State Pension & Benefits

The State Pension is the foundation of most UK retirement plans. This hub explains what you will get in the 2026/27 tax year, when you can claim, how Pension Credit tops up low incomes, and the other benefits that come with reaching State Pension age - with links to deeper guides for each topic.

- 1 Approaching retirement and want to know what you will actually get→ Get a free State Pension forecast at gov.uk/check-state-pension, then read our guide to what £241.30 a week means in practice and how NI years map to the figure on the page.

- 2 Wondering when you can claim - or whether to delay→ Check your exact State Pension age (it is in the middle of a 66 → 67 transition). If you can comfortably wait, deferring the new State Pension adds about 5.8% a year for life.

- 3 Worried about a small pension or low income in retirement→ Run a Pension Credit check. The qualifying line is £238 a week single, £363.25 a couple in 2026/27 - and even a few pence award unlocks gateway benefits worth far more.

- 4 Have savings and unsure whether you still qualify for Pension Credit→ Read our savings-rules guide. The first £10,000 of capital is fully ignored; only deemed income on amounts above that counts. People are routinely wrongly told they would fail the test.

- 5 Helping an elderly parent claim what they are entitled to→ Work through the benefits-for-pensioners checklist - Attendance Allowance, Council Tax Reduction, free TV licence at 75, NHS help, Warm Home Discount and the Winter Fuel Payment.

What is the State Pension?

The State Pension is the UK’s public retirement income. It is paid by the Department for Work and Pensions out of current National Insurance receipts - a pay-as-you-go system, not a personal savings pot - and once you qualify it is paid to you every four weeks for the rest of your life. It rises every April under the triple lock, can be inherited in part by a surviving spouse or civil partner, and is taxable but always paid gross with no tax taken at source.

What it is not: it is not means-tested, it does not depend on where you live now (you can draw it abroad, though uprating only applies in some countries), and it is not based on how much you earned. The only thing that determines your entitlement is your National Insurance record - the years of paid contributions and credits that build up on your NI file over your working life. That distinction is what makes the State Pension different from Pension Credit, which is a means-tested top-up for low retirement incomes.

Around 12.7 million people receive a State Pension today, and for roughly half of pensioner households it makes up more than half of their gross income (DWP, Pensioners’ Incomes Series, latest release). For many lower-earning workers it will be the single largest financial asset of their lives - a 65-year-old qualifying for the full new rate today is, in present-value terms, sitting on around £250,000 of guaranteed inflation-linked income.

The new State Pension explained

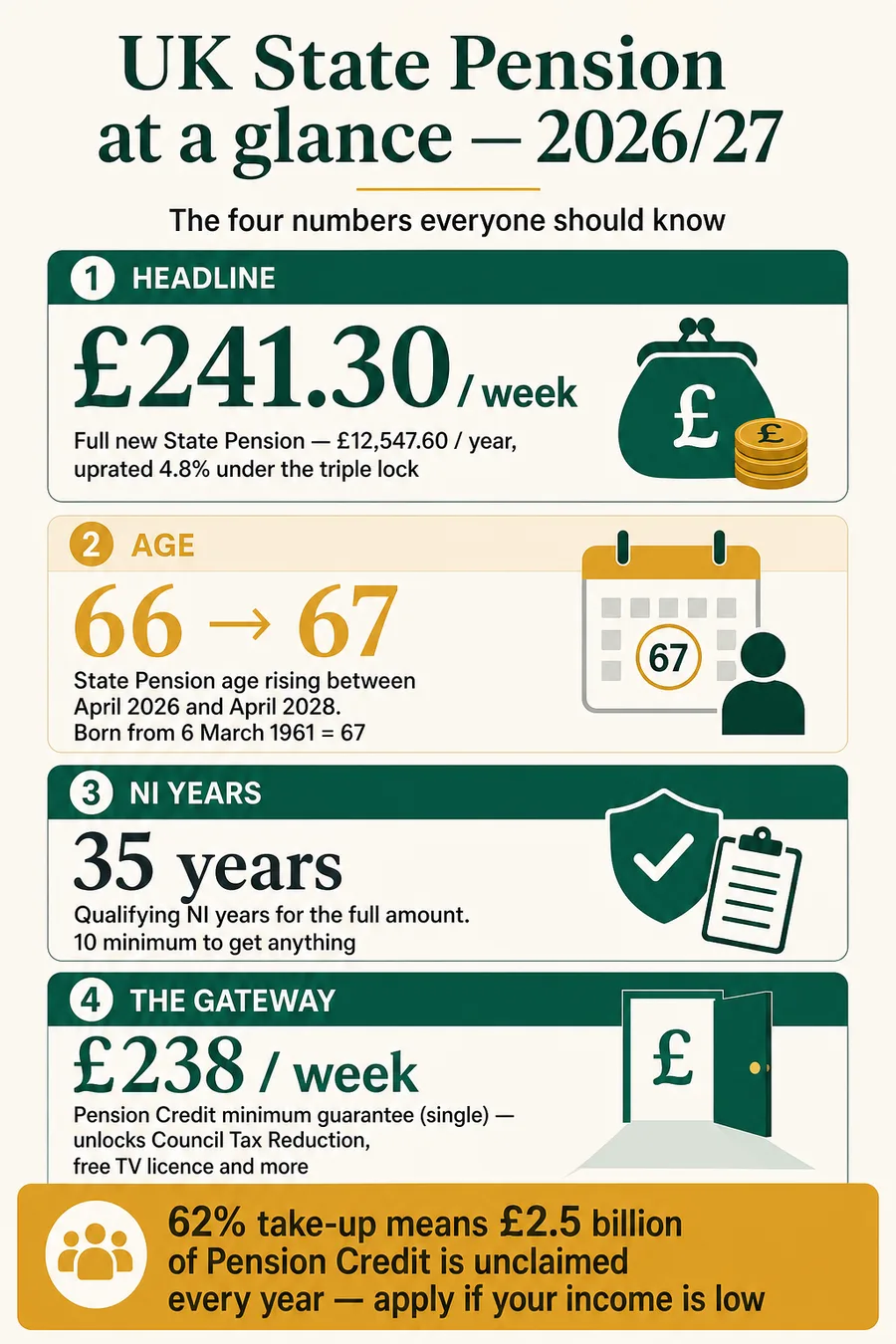

Anyone reaching State Pension age on or after 6 April 2016 is on the new State Pension. It replaced the old two-tier system (basic State Pension plus the earnings-related SERPS / S2P add-on) with a single, simpler flat rate. For 2026/27 that rate is £241.30 a week, or £12,547.60 a year, paid into your bank account every four weeks in arrears.

The new State Pension is broadly proportional to the number of qualifying NI years you hold, up to a cap of 35:

- 35 or more qualifying years → the full £241.30 a week (you cannot exceed the cap by working longer, though deferral adds an uplift).

- 10-34 qualifying years → a pro-rata amount. Each year is worth 1/35th of £241.30 - about £6.89 a week, or roughly £358 a year of extra State Pension for life.

- Fewer than 10 qualifying years → no new State Pension at all. Pension Credit may still be payable on a means-tested basis.

Qualifying years are not just paid contributions. They include NI credits for parents claiming Child Benefit for a child under 12, for carers in receipt of Carer’s Allowance or Carer’s Credit, for people on Jobseeker’s Allowance or Employment and Support Allowance, and for grandparents looking after a working parent’s under-12 (Specified Adult Childcare Credits). One of the most common reasons people’s forecasts are lower than they expect is that Child Benefit was claimed in the other partner’s name, so the NI credits sat with the higher earner who did not need them.

A second gotcha is contracting out. Between 1978 and April 2016 millions of workers contracted out of the additional State Pension through a workplace defined-benefit scheme, paying lower NI in exchange for a guaranteed minimum pension in their employer’s plan. When the new system started in April 2016, DWP calculated a "starting amount" - the higher of what you would have got under old rules or new rules - and deducted a Contracted-Out Pension Equivalent (COPE) to reflect the workplace pension making up for it. People with a long contracted-out history typically see a forecast below £241.30 even with 35+ NI years; the "missing" amount is paid by the workplace scheme. The full mechanics and a forecast walk-through are in how much State Pension will I get.

State Pension age - the moving target

State Pension age is the earliest day you can claim. It depends only on your date of birth and as of May 2026 sits in the middle of a phased rise from 66 to 67. Under the Pensions Act 2014:

- Born before 6 April 1960 - State Pension age was 66. You have already reached it; if you have not yet claimed, you can backdate up to 12 months or carry on deferring.

- Born 6 April 1960 - 5 March 1961 - in the transitional band. Your State Pension age is somewhere between 66 years 1 month and 66 years 11 months, with the exact date set by month-by-month birth-date bands. You will reach it between May 2026 and February 2028.

- Born 6 March 1961 - 5 April 1977 - State Pension age 67. You reach it on your 67th birthday.

- Born from 6 April 1977 - planned State Pension age 68, currently legislated under the Pensions Act 2007 to take effect between 6 April 2044 and 5 April 2046.

What is legislated is not always what ends up happening. The 2023 government review of State Pension age, led by Baroness Neville-Rolfe, recommended bringing the rise to 68 forward to 2041-2043. The government rejected that, saying it would hold a further review "within two years of the next Parliament" - meaning by 2026-2027. As of today (16 May 2026) that review has not reported. If you were born in the late 1970s or in the 1980s, plan for a State Pension age of at least 68, and accept that the date it kicks in could move. The detailed birth-date bands and inline calculator are in State Pension age 2026: when can I claim?.

Pension Credit - the master key

Pension Credit is the most under-claimed benefit in the UK. It tops up the income of pensioner households below a guaranteed minimum - £238 a week for a single person and £363.25 a week for a couple in 2026/27 - and is paid by DWP on a means-tested basis, not based on NI history. Pure income terms, it adds up to roughly £12,376 a year for a single pensioner with no other income.

What makes it disproportionately valuable is that it is a gateway benefit. An award, even of a few pence a week, automatically unlocks:

- Council Tax Reduction (often a full discount, set by your local authority)

- A free TV licence from age 75

- The Warm Home Discount (£150 off the electricity bill)

- NHS exemptions - free prescriptions, dental treatment, eye tests, vouchers for glasses

- Cold Weather Payments (£25 per qualifying week)

- Help with mortgage interest (as a loan) or full Housing Benefit if you rent

Yet DWP’s own statistics show take-up running at around 62% - meaning roughly four in ten eligible households do not claim, leaving an estimated £2.5 billion unclaimed each year. The Pension Credit eligibility guide covers the rules, the savings disregards (often misunderstood - see also the £10,000 savings rule), and how to apply.

The triple lock

Since 2011 the State Pension has been protected by the triple lock, a political commitment that the basic and new State Pensions rise every April by whichever is highest of three measures:

- September CPI inflation

- May-July average weekly earnings (AWE) growth

- 2.5% as a floor

For 2026/27, September 2025 CPI was 1.7%, May-July 2025 AWE growth was 4.8% and the floor was 2.5%. Earnings won, producing the 4.8% uplift that took the full new State Pension to £241.30. The mechanism is the reason pensioners typically see bigger uprates than working-age benefits, which only follow inflation. It is a manifesto pledge, not a permanent statute, and has been suspended once (2022/23). Plan as if it remains in place, but do not assume the formula is untouchable across multi-decade horizons.

The Personal Allowance trap

The income tax Personal Allowance is frozen at £12,570 until at least April 2028 (extended from the original 2025/26 freeze in successive Budgets). The full new State Pension is now £12,547.60 - leaving just £22.40 of headroom before any other income is taxed at 20% from the very first pound. Any workplace pension, annuity, part-time job or savings interest above the personal savings allowance sits fully on top. If the triple lock outpaces frozen thresholds for one more year, the State Pension on its own crosses into tax. The mechanics, including how HMRC collects the tax through a reduced code on your other PAYE income, are covered in State Pension and tax.

Guides in this section

Six in-depth guides covering state pension & benefits for the 2026/27 tax year.

- 01 State Pension age is rising: 66 to 67 in 2026-28 - check yours

State Pension age is rising from 66 to 67 between April 2026 and April 2028. Check the exact date for your birth month and the full timetable.

Read guide → - 02 How much is the State Pension? £241.30 a week in 2026/27

The full new State Pension is £241.30 a week (£12,547.60 a year) in 2026/27. How many qualifying NI years you need and how to check your forecast on GOV.UK.

Read guide → - 03 State Pension deferral explained

How deferring the State Pension works under the new rules, how much extra you get, and when deferral is - and is not - worth it.

Read guide → - 04 Pension Credit eligibility 2026/27

Pension Credit tops up low retirement incomes. See the 2026/27 rates, savings rules, and how to apply through GOV.UK.

Read guide → - 05 Can I get Pension Credit if I have savings?

How savings affect Pension Credit, the £10,000 threshold, deemed income, and worked examples for couples and single pensioners.

Read guide → - 06 What benefits can pensioners claim in the UK?

A plain-English checklist of UK benefits older people may be entitled to - from Pension Credit and Attendance Allowance to Council Tax Reduction and the Winter Fuel Payment.

Read guide →

Frequently asked questions

- How much is the UK State Pension in 2026?

- In the 2026/27 tax year the full new State Pension is £241.30 a week - £12,547.60 a year - paid every four weeks in arrears. The full basic State Pension (for people who reached State Pension age before 6 April 2016) is £184.90 a week, or £9,614.80 a year. Both rates rose by 4.8% from 6 April 2026 under the triple lock, with the increase set by May-July 2025 average weekly earnings growth.

- When can I claim my State Pension?

- You can claim from your personal State Pension age, which depends only on your date of birth. State Pension age is currently rising from 66 to 67 between 6 April 2026 and 5 April 2028 under the Pensions Act 2014. If you were born before 6 April 1960 it was 66. If you were born between 6 April 1960 and 5 March 1961 you are in the transitional band - somewhere between 66 years 1 month and 66 years 11 months. If you were born between 6 March 1961 and 5 April 1977 it is 67. Use GOV.UK’s "Check your State Pension age" tool for the exact date.

- How many years do I need for a full State Pension?

- For the full new State Pension you usually need 35 qualifying years of National Insurance contributions or credits, and at least 10 to get anything. Qualifying years can come from paid Class 1, Class 2 or Class 3 contributions, or from NI credits - for example while claiming Child Benefit for a child under 12, receiving Carer’s Credit, or on certain working-age benefits. The old basic State Pension required 30 qualifying years for the full rate. Always check your forecast at gov.uk/check-state-pension because pre-2016 contracted-out service can change your starting amount.

- Is the State Pension going up in 2026?

- Yes. From 6 April 2026 the full new State Pension increased by 4.8% - from £230.25 to £241.30 a week - and the full basic State Pension rose from £176.45 to £184.90. Triple-lock arithmetic took the highest of CPI inflation (1.7% in September 2025), May-July 2025 average weekly earnings growth (4.8%) and the 2.5% floor, so earnings set the uplift. DWP and HMRC apply the new rate automatically; existing pensioners do not need to claim.

- Can I get the State Pension and a private pension at the same time?

- Yes. The State Pension is paid in addition to any workplace or personal pension you have built up - they are completely separate systems. You can normally access a defined-contribution pension from age 55 (rising to 57 from 6 April 2028) with the first 25% tax-free, while the State Pension starts from your State Pension age. Both count as taxable income and are stacked together for income tax, which matters because the £12,570 personal allowance is frozen until at least April 2028.

- What is Pension Credit and how does it differ from the State Pension?

- Pension Credit is a means-tested top-up benefit that brings a low pensioner income up to a guaranteed minimum - £238 a week for a single person and £363.25 for a couple in 2026/27. Unlike the State Pension, which is based on your National Insurance record, Pension Credit looks at your current income and capital, regardless of how much NI you have paid. It is also a gateway benefit: even an award of a few pence a week unlocks Council Tax Reduction, a free TV licence at 75, NHS exemptions, Cold Weather Payments and the Warm Home Discount. DWP estimates around 62% of eligible households claim it - about £2.5bn goes unclaimed each year.

- Do I pay tax on my State Pension?

- Yes, the State Pension is taxable income - but it is paid gross, with no tax taken off at source. HMRC instead collects any tax due by reducing the tax code on your other PAYE income such as a workplace pension or part-time job. In 2026/27 the full new State Pension is £12,547.60 a year and the personal allowance is frozen at £12,570 - leaving only £22.40 before any other income is taxed at 20%. If the State Pension is your only income you currently pay no tax, but a future uprating that takes it above £12,570 would create a small Simple Assessment bill unless allowances rise too.

- Will the State Pension age rise to 68?

- Under current legislation (Pensions Act 2007, as amended) State Pension age is scheduled to rise from 67 to 68 between 6 April 2044 and 5 April 2046, affecting people born from 6 April 1977. The 2023 government review chose not to bring this forward, despite Baroness Neville-Rolfe’s independent review recommending 2041-2043. The government committed to a further review within two years of the next Parliament. As of May 2026 the 2044-2046 timetable still applies, but it is the most likely part of the system to change for anyone in their 40s today.