Equity Release & Later-Life Lending

Equity release lets UK homeowners aged 55+ unlock tax-free cash from their home without moving. The market is overwhelmingly lifetime mortgages, regulated by the FCA and underpinned by the Equity Release Council's no-negative-equity guarantee. It is also expensive - interest compounds for the rest of your life - and the cheaper alternatives almost always deserve a serious look first.

Four numbers frame every equity-release conversation. Start here, then read on for what they mean for your home and your family.

Equity release is rarely one-size-fits-all — the right move depends on your situation. Find the scenario closest to yours.

- 1 I want a one-off lump sum and don't mind reduced inheritance→ Consider a lifetime mortgage and take regulated advice. Get at least three quotes and look hard at a drawdown plan rather than a lump sum to minimise the compounding bill.

- 2 I want monthly cash flow and have decent pension income→ A retirement interest-only (RIO) mortgage is usually cheaper - you pay the monthly interest from income and the balance stays flat instead of ballooning.

- 3 I want to fund care at home→ Equity release can be a reasonable fit, especially given the 2025 long-term-care ERC waiver. But check Attendance Allowance and local-authority care funding first - care-home funding has cheaper routes.

- 4 I want to clear a mortgage that runs into retirement→ Draw down pension tax-free cash first (25% of a DC pension is tax-free from age 55). Or refinance to a RIO or older-borrower mortgage. Lifetime mortgage rates are higher than mainstream retirement mortgages.

- 5 I'd be happy with a smaller home→ Downsize. Selling and moving realises cash outright with no compounding interest, usually leaves more for the family, and tops up your retirement pot cleanly. Almost always cheaper than equity release.

What equity release is

Equity release is a way for UK homeowners aged 55 or over to unlock some of the cash tied up in their home without moving. The money is paid tax-free because it is either a loan or a partial property sale - not income. The debt is normally only repaid when you die or move permanently into long-term care, at which point the property is sold and the loan plus all rolled-up interest is paid out of the proceeds; anything left over passes to your estate.

There are two products. The lifetime mortgage - over 99% of new plans in 2025 and 2026 - is a loan secured against your home where you keep ownership. Interest is added each year and itself attracts interest (compounding), unless you choose to make voluntary repayments. The home reversion plan - under 1% of the market - involves selling all or part of your home to a provider at well below market value in exchange for tax-free cash and the right to live there rent-free for life.

You must be a homeowner, the property must be your main residence and broadly mortgageable (condition, construction type and location matter), and you must have the mental capacity to enter into the contract at the time of application. Equity release is FCA-regulated under MCOB 8 - taking regulated advice from an adviser with the CeRER qualification is mandatory, as is using an independent solicitor for the legal work.

How the maths actually works

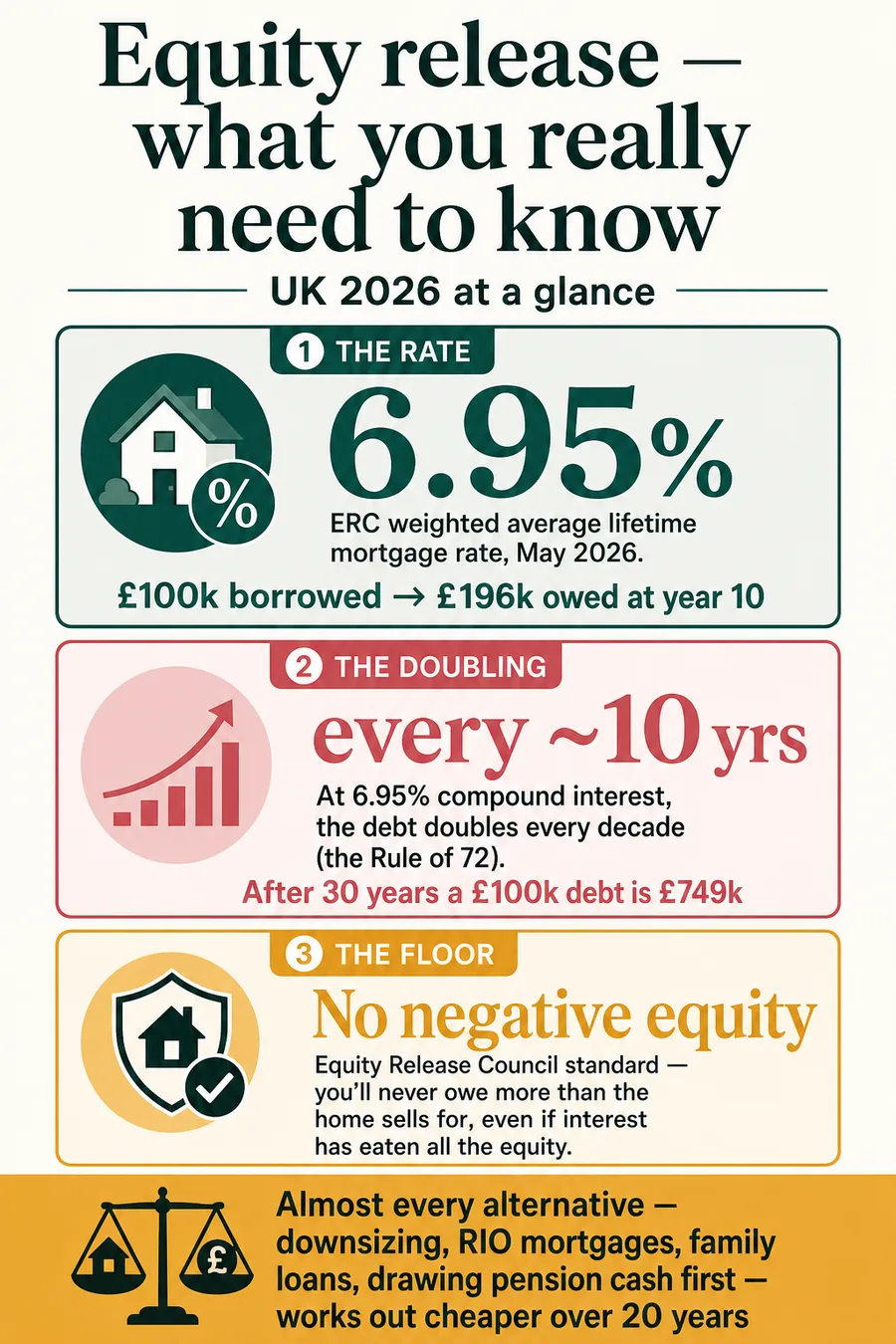

The single most important number on this page is the compounding rate. At the May 2026 Equity Release Council weighted average of 6.95%, a debt left to roll up doubles roughly every 10 years - the "Rule of 72" gives a quick estimate (72 ÷ 6.95 ≈ 10.4). This is the mechanism behind why advisers sometimes describe equity release as "borrowing from your beneficiaries".

Take a representative £100,000 lifetime mortgage at 6.95%, no voluntary repayments:

| Years elapsed | Debt owed | Multiple of original |

|---|---|---|

| Year 10 | ~£196,000 | ~2× |

| Year 20 | ~£383,000 | ~3.8× |

| Year 30 | ~£749,000 | ~7.5× |

The same numbers, in one picture — what a rolled-up loan does to your equity over time:

Take it out at 65, live to 95, and the debt has grown by roughly 7.5×. On most UK property values that is the lion's share of the home gone to the lender. The no-negative-equity guarantee means you cannot owe more than the home actually sells for - but it does not preserve any residual equity for the family. The shortfall is the lender's loss; the rest of the loss is the family's.

Three things blunt this picture in practice. Voluntary repayments of up to 10% per year are penalty-free under Equity Release Council standards - even £200/month against a £100k loan keeps the debt roughly flat at 6.95%. Drawdown plans only charge interest on cash actually drawn, so a £150k reserve sitting unused costs nothing. House price growth partially offsets compounding - but only partially. A flat 3.5% annual rise still loses ground to a 6.95% interest rate.

See our full equity release explainer for the year-by-year cost tables and an inline calculator.

Speak to an FCA-regulated equity release adviser

Compare lifetime mortgages and alternatives with a qualified later-life lending specialist. No fee unless you proceed.

The five Equity Release Council safeguards

Around 90%+ of UK equity release advisers and lenders are members of the Equity Release Council, the industry body whose product standards sit above the FCA baseline. Plans from members carry five guarantees:

- Fixed or capped interest rate for life - the rate is set at the start and cannot rise (if variable, it must have a lifetime cap). Almost all new plans are fixed.

- Right to remain in your home for life - or until you need to move into long-term care - provided it remains your main residence and you meet the contract terms.

- No-negative-equity guarantee (NNEG) - neither you nor your estate can ever owe more than the home sells for, provided it is sold for the best price reasonably obtainable.

- Voluntary partial repayments - every ERC-compliant plan since March 2022 must let you make penalty-free repayments, typically up to 10% of the loan each year.

- Downsizing protection - you can usually move to a smaller home without penalty, subject to the new property being acceptable as security.

In May 2025, ERC Standards 2.0 added a sixth protection: Early Repayment Charges are waived entirely if you move permanently into long-term care (including some informal care arrangements at home, with a medical practitioner's certificate).

The means-tested benefits trap

This is the trap regulated advisers should be flagging - and the one many borrowers learn about too late. The released cash is tax-free, but the moment it lands in your bank account it counts as capital for means-tested benefits.

Pension Credit, Council Tax Reduction, Housing Benefit and Universal Credit are all affected. Capital under £6,000 is ignored; between £6,000 and £16,000 it reduces your benefit by £1 a week for every £500 above £6,000; capital over £16,000 disqualifies you from Pension Credit and most Universal Credit awards outright. The average new lump-sum plan of £127,414 is well over that threshold.

- Under £6,000 — ignored, no effect on means-tested benefits.

- £6,000–£16,000 — tapered: you lose £1/week of benefit per £500 above £6,000.

- Over £16,000 — disqualifies you from Pension Credit and most Universal Credit. A £127k lump sum lands here.

There are two main fixes. Spend the cash promptly on a non-savings purpose (paying off a mortgage, home improvements, care fees) so it does not sit as capital. Or take a drawdown plan that holds the reserve with the lender (where it is not "your" capital) and only releases tranches as you need them. Take dedicated advice on this before applying - see our deeper guide to equity release and means-tested benefits.

The alternatives most people overlook

An FCA-regulated adviser is required to consider alternatives and document why they are not appropriate before recommending equity release. Five usually come up:

- Downsizing. Selling and moving releases real cash with no debt and no compounding. SDLT, agent fees and moving costs typically total 3-8% of the new property price - small compared with 20+ years of interest at 6.95%. Almost always the cheapest route if you would be content with a smaller home.

- Retirement interest-only (RIO) mortgage. You pay the monthly interest from income and the capital balance stays flat. Over 20 years a £100k RIO costs roughly £100k-£140k in interest payments and leaves the £100k debt at the end - versus a £283k balloon on a rolled-up lifetime mortgage. See lifetime mortgage vs RIO.

- Pension tax-free cash first. 25% of a defined contribution pension is tax-free from age 55 (rising to 57 from April 2028). For many households this is the cheapest pool of money to spend in the first decade of retirement - and from April 2027 it is in your estate for IHT anyway.

- Family loan or formal IOU. A documented zero-interest loan from adult children, repaid from your estate, can be radically cheaper than borrowing at 6.95%. Beware family dynamics; do it through a solicitor.

- Unclaimed Pension Credit and Council Tax Reduction. An estimated £2.2bn of Pension Credit goes unclaimed each year. A successful claim opens the door to Council Tax Reduction, Housing Benefit, free TV licence (75+) and the Winter Fuel Payment - often worth more annually than the cash equity release would release.

Full comparison in our equity release alternatives guide.

The April 2027 inheritance tax change

From 6 April 2027, most unused defined contribution pensions and pension death benefits enter your estate for inheritance tax (HM Treasury, July 2025 consultation response). That changes the planning maths for some households. Equity release reduces the value of your estate - because the debt is repaid before anything passes to beneficiaries - so it can offset some of the new pension-IHT exposure.

But the trade rarely stacks up: at 6.95% compounding, a £200k release at age 70 grows to roughly £767k by year 20, which is far more than the IHT it is likely to save. The simpler moves are usually spending pension first, gifting from surplus income, and using the annual exemptions.

Why regulated advice matters

Equity release is regulated by the FCA under MCOB 8 (advising and selling) and MCOB 9 (product disclosure). You must take regulated advice - DIY is not permitted - and use an independent solicitor. The minimum adviser qualification is CeRER (Certificate in Regulated Equity Release), and Equity Release Council members commit to a code that goes beyond the FCA baseline.

Watch out for sales pressure: limited-time offers, "exclusive" rates, free valuations conditional on signing, and any pitch that does not walk you through the alternatives. If you cannot remember being shown the alternatives, the advice may not have been compliant. Use the free MoneyHelper equity release guide and check whether your adviser is on the Equity Release Council member directory.

Speak to an FCA-regulated equity release adviser

Compare lifetime mortgages and alternatives with a qualified later-life lending specialist. No fee unless you proceed.

- Free, no-pressure first chat, typically by phone or video

- Whole-of-market comparison across FCA-regulated lenders

- You stay in control and decide if you take it any further

RetirementExpert is an information service, not an adviser. By submitting this form you consent to being contacted by an FCA-regulated equity release specialist.

Guides in this section

Six in-depth guides covering equity release & later-life lending for the 2026/27 tax year.

- 01 Equity release explained

What equity release is, the two main types - lifetime mortgages and home reversion - and how interest rolls up over time.

Read guide → - 02 Equity release: pros and cons

A balanced look at the benefits and the risks of equity release, including the no-negative-equity guarantee and the impact on your estate.

Read guide → - 03 Equity release alternatives

Downsizing, retirement interest-only mortgages, family loans and using savings - alternatives to consider before releasing equity.

Read guide → - 04 Lifetime mortgage vs retirement interest-only

How a lifetime mortgage compares to a retirement interest-only (RIO) mortgage, with worked examples of the long-term cost.

Read guide → - 05 Does equity release affect benefits?

Equity release can affect means-tested benefits like Pension Credit and Council Tax Reduction. Here is how - and what to check first.

Read guide → - 06 Equity release for care costs

When equity release might fund care at home, the risks, and lower-cost alternatives such as deferred payment agreements with the council.

Read guide →

Frequently asked questions

- What is equity release and how does it work?

- Equity release is a way for UK homeowners aged 55+ to unlock tax-free cash from their home without moving. The dominant product (more than 99% of new plans) is the lifetime mortgage - a loan secured against your home where interest rolls up and compounds. The loan plus all rolled-up interest is repaid from the sale of the property when you die or move into long-term care. The other product, home reversion, involves selling part of your home to a provider at below market value in exchange for tax-free cash. Equity release is FCA-regulated under MCOB 8 and most plans come with five Equity Release Council safeguards including a no-negative-equity guarantee.

- How much does equity release cost in 2026?

- The Equity Release Council weighted average rate for a new lifetime mortgage in May 2026 is around 6.95%. The cheapest advertised plans sit a little below that, around 6.6-6.7% MER. Set-up costs typically add £1,500-£3,000 on top of the loan: advice fee, valuation, legal fees and arrangement fee. The real long-run cost is compound interest: at 6.95% the debt roughly doubles every 10 years (the "Rule of 72"), so £100,000 borrowed today and left untouched grows to roughly £196,000 by year 10, £383,000 by year 20 and £749,000 by year 30.

- Are there alternatives to equity release?

- Yes - and an FCA-regulated adviser is required to consider them before recommending a plan. The main alternatives are downsizing (releases real cash with no debt), a retirement interest-only (RIO) mortgage where you pay monthly interest from income so the balance stays flat, a standard older-borrower mortgage if you have provable income, drawing pension tax-free cash first, a family loan, and claiming any unclaimed Pension Credit. For many households, a successful Pension Credit claim is worth more annually than equity release would ever release. See our full alternatives guide for the trade-offs.

- Will equity release affect my benefits?

- It does not affect the State Pension (not means-tested). But released cash sitting in your bank counts as savings for Pension Credit, Council Tax Reduction, Housing Benefit and Universal Credit. Savings over £6,000 reduce these benefits and savings over £16,000 disqualify you from Pension Credit and most Universal Credit awards. The £127,414 average lump-sum plan would wipe out most means-tested entitlements unless spent quickly on a non-savings purpose. A drawdown plan that releases small tranches as needed is usually the safer shape if benefits are in play.

- Can I use equity release to pay for care?

- Sometimes, particularly for care at home where the alternative is selling. Since May 2025 the Equity Release Council standards include a waiver that cancels Early Repayment Charges if you (or, on a joint plan, the second borrower) move permanently into long-term care. But for residential care funding, equity release is rarely the cheapest answer: the local authority funding rules, deferred payment agreements, Attendance Allowance and NHS Continuing Healthcare all need to be checked first. Our care funding guide walks through the comparison.

- What's the difference between a lifetime mortgage and a RIO?

- A lifetime mortgage has no required monthly payment - interest rolls up and compounds, and the whole debt is repaid when you die or move into care. A retirement interest-only (RIO) mortgage requires a monthly interest payment from your pension income, but the capital balance stays flat - it does not balloon over time. RIO is usually significantly cheaper over a long retirement provided you can afford the monthly interest. The trade-off is that RIO needs you to evidence sustainable retirement income, and a missed payment can put your home at risk in the conventional way.

- Can I lose my home with equity release?

- Not in the usual sense. A plan from an Equity Release Council member gives you the right to remain in your home for life (or until you move into long-term care), provided it remains your main residence and you keep up routine obligations such as buildings insurance and reasonable upkeep. The no-negative-equity guarantee means you can never owe more than the property sells for. The realistic risks are different: interest can eat most of your equity over time, leaving little for beneficiaries; and if you breach the contract (long absences, sub-letting, failure to maintain the property) the lender can demand repayment.

- Should I tell my family before taking out equity release?

- Yes - and a good adviser will encourage it. Equity release reduces (often substantially) what passes to beneficiaries, and family members can sometimes offer cheaper help - an interest-free family loan, a contribution towards a downsizing move, or simply a different solution you had not considered. Some lenders insist on an adult child being present at the legal advice meeting. The Equity Release Council code also requires advisers to discuss the impact on family and any expected inheritance.