Retirement Tax

Most retirees pay some income tax. The State Pension is taxable, drawdown above the 25% tax-free element is taxable, and from April 2027 unused pensions enter your inheritance tax estate. This pillar pulls together the 2026/27 numbers, the cliff edges to avoid, and the six in-depth guides that follow.

- 1 Just took my first pension withdrawal and got hammered→ Emergency tax - HMRC applies a Month-1 code on the first taxable drawdown. Reclaim using form P55, P53Z or P50Z. See the emergency tax guide.

- 2 Wondering if my State Pension is taxable→ Yes. Paid gross by DWP, but it counts as taxable income. HMRC collects the tax due by reducing your private-pension tax code.

- 3 Planning how much drawdown to take this year→ 25% is tax-free, 75% stacks on top of your State Pension and other income. Mind the £50,270 (40%) and £100,000 (taper) cliffs.

- 4 Worried about IHT on my pension after April 2027→ Unused DC pensions enter the estate from 6 April 2027. Spousal exemption still applies. Read the IHT-and-pensions guide.

- 5 Married couple, one on low income→ Check Marriage Allowance - up to £252/year, backdate four years. One of the most under-claimed retirement tax breaks.

The 2026/27 tax bands

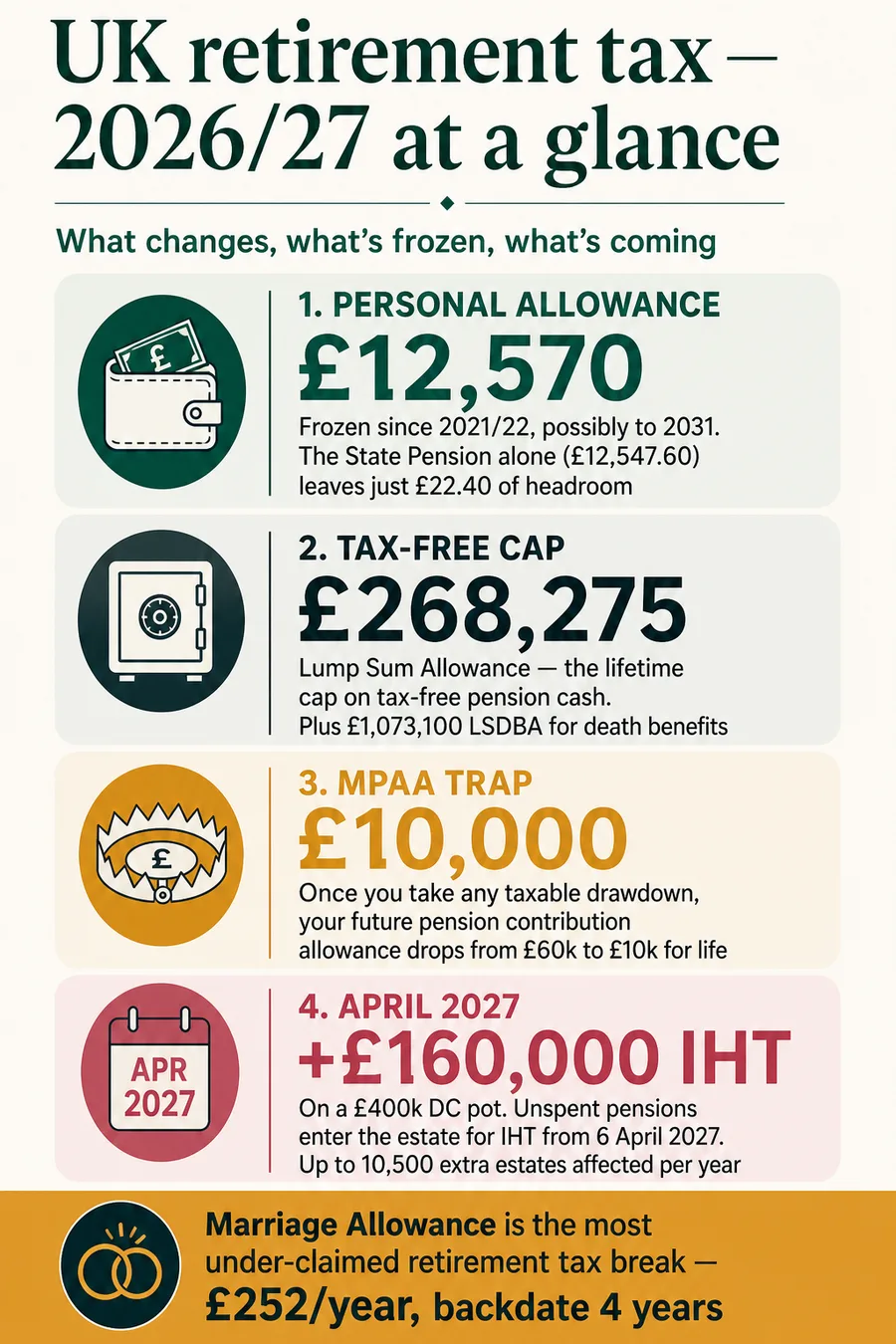

UK income tax in 2026/27 is charged in slabs. The personal allowance is £12,570 - the same for retirees as for anyone else, with no age-related top-up since the old allowance was abolished in 2016. The basic rate of 20% then applies on income up to £50,270, higher rate 40% from £50,271 to £125,140, and additional rate 45% above. The personal allowance has been frozen since 2021/22 and is scheduled to stay frozen until at least April 2028, with several forecasters expecting fiscal-drag extensions out to 2031.

Pension drawdown, the State Pension, annuity income, occupational pensions and rental profits all count as non-savings, non-dividend income - the most heavily-taxed category. They stack on top of each other before any band is applied. The same £20,000 of taxable drawdown costs £4,000 of tax for a basic-rate taxpayer and £8,000 for a higher-rate taxpayer, just because of what other income is already in the picture.

Above £100,000 of total income, the personal allowance tapers at the rate of £1 lost for every £2 over the threshold. By £125,140 the allowance is gone entirely. Inside that £25,140 band the effective marginal rate is 60% - 40% income tax on the extra pound, plus another 20% from the disappearing allowance. Drawdown taken right up to this cliff is one of the most expensive tax mistakes in retirement, and one of the easiest to avoid with two-tax-year splitting.

State Pension is taxable

The full new State Pension is £241.30 a week, or £12,547.60 a year in 2026/27. The personal allowance is £12,570. That leaves precisely £22.40 of headroom before basic-rate tax bites. For anyone with a full or near-full entitlement, every pound of taxable drawdown income and every pound of taxable savings interest above the personal savings allowance is taxed at 20% from the very first pound.

DWP pays the State Pension gross - no tax is deducted at source, because DWP is not a PAYE employer. HMRC collects the tax owed by reducing the tax code that applies to your other PAYE income, usually a private pension, drawdown PAYE stream or final-salary pension. Read your March and April coding notices carefully: the State Pension is the most common reason a tax code is much lower than the standard 1257L.

The State Pension has risen by 4.1% in 2026/27 under the triple lock. If the triple lock continues to deliver mid-single-digit uprating, the full new State Pension is likely to exceed the frozen £12,570 personal allowance during 2027/28 or 2028/29 - at which point even pensioners with no other income at all will start paying small amounts of income tax for the first time. Once that crossover happens, HMRC has to set up a simple assessment process, because there is no PAYE source to collect the tax through.

Drawdown tax - the basics

Every pound that comes out of a defined-contribution pension is split in two. The 25% tax-free element - the PCLS, or the tax-free slice of a UFPLS - is paid free of income tax, does not appear on your tax code, and does not eat into your personal allowance. The other 75% is taxable at your marginal rate, stacked on top of your State Pension and any other income.

Drawing any taxable income from a DC pension also triggers the Money Purchase Annual Allowance (MPAA): from that day, your annual DC contribution allowance drops from £60,000 to £10,000 for 2026/27, and carry forward of unused allowance no longer applies to DC pots. Taking only the 25% PCLS does not trigger the MPAA - but the first taxable pound does, and you cannot un-trigger it. If you are still working and accumulating a workplace pension, do not crystallise anything taxable until you stop.

Expect the first withdrawal to be heavily over-taxed. HMRC's PAYE system applies a Month-1 emergency code that projects the lump sum as if it were monthly income for the whole tax year. A £20,000 first UFPLS in spring can attract £4,500+ of tax instead of the £3,000 actually due. In Q1 2026 alone, HMRC repaid roughly £44 million of over-deducted pension tax. The average refund per claim is north of £3,000. The three reclaim forms are P55 (pot not emptied), P53Z (emptied, with other income), and P50Z (emptied, no other income).

The 25% tax-free element

The lifetime ceiling on tax-free pension cash is the Lump Sum Allowance (LSA) of £268,275, in force since 6 April 2024 when it replaced the Lifetime Allowance. Most retirees never come close to it: it would take a pension pot of more than £1.07 million to generate that much tax-free cash at the standard 25% rate.

Three ways to take it. PCLS takes the full 25% in one go up-front, and the remaining 75% sits in flexi-access drawdown to be drawn at your own pace. UFPLS takes a slice of the whole pot at once - 25% tax-free, 75% taxable, every time. Phased drawdown crystallises smaller chunks each year, drawing the 25% tax-free slice of each chunk to fill a target income. Mathematically, taking £268,275 of tax-free cash all at once costs the same as taking it in slices - the difference is timing, growth on the residual pot, and which trigger events apply.

Scotland is different

Scottish-resident taxpayers pay Scottish income tax on their pension drawdown, occupational pension and State Pension income. Scotland uses six bands in 2026/27: starter 19% on £12,571-£16,537, basic 20% on £16,538-£29,526, intermediate 21% on £29,527-£43,662, higher 42% on £43,663-£75,000, advanced 45% on £75,001-£125,140, and a top rate of 48% above £125,140 (introduced in April 2024). The £12,570 personal allowance is the same UK-wide. HMRC flags you as Scottish-resident based on where your main home is during the tax year, and your tax code is prefixed with an S.

Marriage Allowance

Probably the most under-claimed retirement tax break. If one spouse or civil partner has income below the £12,570 personal allowance and the other is a basic-rate taxpayer (£12,571-£50,270, or up to £43,662 in Scotland), the lower earner can transfer £1,260 of personal allowance to the higher earner. The recipient pays £252/year less tax. Claims can be backdated four tax years - worth roughly £1,000 in arrears if eligibility has held the whole time. Apply once through GOV.UK; the election rolls over automatically until cancelled or circumstances change.

April 2027 - pensions enter the IHT estate

The single biggest retirement-tax change of the decade lands on 6 April 2027. From that date, unused defined-contribution pension funds and most lump-sum death benefits will form part of the deceased member's estate for inheritance tax purposes. The 40% IHT rate applies above the £325,000 nil-rate band (plus the residence nil-rate band where applicable). The Office for Budget Responsibility estimates the change will pull up to 10,500 additional estates a year into IHT.

What is changing: the long-standing "pensions are outside the estate" planning rule that made SIPPs a wealth-transfer vehicle of choice over the past decade. What is not changing: the spousal exemption, which means anything passing to a UK-domiciled spouse or civil partner remains entirely IHT-free; and the pre-75 / post-75 income-tax treatment of beneficiary withdrawals - beneficiaries of someone who died before age 75 can still draw the pot income-tax-free, while those inheriting from someone who died after 75 pay income tax at their own marginal rate.

Planning implications worth thinking through with an adviser before April 2027: whether to draw earlier in retirement to leave less in the wrapper at death; whether to gift surplus income or lump sums under the seven-year-rule or the "normal expenditure out of income" exemption; whether the residence nil-rate band - which tapers above a £2 million estate - is now in scope for a household it previously did not affect; and whether spousal bypass trusts or revised expression-of-wish nominations still make sense under the new regime.

Guides in this section

Six in-depth guides covering retirement tax for the 2026/27 tax year.

- 01 Is the State Pension taxable?

How the State Pension counts as taxable income, how HMRC collects the tax, and what happens if your pension uses up your personal allowance.

Read guide → - 02 Tax on pension drawdown

How income tax works on flexi-access drawdown, the 25% tax-free element, and how to avoid pushing yourself into a higher tax band.

Read guide → - 03 Emergency tax on pension withdrawals

Why HMRC often emergency-taxes your first pension withdrawal, the forms you can use to reclaim it, and how to avoid the problem.

Read guide → - 04 How much pension can I take tax-free?

The 25% tax-free rule, the Lump Sum Allowance, and how the rules apply to defined contribution and defined benefit pensions.

Read guide → - 05 Marriage Allowance for pensioners

How retired couples can use Marriage Allowance to save up to £252 in tax, who qualifies, and how to apply through HMRC.

Read guide → - 06 Inheritance tax and pensions

How pensions interact with inheritance tax, the changes scheduled for April 2027, and what passes to your beneficiaries.

Read guide →

Frequently asked questions

- Do I pay tax on my UK pension?

- Yes, most pension income is taxable in the UK. The State Pension and any taxable drawdown or annuity income are added together with earnings, rental profits and savings interest above the personal savings allowance, and the total is taxed in slabs. In 2026/27 the personal allowance is £12,570 (0%), basic rate 20% applies up to £50,270 of total income, higher rate 40% from £50,271 to £125,140, and additional rate 45% above. Scottish-resident taxpayers pay Scottish rates on their pension income - six bands from 19% to 48%. The only meaningful tax-free slice is the 25% pension commencement lump sum (PCLS), capped at the £268,275 Lump Sum Allowance.

- Is the State Pension taxable?

- Yes. The State Pension is treated as taxable income in the year it is paid, even though DWP pays it gross without deducting tax at source. HMRC collects the tax owed on the State Pension by reducing the tax code that applies to your other PAYE income - usually a private pension, drawdown PAYE stream or final-salary pension. In 2026/27 the full new State Pension is £241.30 a week, or £12,547.60 a year, which uses almost all of the £12,570 personal allowance and leaves just £22.40 of headroom. If the State Pension is your only income, you pay no tax - but the moment you add drawdown or other income, basic-rate tax bites from the first pound.

- How much pension can I take tax-free?

- Most savers can take 25% of each defined-contribution pension as a tax-free lump sum, up to a lifetime ceiling of £268,275 called the Lump Sum Allowance. The LSA replaced the Lifetime Allowance on 6 April 2024 and remains in force for 2026/27. You can take the tax-free element as a one-off pension commencement lump sum (PCLS) at the start, as the 25% slice of each UFPLS withdrawal, or in phases alongside regular drawdown income - the tax outcome is the same. The remaining 75% of any pension you crystallise is taxable as income at your marginal rate when you draw it.

- Why was my pension withdrawal taxed so much?

- HMRC almost always applies an emergency Month-1 tax code to your first taxable pension withdrawal. The provider taxes the lump sum as if you were going to take the same amount every month for the rest of the tax year, which over-projects your income and over-deducts the tax. A £20,000 first UFPLS in spring can attract £4,500+ in tax instead of the £3,000 actually due. Reclaim using form P55 if you have not emptied the pot, P53Z if you have emptied it but have other taxable income, or P50Z if you have emptied it and have no other income. HMRC typically repays within 30 working days. In Q1 2026 alone, HMRC repaid roughly £44 million of over-deducted pension tax.

- Will my pension be subject to inheritance tax from 2027?

- Yes - for most unused defined-contribution pension pots, from 6 April 2027. The 2024 Autumn Budget confirmed that from that date, unused DC pension funds and most lump-sum death benefits will form part of the deceased member's estate for inheritance tax purposes. The 40% IHT charge applies above the £325,000 nil-rate band (plus the residence nil-rate band where relevant). The Office for Budget Responsibility estimates up to 10,500 additional estates a year will pay IHT under the new rules. What is not changing: transfers between spouses and civil partners remain IHT-exempt, and the pre-75 / post-75 income-tax treatment of beneficiary withdrawals stays the same.

- Do retirees get a higher Personal Allowance?

- No. The age-related personal allowance was abolished in 2016, and pensioners now get exactly the same £12,570 allowance as anyone else in 2026/27. The allowance has been frozen since 2021/22 and is currently scheduled to remain at £12,570 until at least April 2028, with several forecasters expecting the freeze to extend to 2031. As the State Pension rises each year under the triple lock, the gap between the State Pension and the personal allowance closes - by 2027/28 or 2028/29, the full new State Pension is likely to exceed the personal allowance on its own, meaning DWP-pensioners with no other income would start paying basic-rate tax for the first time.

- Is pension income taxed differently in Scotland?

- Yes. Scottish-resident taxpayers pay Scottish income tax on their pension drawdown, occupational pension and State Pension income. Scotland uses six bands in 2026/27: starter 19% on £12,571-£16,537, basic 20% on £16,538-£29,526, intermediate 21% on £29,527-£43,662, higher 42% on £43,663-£75,000, advanced 45% on £75,001-£125,140, and top rate 48% above £125,140. The £12,570 personal allowance is the same UK-wide. HMRC identifies you as Scottish-resident based on where your main home is during the tax year, not where your pension provider is based, and your tax code is prefixed with an S.

- How does Marriage Allowance work for pensioners?

- Marriage Allowance is one of the most under-claimed tax breaks among retired couples. If one spouse or civil partner has income below the £12,570 personal allowance and the other is a basic-rate taxpayer (£12,571-£50,270, or up to £43,662 in Scotland), the lower earner can transfer £1,260 of personal allowance to the higher earner. The recipient gets a tax reduction worth up to £252 a year. Claims can be backdated four tax years - worth roughly £1,000 in arrears if you have been eligible the whole time. Once you elect through GOV.UK it carries on automatically each year until you cancel or your circumstances change.