaps your pot for a guaranteed lifetime income that cannot run out. You give up flexibility, growth potential and (with a single-life policy) anything left for beneficiaries.

- Hybrid. Annuitise enough to cover essential spending when added to the State Pension; keep the rest in drawdown for discretionary income, growth and legacy. This is the structure most independent retirement specialists now lean toward.

Whatever you do, shop around. The FCA found that 62% of annuities are now bought from a provider other than the consumer's existing pension scheme - the highest share since the data series began. Just Group's analysis suggests a healthy 65-year-old can earn 13% more income by comparing quotes, rising to 20%+ at 75. Read the full drawdown vs annuity comparison.

The sustainable withdrawal rate question

William Bengen's famous 4% rule came from US data in the 1990s: in his model, withdrawing 4% of a balanced US portfolio in year one, then increasing that pound figure with inflation, survived every 30-year retirement window in his backtest. UK retirees are not Americans. Morningstar's UK-specific research for 2024/25 lowered the safe inflation-adjusted starting rate to 3.7% (2024) and 3.9% (2025) for a 30-year retirement at 90% confidence - a meaningful gap that reflects higher UK inflation volatility, lower expected real returns and a different government-bond mix.

The bigger risk than the headline rate is sequence-of-returns risk: two retirees with the same average return over 30 years can end up with wildly different outcomes if one retires into a market crash. Three practical defences are universally accepted. Hold 1-2 years of withdrawals in cash so you never sell fund units at depressed prices. Use a guardrails strategy - cut withdrawals by 10% after a year where the pot falls more than 15%, restore them when it recovers. Annuitise the floor so a market wobble doesn't threaten essentials. Our UK safe withdrawal rate guide has the full Morningstar numbers and the guardrail mechanics.

How drawdown is taxed in 2026/27

The 25% tax-free cash does not use your personal allowance. The other 75% - and every UFPLS withdrawal's taxable portion - counts as income in the tax year you take it, on top of any State Pension, defined benefit pension, earnings and savings interest. With the full new State Pension at £241.30/wk (£12,547.60/year) for 2026/27, just adding £4,000 of drawdown puts you over the £12,570 personal allowance into the 20% basic-rate band. Take a larger lump sum and you can easily spill into 40% higher-rate territory in a single tax year.

Two specific gotchas. HMRC applies an emergency tax code to almost every first taxable pension withdrawal, treating it as if you'll receive it monthly - you reclaim with P55 (pot still open) or P53Z (pot fully emptied). And any taxable drawdown income - even £1 - triggers the Money Purchase Annual Allowance, slashing your future pension contributions from £60,000 to £10,000 a year. The 25% tax-free cash does not trigger the MPAA on its own. Full mechanics in our drawdown tax guide.

The April 2027 inheritance tax change

Under rules in force today, unused defined contribution pensions sit outside your estate for inheritance tax - die before 75 and beneficiaries receive the pot tax-free, die at 75 or later and they pay only income tax at their marginal rate on what they withdraw. That changes from 6 April 2027: most unused DC pensions will be brought inside the IHT estate, meaning estates above the nil-rate band could face a 40% IHT charge on top of the existing income tax due. The Treasury expects this to affect roughly 8% of estates, but for higher-net-worth retirees with substantial DC pots it is one of the largest planning changes in a generation. Our inheritance tax and pensions guide walks through the gifting, life-cover and bypass-trust options being discussed by advisers.

Guides in this section

Six in-depth guides covering pension drawdown & retirement income for the 2026/27 tax year.

- 01 Pension drawdown explained

What flexi-access drawdown is, how it differs from an annuity, the tax rules, and the risks of running your pension pot down too fast.

Read guide → - 02 £100k pension pot: drawdown & annuity income in 2026

What a £100k pension pot buys in 2026: ~£7,891/yr from a level annuity at 65 or ~£4k/yr drawdown, with annuity rate tables and a calculator.

Read guide → - 03 £150,000 pension pot: how much income in 2026?

A £150k pension pot gives ~£6,000/yr drawdown or ~£11,790/yr level annuity at 65, plus the £12,547 State Pension. July 2026 rates, tax and 30-year tables.

Read guide → - 04 £200,000 pension pot: how much income in 2026?

A £200k pot buys ~£8,000/yr drawdown income or ~£15,720/yr level annuity at 65, plus £12,547 State Pension. July 2026 annuity rates, tax and 30-year tables.

Read guide → - 05 £250,000 pension pot: how much income?

How long a £250,000 pension pot might last in drawdown, plus example annuity rates and how the 25% tax-free lump sum changes the maths.

Read guide → - 06 £300,000 pension pot: how much income in 2026?

A £300k pension pot buys ~£23,580/yr from a level annuity at 65 or ~£12,000/yr at 4% drawdown. With the £12,547 State Pension the annuity route tops £36,000.

Read guide → - 07 £500,000 pension pot: how much income?

Worked examples for a £500k pension pot: drawdown income, annuity rates, and the tax you might pay each year.

Read guide → - 08 UK annuity rates July 2026: what £100k buys by age

UK annuity rates July 2026: £100,000 buys a healthy 65-year-old ~£7,860-£7,936 a year for life at best-buy rates. Full tables by age, pot size and health.

Read guide → - 09 Drawdown vs annuity: which is right for you?

A side-by-side comparison of pension drawdown and annuities - flexibility, longevity risk, tax and what happens to your money when you die.

Read guide → - 10 What is a safe withdrawal rate in the UK?

The 4% rule, why UK retirees may need a lower figure, and how sequence-of-returns risk affects how much you can draw each year.

Read guide → - 11 Taking your 25% tax-free pension lump sum

How the pension tax-free cash works, the lump sum allowance, and worked examples of taking it all at once vs in slices.

Read guide →

Frequently asked questions

- What is pension drawdown?

- Pension drawdown - properly called flexi-access drawdown - is the most popular way to turn a defined contribution pension into a retirement income since the 2015 pension freedoms. You keep your pot invested, take 25% as a tax-free lump sum if you want it, and withdraw the rest as taxable income whenever you choose. Unlike an annuity, the money is not converted into a guaranteed income - you bear the investment risk and the longevity risk in exchange for flexibility and the ability to pass any remaining pot on to beneficiaries. In 2024/25 drawdown was used to access 349,992 pension plans, a 25.5% jump year on year, according to FCA Retirement Income Market Data.

- How is pension drawdown taxed?

- The first 25% you take out is tax-free (the pension commencement lump sum, or PCLS), up to a lifetime cap of £268,275 across all your pensions - the Lump Sum Allowance. Everything beyond that is taxed as income in the tax year you withdraw it, on top of your State Pension and any other taxable income. The first £12,570 of total income is covered by the personal allowance, then 20% basic rate, 40% higher rate, 45% additional rate (Scotland's bands differ slightly). HMRC almost always applies an emergency tax code to your first taxable withdrawal - reclaim using form P55 if the pot is not empty, P53Z if it is. Once you take any taxable drawdown income you also trigger the Money Purchase Annual Allowance, which slashes the amount you can contribute to a pension to £10,000 a year.

- What's the safest pension withdrawal rate in the UK?

- Morningstar's UK-specific 2024/25 research put the safe inflation-adjusted starting withdrawal rate at 3.7% in 2024 and 3.9% in 2025, for a 30-year retirement at 90% confidence using a balanced portfolio. That is lower than William Bengen's original US 4% rule because UK retirees face higher inflation volatility, lower expected real returns and a different fixed-income mix. A 65-year-old today might reasonably start at 3.7%-4% of their pot, indexed to inflation, but cut withdrawals after very bad investment years (a 'guardrails' strategy) and hold one to two years of expected spending in cash so they never have to sell fund units at depressed prices.

- Drawdown or annuity - which is better in 2026?

- Neither is universally right; the decision turns on whether you most value flexibility or certainty. Drawdown gives you investment growth potential, flexible income and a pot you can leave to family - but no guarantee. An annuity gives you a guaranteed income for life - but no flexibility, and (without a joint-life or guarantee period) nothing left for beneficiaries. May 2026 annuity rates are at their strongest level since the financial crisis: Hargreaves Lansdown's best-buy table shows £7,892 a year per £100,000 for a healthy 65-year-old on a level single-life basis. Many UK retirees split the decision - annuitise enough to cover essentials when added to the State Pension, then keep the rest in drawdown. Pension Wise (free, government-backed) is the right first step before signing anything.

- Can I take all my pension as cash?

- Yes - pension freedoms in April 2015 ended compulsory annuitisation, so from age 55 (rising to 57 from 6 April 2028) you can take a defined contribution pension as cash if you want to. The catch is tax. Only the first 25% (capped by the £268,275 Lump Sum Allowance) is tax-free. The other 75% is taxed as income in the year you withdraw it, which on a £100,000 pot would push most people into higher-rate tax. Small pots under £10,000 can be taken as a 'small lump sum' (the first 25% tax-free, the rest at marginal rate) without triggering the MPAA - and DB pensions under £30,000 can sometimes be taken as a 'trivial commutation' lump sum. For anything larger, taking it all in one go is rarely tax-efficient. Phasing withdrawals across multiple tax years almost always pays less tax.

- When can I start drawing my pension?

- The Normal Minimum Pension Age (NMPA) for accessing a defined contribution pension is currently 55. It rises to 57 from 6 April 2028 under legislation already on the statute book - so anyone born on or after 6 April 1973 will not be able to access their private pension until 57. Some older scheme members have a 'protected' lower retirement age written into their original pension contract; these protections can still apply. The State Pension is separate, with its own State Pension age - currently 66, rising to 67 between April 2026 and April 2028, and to 68 between 2044 and 2046. There is nothing stopping you taking your private pension at 55 and deferring the State Pension to earn the ~5.8%-a-year deferral uplift.

- What happens to my drawdown pension when I die?

- Under the current rules, a defined contribution pension passes to your nominated beneficiary outside your estate. Die before age 75 and the beneficiary receives the pot tax-free, whether they take it as a lump sum or as drawdown income. Die at age 75 or later and the beneficiary pays income tax at their marginal rate on whatever they withdraw - the pot itself is not taxed, only the income drawn from it. From April 2027 the government plans to bring most unused defined contribution pensions inside the inheritance tax estate, which would expose larger estates to a 40% IHT charge on top of the income tax due. This is one of the biggest planning changes coming for retirees with substantial pots - see our guide on inheritance tax and pensions for the detail.

- Do I need a financial adviser for drawdown?

- Legally, no - unlike a final-salary transfer over £30,000, you do not need regulated advice to start drawdown. But you do need a clear plan. Pension Wise (delivered by MoneyHelper) is free, government-backed and takes 60 minutes by phone or video; it covers your options without recommending products. For anything beyond a straightforward small pot, paid regulated advice from an FCA-authorised adviser will usually pay for itself - particularly around tax sequencing, MPAA planning, and (from April 2027) inheritance tax. The FCA's 2024/25 data shows roughly a third of new drawdown accounts were opened without regulated advice, which is up from previous years - concerning given the irreversibility of bad first-year decisions.