TL;DR - the headline numbers for 2026/27

Long-term care in the UK is means-tested, not free at the point of use. The NHS pays only if your needs are primarily medical (NHS Continuing Healthcare) or if a registered nurse provides regular care (NHS-Funded Nursing Care). For everything else - the typical residential or dementia care home placement - you pay until your assessable capital falls below your nation's upper threshold, at which point the local authority takes over a tapered share.

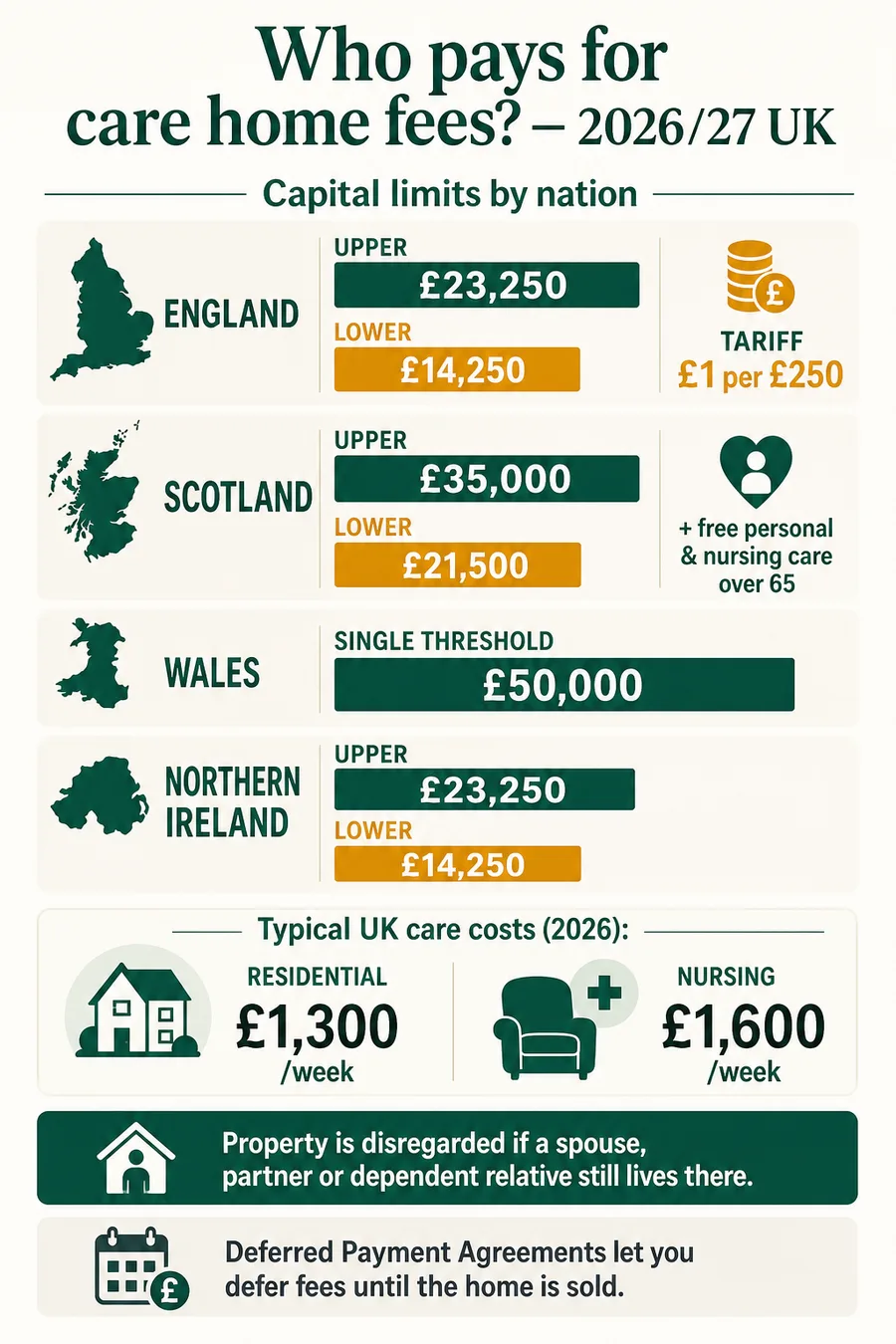

Five numbers anchor every other paragraph on this page. The England and Northern Ireland capital limits are £23,250 upper / £14,250 lower for 2026/27 - unchanged since April 2010 in cash terms and not scheduled to change. Scotland uses £35,000 / £21,500. Wales has a single flat £50,000 capital limit, the highest in the UK. Average self-funder fees, per LaingBuisson's Care of Older People market report, are around £1,300/week residential and £1,600/week nursing. And around 60,000 people in England receive NHS Continuing Healthcare at any time - fully NHS-funded care, the single most valuable entitlement to test for early (see NHS England's CHC quarterly statistics).

The DHSC charging reform announced in 2021 - which would have raised the England upper capital limit to £100,000 and introduced an £86,000 lifetime care-cost cap - was cancelled in July 2024 by the incoming government and is not in the current legislative programme. The longstanding £23,250/£14,250 limits therefore continue for 2026/27. An independent commission (Casey, due to report in 2028) will examine future reform; nothing in front of Parliament right now changes the rules below.

Who pays for your care? A 30-second decision tree

Use this to triage your situation. The single most important early step is to ask the local authority for a needs assessment under the Care Act 2014 (England), Social Services and Well-being (Wales) Act 2014, Social Care (Self-directed Support) (Scotland) Act 2013, or the equivalent NI framework. The assessment is free, statutory, and triggers your right to a financial assessment, deferred payment agreement, and NHS CHC checklist.

- 1 You own your home and have savings above the capital limit (£23,250 England/NI, £35,000 Scotland, £50,000 Wales)→ You are a self-funder. You pay the full bill until your assessable capital falls below the upper limit. Ask the council for an assessment anyway - it triggers your right to a deferred payment agreement and to NHS Continuing Healthcare screening.

- 2 Your needs are primarily health (not social) - e.g. advanced dementia, end-of-life→ Request an NHS Continuing Healthcare (CHC) assessment. If awarded, the NHS pays your full care fees - fees, accommodation and personal care - regardless of capital. Only around 60,000 people are in receipt at any time, but applying is free.

- 3 A spouse, partner, dependent child or qualifying relative still lives in your home→ The value of your home is disregarded. Many self-funders are reclassified as council-funded the moment a spouse or qualifying relative is correctly identified. Do not let the council count the house if any disregard applies.

- 4 You need nursing care delivered by a registered nurse→ The NHS pays a flat Funded Nursing Care (FNC) contribution direct to the home - £254.06/week in England (2025/26). It is paid on top of any local-authority funding or self-pay, and is automatic once an assessment confirms registered-nursing input.

- 5 Your capital is between the upper and lower thresholds→ You pay a tapered contribution. England, Scotland and NI add £1/week of tariff income for every £250 of capital above the lower limit, on top of your real income. Wales has a single £50,000 cliff - above it you pay all, below it the council means-tests income only.

Four-nation comparison: capital limits, tariff income, NHS contributions

Adult social care is fully devolved, and the differences between the four nations are substantial. The table below is the page in one block - capital thresholds, how tariff income works in each, and any NHS-funded contribution paid on top.

| Nation | Upper limit | Lower limit | Tariff income | NHS extras |

|---|---|---|---|---|

| England | £23,250 | £14,250 | £1/wk per £250 | NHS FNC £254.06/wk if nursing; 12-week property disregard |

| Scotland | £35,000 | £21,500 | £1/wk per £250 | Free Personal Care £248.70/wk (65+); FNC £111.90/wk |

| Wales | £50,000 | £50,000 | No tariff income - flat cliff | NHS-Funded Nursing ~£197.20/wk; £100/wk max for home care |

| Northern Ireland | £23,250 | £14,250 | £1/wk per £250 | Registered Nursing Care Contribution paid separately |

Two notes are worth pulling out. First, the Wales £50,000 limit has no tariff-income taper - it is a single cliff. Above £50,000 you pay everything; below it the council means-tests your income only. Second, Scotland's "free personal care" is a fixed weekly payment to the home, not free residential care: hotel costs (accommodation, food, heating) still come from your own pocket subject to the £35,000/£21,500 capital test.

How the England means test works in detail

If you live in England (the rules in Northern Ireland are materially the same) the council's financial assessment runs in three steps. The first is the capital test. The council adds up your assessable savings, investments, second properties and (where the disregards do not apply) your main home. Above £23,250 you pay the full cost. Below £14,250 your capital is ignored entirely - only your income counts. Between the two limits the council applies tariff income of £1 a week for every £250 of capital above the lower limit. Note the figure: it is £1 per £250, not the £1-per-£500 used in Pension Credit. Many websites (and some advisers) still misquote it - always check against the DHSC's Care and Support Statutory Guidance.

The second step is the income test. The council adds up your State Pension, any private pensions, annuity income, certain investment income and Attendance Allowance (for self-funders only). It then deducts a statutory Personal Expenses Allowance (PEA) of £32.65 a week - your "spending money" - and any guaranteed disregard for half of an occupational pension paid to a spouse remaining at home. What is left is your assessable weekly income.

Step three is the contribution calculation. The council pays the difference between your assessable income (plus any tariff income) and the home's contracted weekly fee. If your assessable income exceeds the contracted fee, you pay all of it and the council pays nothing. If you are a self-funder (capital above £23,250), the council does not contribute at all, regardless of how high your fees are or how fast your savings are eroding.

A common mistake: assuming tariff income uses the Pension Credit rule of £1 per £500. It does not. The care-home rule is twice as harsh - £1 per £250. On £20,000 of capital that means £23/week of deemed income (£20,000 − £14,250 = £5,750 → £24/wk). On £22,000 it means £31/week. Get this wrong and you will under-estimate your contribution by £1,000-£1,500 a year.

Inline means-test calculator

Enter your capital, weekly income and the home's weekly fee. The calculator applies the current capital limits, tariff-income rule, personal-expenses allowance and (where applicable) Scotland's free personal care or England's Funded Nursing Care offset. This is an estimate - your council will give you a definitive figure after a formal financial assessment - but it usually lands within a few pounds a week of the official number.

Estimate only. Excludes Pension Credit, savings credit gateway effects and means-test disregards for half of an occupational pension paid to a spouse remaining at home. For an exact figure use the entitledto care-fees tool or request a formal financial assessment from your local council.

The property disregard - when your home doesn't count

The single biggest variable in any care-home means test is whether the value of your home counts as capital. For a sole homeowner moving permanently into a care home, the answer is usually yes - but there are five statutory disregards that override the default, and they recategorise many would-be self-funders as council-funded the moment they are correctly identified.

The council ignores your main home if any of these people still live in it as their main residence:

- Your spouse, civil partner or unmarried partner

- A relative aged 60 or over

- A relative who is incapacitated (any age)

- A dependent child under 16 you are liable to maintain

- A former partner who is a lone parent (England discretionary)

The disregard runs for as long as the qualifying person lives there. The moment they leave, the property becomes assessable capital. Make sure the council records the disregard explicitly - do not assume they have noticed.

For a single person with no qualifying co-resident, the home is included as capital but only after a mandatory 12-week property disregard. During those 12 weeks the council treats you as if you owned no property and pays toward your fees on income alone. The 12-week window exists to let families arrange a sale, a tenancy or a deferred payment agreement without panic. Use it. Many families either do not know it exists or fail to invoke it formally - the council will not always volunteer it.

Deferred Payment Agreement - borrowing from the council

A Deferred Payment Agreement (DPA) is a statutory loan from the local authority secured against your home. The council pays your care fees (up to the contracted rate, not the self-funder rate); you accrue a debt that is repaid when the property is sold - typically after death. DPAs are universal in England under the Care Act 2014 and are mirrored in the other nations under broadly similar rules.

- You must own (or part-own) the property, with your name on the title.

- Your non-property capital must be below £23,250 - otherwise you can pay from savings first.

- The total deferred amount cannot exceed roughly 90% of the home's equity value (council retains a buffer for fees and sale costs).

- Interest accrues at the DHSC-published rate - currently 3.31% (15-year gilts plus 0.15%, reviewed every 6 months).

- The council can charge a one-off admin fee, typically £500-£1,500 plus the cost of the legal charge.

- You retain the right to rent the property out during the agreement, which can offset some or all of the interest.

Compared with the alternatives - equity release, an emergency sale, or borrowing from family - the DPA is almost always the cheapest source of funding. A lifetime mortgage in 2026 carries interest at 6.5-7.5% on a rolled-up basis; the council's 3.31% is less than half that. The main caveat is that DPAs use the contracted (council-rate) fee, not the self-funder fee - so the home must agree to charge that rate, which is not automatic and may require negotiation.

NHS Continuing Healthcare - the most valuable entitlement to test for

If a person's primary need is health, not social, the entire cost of their care - fees, accommodation, personal care and nursing - is paid by the NHS, regardless of capital, income or property. This is NHS Continuing Healthcare (CHC). It is the single most valuable entitlement in the long-term-care system. It is also the most poorly understood and most frequently refused.

A registered nurse and a social worker jointly score the person against a Decision Support Tool across 12 care domains: behaviour, cognition, communication, mobility, nutrition, continence, skin, breathing, drug therapies, altered state of consciousness, psychological and emotional needs, and "other significant needs". Each domain is graded from "no needs" to "priority" (or "severe" for those without a priority option). Eligibility typically requires:

- One "priority" score, or

- Two "severe" scores, or

- A combination that, taken together, represents a "primary health need" - a needs profile that is intense, complex or unpredictable.

Fast-track assessment is available for rapidly deteriorating conditions (typically end-of-life). Approximately 60,000 people in England are in receipt at any time (NHS England Q4 2024 figures: roughly 51,000 standard plus 9,000 fast-track).

The application process is rigorous and refusal is common. Three actions raise the success rate materially. First, insist on a CHC Checklist before signing any self-funder contract - the screening tool is free, the threshold to progress is low, and it costs nothing to do. Second, prepare evidence: the assessment is meant to be evidence-based but families who arrive with care diaries, GP letters and medication lists score better than those who do not. Third, use a specialist if needed. Charities such as Age UK and Beacon, and regulated solicitors with CHC expertise, offer free initial advice and contingent-fee representation for appeals. Retrospective claims (for care fees wrongly self-paid in the past) can run into tens of thousands of pounds.

NHS-Funded Nursing Care - a flat-rate top-up

Where care is delivered in a nursing home (not residential) and includes input from a registered nurse, the NHS pays a flat weekly NHS-Funded Nursing Care (FNC) contribution direct to the home. It applies whether you are self-funding, council-funded or anything in between. It is not means-tested. In England the 2025/26 rate is £254.06 a week (£13,211/year) and is reviewed annually. Wales pays a single combined rate of around £197.20/week; Northern Ireland uses a separate Registered Nursing Care Contribution.

FNC is automatic once an assessment confirms that registered-nursing input is part of your care plan. You should not have to apply separately - the home initiates it. Check your weekly invoice: the FNC contribution should be shown as a deduction, not absorbed silently into the home's headline fee.

Scotland: free personal and nursing care

Scotland has the most generous long-term-care settlement in the UK. Free Personal and Nursing Care was introduced in 2002 and remains in force. The Scottish Government pays the care home a flat weekly contribution for personal care (£248.70/week in 2025/26 for residents aged 65+) and, where nursing care is provided, a further £111.90/week. Both payments go straight to the home and reduce the headline bill you face.

What remains is the "hotel cost" - accommodation, food, heating, ancillary services - and that is means-tested against the Scottish capital limits of £35,000 / £21,500. So a Scottish resident in a £1,400/week home with capital below £21,500 pays only the income-based contribution toward hotel costs (after a £33.65 personal allowance); a self-funder with £80,000 of savings still pays around £1,000/week (£1,400 − £249 − £112 nursing if applicable, plus £39 hotel-cost contribution).

Wales and Northern Ireland

Wales has the simplest rules. A single flat capital limit of £50,000 - the highest in the UK - replaces England's two-tier system entirely. Above £50,000 of capital you pay everything; below it the council means-tests your income only, with no tariff income on capital. Domiciliary care (care at home, not in a residential setting) is capped at £100/week regardless of need or income. Wales pays an NHS-Funded Nursing Care contribution of approximately £197.20/week.

Northern Ireland mirrors England with capital limits of £23,250 / £14,250, the same £1-per-£250 tariff-income rule, and a Registered Nursing Care Contribution paid separately by the Department of Health. The means test runs through Health and Social Care Trusts rather than local authorities, but the financial mechanics are effectively the same as in England.

Three real scenarios

Situation: Doris is widowed, lives alone, and is moving into a residential home in West Yorkshire after a fall. The home charges £1,250/week. She owns her two-bedroom semi (estimated value £180,000) and has £36,000 in cash ISAs and current accounts. Her weekly income is her State Pension £221.20 plus a £42/week private pension.

- 12-week property disregard: for the first 12 weeks the council pays toward her fees on income alone. With £36,000 of non-property capital (above £23,250) she still pays the assessable portion of her income (£263 − £32.65 PEA = £230/week), and the council covers the difference (£1,250 − £230 = £1,020/week).

- Week 13 onwards: the house counts as capital. Combined assessable capital is £216,000, well above £23,250. Doris becomes a self-funder paying the full £1,250/week. At that rate her £36,000 lasts about 9 months before the house must be sold or a deferred payment agreement signed.

- Deferred Payment Agreement: Doris signs a DPA at the start of week 13. The council pays the home's contracted rate (negotiated down to £1,050/week - the council-rate). Interest accrues on the debt at 3.31%. Doris keeps the house rented out (net £900/month) which more than offsets the interest.

- Attendance Allowance: Doris applies for the higher rate (£114.60/week = £5,959/year) - as a self-funder it continues throughout her stay and offsets the fees.

Result: Doris keeps the house, defers the sale, and the family ultimately settles a ~£90,000 debt out of sale proceeds rather than facing a forced sale in month 13.

Situation: Frank has advanced Parkinson's and is moving into a nursing home charging £1,650/week. Elsie, his wife, remains in their owner-occupied home in Surrey (value £550,000). They have £62,000 in joint savings. Frank's State Pension is £221.20/week plus a £180/week occupational pension.

- Property disregard - automatic: Elsie still lives there, so the house is disregarded indefinitely. Joint savings are usually halved for assessment, giving Frank £31,000 - still above £23,250.

- Occupational pension split: 50% of Frank's £180/week occupational pension is disregarded if paid voluntarily to Elsie. Frank's assessable income falls to £221.20 + £90 = £311.20, minus £32.65 PEA = £278.55/week.

- NHS-Funded Nursing Care: at £254.06/week, the NHS pays the home direct. Frank's net fee falls to £1,396/week.

- Self-funder contribution: capital still above £23,250, so Frank pays the full £1,396/week from income and savings combined. Savings deplete by roughly £58,000/year.

- NHS CHC application: with advanced Parkinson's and complex care needs, Frank's family request a CHC assessment immediately. If awarded, the NHS pays the full £1,650/week and savings are protected. Worth applying for - many Parkinson's-with-dementia cases meet the "primary health need" test.

Result: the £550,000 house is fully protected for Elsie. Frank's contribution is around £58,000/year - but with NHS CHC potentially payable, the assessment is the highest-value action of the year.

Situation: Iain moved into residential care in Glasgow after a stroke. The home charges £1,350/week. His capital is £19,000 (below the Scottish lower limit of £21,500 - capital ignored). Weekly income: State Pension £221.20 + private pension £55.

- Free Personal Care: Scottish Government pays the home £248.70/week direct.

- Capital below lower limit: capital ignored entirely. Only income counts.

- Assessable income: £276.20 − £33.65 personal allowance = £242.55/week toward hotel costs.

- Iain pays: £242.55/week (the council pays the difference between hotel cost and Iain's contribution).

- Annual cost to Iain: roughly £12,613/year - versus a notional £70,200 if he were a full self-funder. Scotland's free personal care plus the lower capital test save him £57,000 a year compared with an English equivalent on the same income.

Result: Iain's combined Free Personal Care + below-threshold capital means the bulk of his fees are publicly funded. Scotland's settlement is materially more generous than England's for residents in this income/capital bracket.

The self-funder cross-subsidy - why private payers pay more

Local authorities commission care home places at rates set by their commissioning teams. Across England the average council-commissioned residential fee in 2024/25 was around £850-£950/week; self-funders in the same homes paid an average of £1,100-£1,300/week. The difference - typically £200-£250/week or £10,000-£13,000/year - is the so-called self-funder cross-subsidy. Care homes use it to recover the gap between commissioning rates (often below the true cost of care) and the long-run cost of running the home.

The Competition and Markets Authority documented the practice in its 2017 market study, and follow-up DHSC analysis in 2023 confirmed the gap had widened. Funding reforms intended to equalise rates were postponed indefinitely in July 2024.

What to do: always ask the home for both their self-funder and council-commissioned weekly rates in writing. Negotiate: many homes will discount privately for guaranteed long-stay residents. If your capital is approaching £23,250, ask the council to start a financial assessment before you cross the threshold - when you become council-funded the home is contractually bound to accept the council rate for your bed.

Planning tools - what works, what doesn't

Three categories of tool come up repeatedly when families plan for care costs. None is a silver bullet, and one is largely a marketing exercise.

- Immediate-needs annuities (care fees annuities): a one-off lump sum buys a guaranteed income paid directly to the home for life. Quotes are sharply medically underwritten - the higher the assessed mortality, the more income per £1 of premium. Useful when capital is around £100,000-£250,000, the resident is in poor health and the family wants certainty. Not useful for younger, healthier residents (the rate of return is poor) or where the resident is likely to live many more years (the cap on income is fixed).

- Equity release / lifetime mortgages: raising capital from a home where a spouse remains. Useful in a narrow set of circumstances - typically where the property disregard already protects the home and the family wants liquidity for additional services. Almost always more expensive than a Deferred Payment Agreement for the resident leaving the home. Read our lifetime mortgages explainer before signing anything.

- "Asset protection" trusts and gifting: heavily marketed; rarely useful; frequently dangerous. Councils have wide powers under the deliberate deprivation of capital rules to disregard transfers made with the intent of avoiding care fees, regardless of the seven-year IHT rule. A property gifted to children remains assessable capital if the gifting was foreseeably linked to care needs. Take regulated advice before any transfer.

Frequently asked questions

- Who pays for care home fees in the UK?

- It depends on your assessable capital, your nation, and the nature of your needs. In England and Northern Ireland the council pays toward your care if your capital is below £23,250; you pay the full cost above that threshold. Scotland uses £35,000 (and pays a Free Personal Care contribution of around £248.70/week to all over-65s in residential care). Wales has a single £50,000 capital limit - below it the council means-tests your income; above it you pay in full. If your needs are primarily medical rather than social you may qualify for NHS Continuing Healthcare, which covers the full cost regardless of capital. About 60,000 people in England are in receipt at any time.

- How much does a care home cost in the UK in 2026?

- LaingBuisson's 2025/26 Care of Older People report puts the average self-funder residential fee at around £1,300 a week (£67,600/year) and nursing care at around £1,600 a week (£83,200/year). The South-East and London run 20-35% higher; the North East and Northern Ireland run 15-25% lower. Self-funders typically pay £200-£250 a week more than the local-authority commissioned rate for the same bed - the so-called cross-subsidy. Specialist dementia nursing units can exceed £1,800/week. Always ask the home for both the self-funder weekly fee and the council-commissioned rate, in writing, before you sign.

- What is the care home means test capital limit in 2026?

- In England and Northern Ireland the upper capital limit is £23,250 and the lower limit is £14,250. Above £23,250 you pay the full cost yourself. Between the two limits the council adds £1 a week of "tariff income" for every £250 of capital above £14,250. Below £14,250 your capital is ignored entirely - only your real income (State Pension, private pensions, etc.) counts. Scotland uses £35,000/£21,500; Wales has a single £50,000 flat capital limit. The original DHSC plan to raise the England upper limit to £100,000 from October 2025 was cancelled in July 2024 and is not on the current government's legislative programme.

- Does my house count toward the care home means test?

- It depends on who else lives there. The value of your home is fully disregarded if any of the following remain living in it as their main residence: your spouse, civil partner or unmarried partner; a relative aged 60+; a relative who is incapacitated; a dependent child under 16 you are liable to maintain. If none of those apply (typical of a widowed or single homeowner moving permanently into care), the house is included as capital but only after a mandatory 12-week disregard. During those 12 weeks the council pays toward your fees as if you had no property, giving you time to arrange a sale or a deferred payment agreement.

- What is a deferred payment agreement and how much does it cost?

- A deferred payment agreement (DPA) lets you postpone selling your home to pay for care. The council pays your fees and registers a legal charge against the property; the debt is repaid when the property is eventually sold (often after death). DPAs are available in England to anyone whose home is included in the means test, whose other assets are below £23,250, and who has consented. The council charges interest at the DHSC-published rate - currently 3.31% (effective July 2025-January 2026), reviewed every six months and pegged to 15-year gilts plus 0.15%. Councils may also charge a one-off administration fee, typically £500-£1,500. Compared with selling under time pressure, or taking equity release, the DPA is usually the cheapest way to defer.

- What is NHS Continuing Healthcare and who qualifies?

- NHS Continuing Healthcare (CHC) is fully NHS-funded care for adults whose primary need is health-related rather than social. If awarded, the NHS pays the full cost of care - including accommodation, personal care and nursing - anywhere you choose to receive it, and irrespective of your savings or income. Eligibility hinges on a "Decision Support Tool" assessment that scores 12 care domains (behaviour, cognition, communication, mobility, nutrition, continence, skin, breathing, drug therapies, altered state of consciousness, psychological and emotional needs, other significant needs). You usually need a "severe" in one priority domain, two "severes" overall, or a combination that adds up to a "primary health need". About 60,000 people in England are in receipt at any time. The application process is rigorous and refusal rates are high - Age UK, Beacon and CHC specialists offer free or contingent-fee advocacy.

- What is NHS-Funded Nursing Care?

- NHS-Funded Nursing Care (FNC) is a flat-rate weekly payment from the NHS direct to a nursing home to cover the cost of registered-nurse input. In England the rate for 2025/26 is £254.06 a week (rising broadly in line with NHS pay). It is paid for anyone in a nursing home (not residential) whose care requires a registered nurse and who is not on full NHS Continuing Healthcare. FNC is automatic once a nurse-led assessment confirms eligibility - you do not need to means-test or apply. Wales pays a higher rate of around £197.20/week and Northern Ireland uses a separate Registered Nursing Care Contribution.

- How does free personal care work in Scotland?

- Scotland funds Free Personal and Nursing Care for adults assessed as needing it. In a care home (2025/26 figures) the Scottish Government pays the care home £248.70 a week for personal care and a further £111.90 a week for nursing care, on top of any other contributions. You still pay for "hotel costs" - accommodation, food, heating - from your own income and capital, subject to the £35,000/£21,500 capital limits. So free personal care is genuinely free of charge, but it is not free care home fees. A self-funding Scottish resident in a £1,400/week home typically nets out paying around £1,000/week after the FPC and FNC offsets.

- Are care home fees different in Wales and Northern Ireland?

- Yes. Wales has the most generous capital limit in the UK - a single flat £50,000 - and operates a £100 maximum weekly contribution toward domiciliary (home) care. Above £50,000 of capital you pay full residential fees; below it the council means-tests your income only. Northern Ireland mirrors England with £23,250/£14,250 capital limits and similar tariff-income rules. Both nations pay separate nursing care contributions: Wales around £197.20/week, Northern Ireland a Registered Nursing Care Contribution at a similar level. Always verify with the relevant department - adult social care is fully devolved.

- Does Attendance Allowance count as income for the means test?

- For residential care in England, Attendance Allowance and the care component of Disability Living Allowance or Personal Independence Payment normally stop being paid after 28 days of local-authority-funded care. If you are a self-funder, AA continues - it is treated as income for the means test but it does not disqualify you from anything and it offsets the cost of care. Always claim AA the moment a person becomes care-needy: backdating is impossible and the higher rate (£114.60/week in 2026/27) over a year is nearly £6,000 of tax-free income. Pension Credit, Council Tax Reduction and the Severe Disability Addition continue alongside.

- What is the self-funder cross-subsidy and can I avoid it?

- Local authorities commission care home places at rates 15-30% below the market price homes charge private payers. Homes recover the difference by charging self-funders more for the same room and the same care - the "cross-subsidy", typically £200-£250 a week extra. The Competition and Markets Authority confirmed the practice in its 2017 market study and again in 2024 follow-up work; DHSC funding reforms intended to end it have been repeatedly postponed. You cannot insist on the council rate as a self-funder, but you can (a) negotiate hard on a private fee before signing - homes will discount for guaranteed long-stay residents, (b) ask explicitly for the council-commissioned rate sheet so you know the gap, and (c) trigger a council assessment as soon as your capital falls below £23,250 (England) so the home is forced to accept the contracted rate.