Care, Housing & Family Decisions

Retirement is rarely just about pensions. These six guides cover the bigger decisions of later life - paying for care, sorting out a lasting power of attorney, helping elderly parents, downsizing, and dealing with a mortgage that runs into retirement.

Above this you pay the full cost. Below £14,250 only your income is assessed. Your property is disregarded if a spouse, partner or dependent relative still lives there. Scotland uses £35,000; Wales has a single flat £50,000 limit.

- 1 You are helping a parent who is still well→ Run a benefits check (Attendance Allowance, Pension Credit, Council Tax Reduction) and set up Lasting Powers of Attorney now - while they have capacity. Both jobs together usually take a weekend.

- 2 You are planning ahead for your own later life→ Three priorities: register both LPAs, decide whether to downsize while the housing market is in your favour, and start inheritance-tax planning if your estate is heading above the nil-rate bands.

- 3 A parent needs care now→ Ask the council for a free Care Act needs assessment, request an NHS Continuing Healthcare checklist before signing anything, then read up on the means test and the four-nation capital limits.

- 4 A parent has lost capacity and there is no LPA in place→ You will need to apply to the Court of Protection to become a deputy. Budget £400+ in fees, 6-12 months of waiting, and ongoing supervision. Avoid this route by setting up LPAs early.

- 5 Your mortgage is running into retirement→ Six options to weigh up - extending the term, switching to interest-only, retirement interest-only (RIO), a lifetime mortgage, downsizing, or using pension tax-free cash to clear it.

The two big decisions of later life

Most retirement planning starts with pensions and stops there. But the two decisions that dominate later life tend to lie elsewhere - what happens if you (or a parent) need care, and what happens if you lose the mental capacity to make your own financial decisions. Neither is pleasant to think about. Both are extremely expensive to get wrong. And both are best handled years before they become urgent.

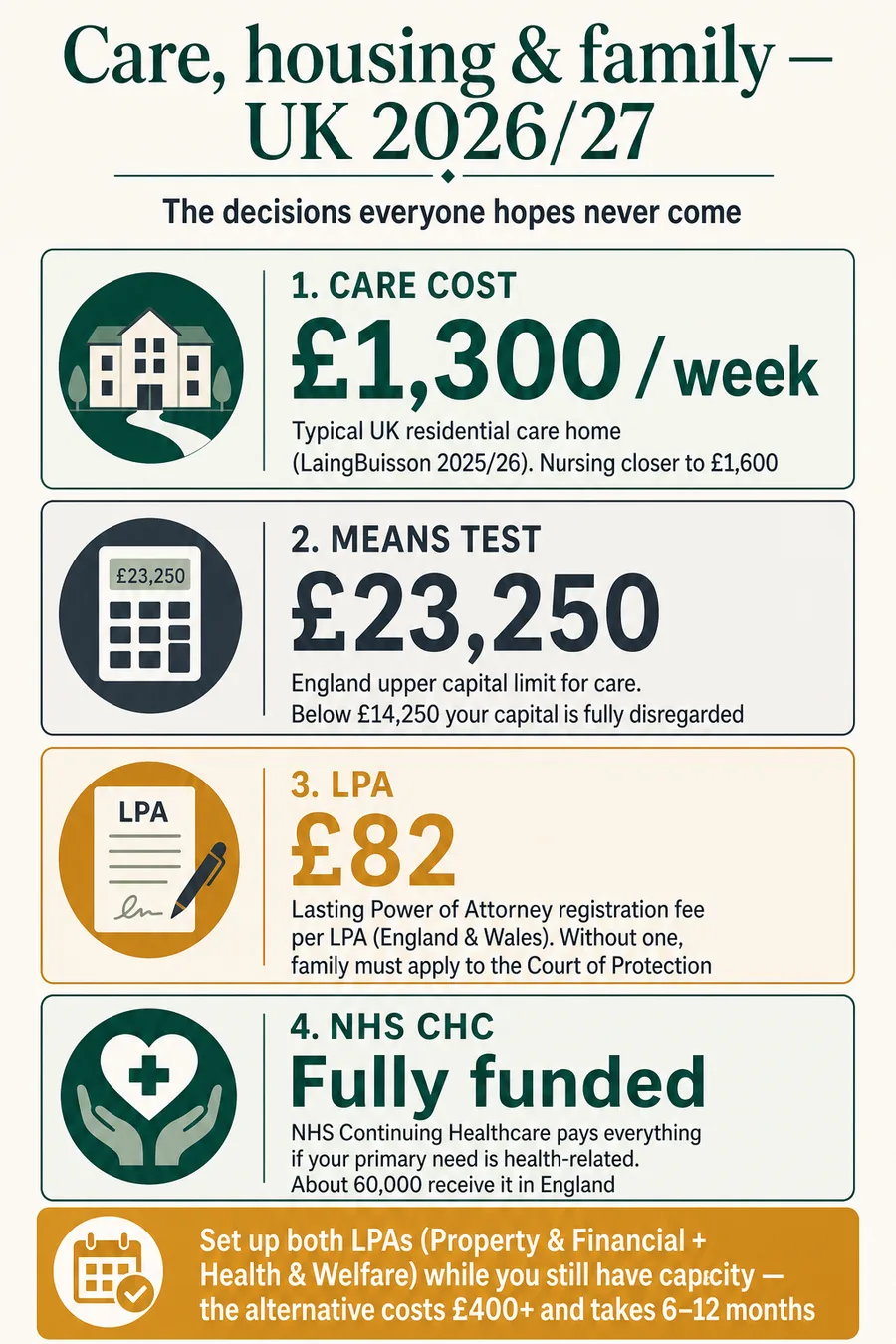

The numbers are sobering. The average self-funder pays around £1,300 a week for residential care in the UK and £1,600 a week for nursing - roughly £68,000 and £83,000 a year. Roughly one in seven over-85s will live in a care home at some point, and the median length of stay is around two and a half years. Capacity, meanwhile, is not something most people associate with their own future: but around one in fourteen people over 65 has dementia, rising to one in six over 80. The decisions you make today about Lasting Powers of Attorney, your home, and your savings shape how those years play out for everyone in the family.

The good news is that none of this is mysterious. The means-test rules are written down, the LPA paperwork is standardised, and the NHS Continuing Healthcare framework - though notoriously difficult - is at least transparent. The six guides linked below walk through the specifics; this page is the map.

Care home fees - who pays?

Long-term care in the UK is means-tested, not free at the point of use. The local authority runs a financial assessment that adds up your assessable capital - savings, investments, second properties, and (where the disregards do not apply) your main home - and compares it to a national threshold. Adult social care is fully devolved, so the threshold depends on where you live.

In England and Northern Ireland the upper capital limit is £23,250 and the lower limit is £14,250. Above £23,250 you pay the full cost yourself. Below £14,250 your capital is ignored entirely. Between the two, the council adds £1 a week of "tariff income" for every £250 of capital above the lower limit - twice as harsh as the Pension Credit £1-per-£500 rule. Scotland uses £35,000 and £21,500, and also pays a Free Personal Care contribution of around £248.70/week to anyone aged 65+ in residential care. Wales has the most generous and the simplest rules - a single flat £50,000 capital limit and no tariff income.

Two further mechanics matter. The first is the property disregard: the value of your home is fully ignored if a spouse, partner, dependent child or qualifying relative still lives in it. If the home does count, a mandatory 12-week disregard gives you breathing space at the point of admission to arrange a sale or a deferred payment agreement. The second is NHS Continuing Healthcare: if your needs are primarily medical (severe dementia, end-of-life, complex post-stroke care), the NHS pays everything regardless of capital. About 60,000 people in England are in receipt at any time. Always ask for a CHC checklist before signing a self-funder contract - the screening is free and a positive result moves the entire bill onto the NHS.

Our deep-dive on care home fees and the means test walks through all four nations with worked examples and an inline calculator.

Lasting Power of Attorney

A Lasting Power of Attorney is the single most important document most people over 60 should have - more important, day to day, than a will. An LPA lets you appoint someone you trust to make decisions on your behalf if you lose the mental capacity to make them yourself.

There are two separate LPAs in England and Wales: Property and Financial Affairs (paying bills, managing investments, selling the house) and Health and Welfare (care arrangements, medical treatment, where you live). They are independent - you can register one without the other, but most advisers recommend registering both. Each costs £92 to register with the Office of the Public Guardian. Fee remissions are available if your income is below £12,000 or you receive certain means-tested benefits. OPG processing currently takes 8-10 weeks.

The alternative is no alternative. If you lose capacity without an LPA in place, your family must apply to the Court of Protection to become a deputy. It costs at least £400 in court fees, takes 6-12 months, brings ongoing supervision by the Public Guardian, and gives the deputy materially fewer powers than an attorney. The Mental Capacity Act 2005 sets out the five principles that govern all of this - including the presumption of capacity and the right to make unwise decisions.

Our step-by-step guide on setting up a Lasting Power of Attorney covers the forms, the witness rules and how to brief your attorneys.

Should you give the house to your children?

Almost never. Gifting the family home is one of the most heavily marketed "tax planning" ideas in the UK and one of the most consistently disastrous. HMRC will treat the transfer as a gift with reservation of benefit (GROB) if you continue to live there without paying a full market rent - meaning the house stays in your estate for inheritance tax. The council can treat it as deliberate deprivation of assets and means-test you as if you still owned it (there is no seven-year rule for care fees). Your children inherit your capital gains tax history, losing the main-residence exemption on a future sale. And the house becomes vulnerable to your children's divorces, bankruptcies and premature deaths.

Our detailed guide on why gifting the house to children rarely works walks through GROB, deprivation of assets, CGT and the few narrow situations where some form of transfer can be sensible.

Downsizing vs equity release

If you want to release capital from your home, two routes dominate: downsizing or equity release (a lifetime mortgage). They are not equivalent. Downsizing releases real cash, in your hand, with no compounding debt - and the smaller property keeps paying off through lower council tax, heating and maintenance bills for the rest of your life. The cost is the move itself: stamp duty, estate-agent and legal fees, and the emotional toll of leaving a family home. For most retirees, downsizing is the cheapest way to release equity.

Equity release is occasionally the right answer - particularly if you have a strong preference for staying in the current home and the property is genuinely too large to sell easily. But 6.5-7.5% rolled-up interest doubles the loan every 10-11 years, and the cost compounds against your estate. Read our guide to downsizing in retirement and our plain-English equity release explainer before committing to either.

Helping elderly parents

If you are an adult child looking after an ageing parent's finances, three priorities matter more than anything else. One - run a benefits check. Attendance Allowance (£114.60/week at the higher rate for 2026/27) is non-means-tested, tax-free, and routinely under-claimed. Pension Credit is the gateway to Council Tax Reduction, the Warm Home Discount, free NHS dental treatment and a free TV licence. Two - set up LPAs while they still have capacity. If you wait until capacity is in doubt, you are in Court of Protection territory. Three - sort out banking. Most UK banks now offer formal third-party access arrangements that are safer and more transparent than the informal "I've got their PIN" set-up most families drift into.

Our adult child's checklist for helping elderly parents walks through each in detail, plus the warning signs of cognitive decline and the conversations worth having early.

Retiring with a mortgage

Retiring with a mortgage outstanding is increasingly common - partly because people are buying later, partly because interest-only mortgages from the 1990s are now reaching term end. Six options are worth knowing: extending the existing mortgage term, switching to interest-only on a standard mortgage, taking a retirement interest-only (RIO) mortgage, drawing pension tax-free cash to clear the balance, downsizing, or - at the last resort - a lifetime mortgage. The right answer depends on your age, income, the size of the balance and what you want to leave to your family. Our six paths through a retirement mortgage sets out the pros and cons of each.

Guides in this section

Six in-depth guides covering care, housing & family decisions for the 2026/27 tax year.

- 01 Paying for care home fees

How the local authority means test works, the upper and lower capital limits, and what you can do to plan for care fees.

Read guide → - 02 Can I give my house to my children?

The risks of gifting your home to your children - inheritance tax, deprivation of assets, gift with reservation, and capital gains tax.

Read guide → - 03 Downsizing in retirement

When downsizing makes sense, the real costs (stamp duty, moving, legal) and how to weigh it up against equity release.

Read guide → - 04 Retiring with a mortgage

How to handle a mortgage that runs into retirement - extending the term, RIO mortgages, drawdown to clear it, or downsizing.

Read guide → - 05 Helping elderly parents with money

Practical steps for adult children - checking entitlements, setting up online banking safely, third-party access and lasting power of attorney.

Read guide → - 06 Lasting power of attorney and retirement planning

The two types of LPA, why they matter more than a will for retirement planning, and how to register one with the Office of the Public Guardian.

Read guide →

Frequently asked questions

- Who pays for care home fees in the UK?

- It depends on your capital, the nature of your needs, and which UK nation you live in. In England and Northern Ireland the local authority starts contributing once your assessable capital falls below £23,250 - above that you are a self-funder. Scotland uses £35,000 and pays a Free Personal Care contribution of around £248.70/week to residents aged 65 and over. Wales has a single £50,000 flat capital limit. If your primary need is health rather than social - for example advanced dementia or end-of-life care - NHS Continuing Healthcare pays the full cost regardless of capital. About 60,000 people in England are in receipt at any one time.

- Will I have to sell my house to pay for care?

- Not necessarily. The value of your home is fully disregarded if a spouse, civil partner, unmarried partner, dependent child under 16, or a relative aged 60+ or who is incapacitated still lives there as their main residence. Where the home does count as capital, there is a mandatory 12-week property disregard at the point of admission, after which you can sign a Deferred Payment Agreement with the council. A DPA lets you defer the bill until the property is eventually sold, with interest currently around 3.31% - far cheaper than equity release or an emergency sale.

- What is a Lasting Power of Attorney and how much does it cost?

- A Lasting Power of Attorney (LPA) is a legal document letting you appoint someone to make decisions for you if you lose mental capacity. There are two separate LPAs - Property and Financial Affairs, and Health and Welfare - and each costs £92 to register with the Office of the Public Guardian in England and Wales, up from £82 on 17 November 2025 (£87 in Scotland for the equivalent Continuing Power of Attorney; Northern Ireland uses Enduring Powers of Attorney). Processing currently takes 8-10 weeks. Without an LPA in place, family members must apply to the Court of Protection to become a deputy - a process where the application fee alone is £432, takes 6-12 months, and brings ongoing supervision.

- Should I give my house to my children?

- In almost all cases, no. Gifting the family home rarely works as people hope. HMRC will treat the transfer as a gift with reservation of benefit (GROB) if you continue to live there rent-free, keeping it inside your estate for inheritance tax. The council can treat it as deliberate deprivation of capital and means-test you as if you still owned it. Your children inherit your capital gains tax history, losing the main-residence exemption on a future sale. And if your children divorce, go bankrupt or die before you, the property follows their estate, not yours. Take regulated advice before any transfer.

- How does downsizing in retirement work?

- Downsizing means selling your current home and buying a smaller, cheaper one, releasing the difference as cash. For a typical retired couple, moving from a four-bed family home worth £450,000 to a two-bed bungalow at £275,000 releases around £160,000 after stamp duty, estate agent fees, legal costs and moving expenses (which together usually total £15,000-£25,000). Unlike equity release, downsizing releases real cash that is not subject to compounding interest, and the lower running costs (council tax, heating, maintenance) keep paying off year after year. The trade-off is the emotional and physical cost of leaving a family home.

- What is NHS Continuing Healthcare?

- NHS Continuing Healthcare (CHC) is fully NHS-funded long-term care for adults whose primary need is health-related rather than social. If awarded, the NHS pays the entire cost - fees, accommodation, personal care and nursing - anywhere you receive care, with no means test on capital or income. Eligibility hinges on a Decision Support Tool assessment that scores 12 care domains; you typically need one "priority" score, two "severes", or a combination representing a "primary health need". Refusal is common but appealable. About 60,000 people in England are in receipt, split roughly between 51,000 standard and 9,000 fast-track (end-of-life) packages.

- Can I get a mortgage in retirement?

- Yes - and an increasing number of UK retirees do. Lenders offer several products: standard residential mortgages where pension income is treated as affordable, retirement interest-only (RIO) mortgages where you pay interest only and the capital is repaid when you sell or die, lifetime mortgages where interest rolls up, and term extensions on an existing mortgage. The right answer depends on income, age, the size of the remaining balance and whether you want to leave the property to children. Many retirees use their 25% tax-free pension lump sum to clear a small remaining balance - straightforward, but it depletes a tax-advantaged pot that could otherwise pass to family inheritance-tax-free.

- How do I help my elderly parents manage their money?

- Three priorities, in order. First, run a benefits check - many older people miss out on Attendance Allowance (£114.60/week higher rate in 2026/27), Pension Credit (gateway to Council Tax Reduction, free TV licence and Cold Weather Payments), and free NHS prescriptions. Second, set up Lasting Powers of Attorney while they still have capacity - both Property and Financial Affairs, and Health and Welfare. Third, sort out banking access - most UK banks now offer formal third-party access arrangements that are safer and more transparent than informal sharing of PINs and cards. Avoid joint accounts unless you understand the inheritance tax and means-test consequences.