How equity release actually works

There are two product types in UK equity release, and one now dominates so completely that the other is a footnote.

- Lifetime mortgage - over 99% of new plans in 2025 (Equity Release Council). A loan secured against your home; you keep ownership. Interest is added each year and itself attracts interest (compounding). The loan and all rolled-up interest are repaid from the sale of the property when you die or move into long-term care; anything left over goes to your estate.

- Home reversion - under 1% of new plans. You sell a fixed percentage of your home (commonly 25-100%) to a reversion provider for tax-free cash, while continuing to live there rent-free under a lifetime lease. The cash you receive is typically 20-60% of the market value of the share you sell, because the provider is waiting decades to be paid.

Within lifetime mortgages there are three sub-shapes:

- Lump-sum - one upfront cash payment; interest accrues on the whole loan from day one. Average new lump-sum plan in Q4 2025: £127,414 (ERC).

- Drawdown - a smaller initial payment plus a reserve facility you draw from in tranches. Interest only accrues on what you have actually drawn - usually the cheapest shape over a long retirement.

- Income - the provider pays you a regular monthly sum (typically 10-25 years) instead of a lump. Niche but useful when a large bank balance would damage means-tested benefits.

Equity release is regulated by the FCA under MCOB 8 (advising and selling) and MCOB 9 (product disclosure). You must take regulated advice (no DIY) and use a solicitor. The cash you receive is tax-free because it is a loan or property sale, not income.

Is equity release right for you?

Equity release suits a specific set of circumstances and is clearly wrong in others. Use the decision tree as a starting point; a free MoneyHelper conversation and regulated adviser are then mandatory before signing.

- 1 I want to stay in my home but need a meaningful cash sum, and I have no other realistic way to raise it→ A lifetime mortgage is a reasonable candidate. Take regulated advice, get at least three quotes, and consider a drawdown plan rather than a lump sum to minimise the compounding bill.

- 2 I'd happily move to a smaller home if it freed up cash→ Downsize first. Selling and moving avoids decades of compounding interest, gives you the cash outright, and usually leaves more for the family. Equity release is most expensive when it could have been avoided by a move.

- 3 I want a regular income to top up my pension→ Consider an income lifetime mortgage, but also model a retirement interest-only (RIO) mortgage where you pay the monthly interest from income - the capital stays put rather than ballooning.

- 4 I'm under 65, in good health, and the loan would have to last 25+ years→ Be very cautious. The roll-up table below shows £100k borrowed at 6.63% becomes ~£497k after 25 years and ~£686k after 30. Younger borrowers pay the longest compounding bill. Look hard at alternatives.

- 5 I'm claiming or might claim Pension Credit, Council Tax Reduction or Universal Credit→ Pause. Cash from equity release counts as savings (over £6,000 reduces benefits, over £16,000 disqualifies most means-tested benefits). Check your benefits entitlement first - a Pension Credit claim is often worth more than the equity you would release.

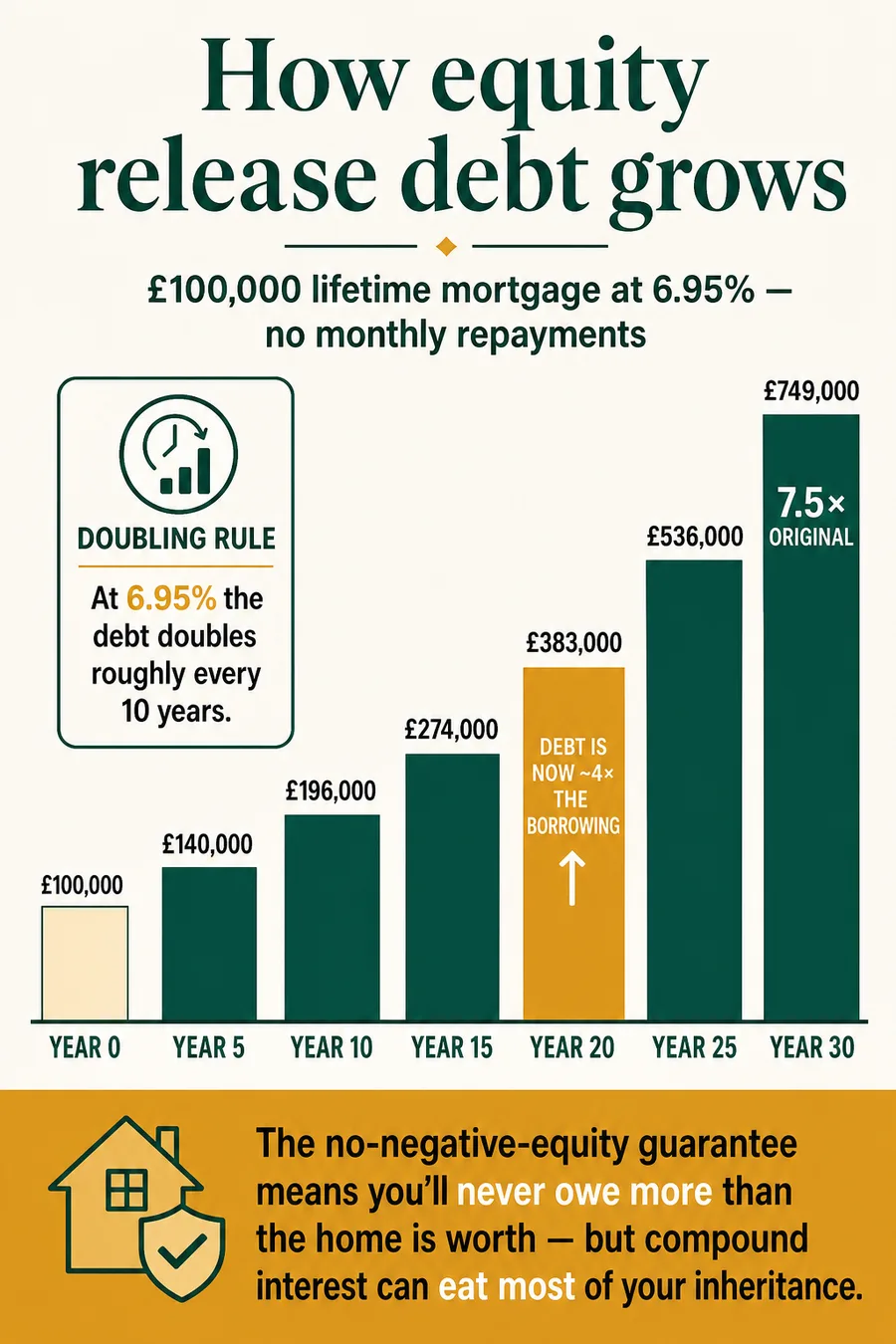

The real cost of roll-up interest - £100,000 borrowed at 6.63%

The table the marketing brochures bury. £100,000 borrowed at 6.63% (the cheapest May 2026 rate) with no repayments, against a £350,000 home held flat - a flat figure isolates the compounding effect rather than assuming house prices "cover it".

| Years | Debt owed (£100k @ 6.63%) | % of £350k home | Residual equity left |

|---|---|---|---|

| 5 | £137,847 | 39% | £212,153 |

| 10 | £190,018 | 54% | £159,982 |

| 15 | £261,934 | 75% | £88,066 |

| 20 | £361,067 | 103% | £0 |

| 25 | £497,720 | 142% | £0 |

| 30 | £686,092 | 196% | £0 |

Compound interest only, no repayments, flat £350,000 home value. Rates verified at 6.63% MER per moneyrelease.co.uk lowest-rate tracker, May 2026; this is below the Equity Release Council market average of ~7.24%. At the average rate of 7.24% the year-20 debt would be ~£405,000 and the year-30 debt ~£814,000. The no-negative-equity guarantee means you would never owe more than the home actually sells for - but it does not preserve your residual equity for the family.

Speak to an FCA-regulated equity release adviser

Compare lifetime mortgages and alternatives with a qualified later-life lending specialist. No fee unless you proceed.

Inline calculator: what will it cost over time?

Market average 7.24% (ERC); cheapest May 2026 6.63% MER.

| Years from now | Debt owed | Residual equity (flat home value) |

|---|---|---|

| 5 | £110,278 | £289,722 |

| 10 | £152,014 | £247,986 |

| 15 | £209,547 | £190,453 |

| 20 | £288,854 | £111,146 |

| 25 | £398,176 | £1,824 |

Compound interest only, no repayments, no growth in property value. Real-world plans may allow up to 10% voluntary annual repayment penalty-free (Equity Release Council standard), which materially reduces the long-run bill. Always confirm with a regulated equity release adviser using the MoneyHelper equity release guide and a Key Facts Illustration before signing.

The five Equity Release Council safeguards

Around 90%+ of new equity release advisers and lenders are members of the Equity Release Council, the trade body that sets product standards above the FCA baseline. Any plan from a member must meet five product safeguards. These are the bedrock of the consumer-protection case for equity release.

- No-negative-equity guarantee. When the property is sold for the best reasonably obtainable price, neither you nor your estate will ever owe more than the home sells for. Any shortfall is the lender's loss.

- Fixed (or capped) interest rate for life. The rate is set when you take out the plan and cannot rise (or, if variable, must have a lifetime cap). Almost all new plans are fixed.

- Right to remain in your home for life - or until you need to move into long-term care - provided it remains your main residence and you meet the terms of the contract.

- Right to port the loan to a new property. You can move home, subject to the new property being acceptable to your lender as continuing security.

- Right to make penalty-free voluntary repayments. Every ERC-compliant plan since March 2022 must allow voluntary partial repayments without Early Repayment Charges, within the lender's stated limits (commonly up to 10% of the loan each year).

A sixth protection added in May 2025 waives Early Repayment Charges entirely if you move permanently into long-term care, including informal care arrangements with relatives (a medical practitioner's certificate is required).

Three real-shape scenarios

Situation: Joan is increasingly frail. The family needs to plug a £30,000/year shortfall for care at home.

At 78 Joan's indicative max LTV is ~52% (~£230,000 on a £450,000 home). She takes a drawdown lifetime mortgage: £40,000 initially plus a £120,000 reserve drawn down as care needs grow.

- Year 1 debt: £40,000 (only drawn cash accrues interest)

- After 10 years drawing ~£25k/yr for six years: rolled-up debt ~£260,000; residual equity ~£190,000 (flat home value)

One of the cleaner cases for equity release: the alternative (selling Joan's home and moving into residential care she does not want) is worse on every dimension she values. The family should also check Attendance Allowance (non-means-tested, ~£5,740/yr higher rate in 2025/26) before drawing the maximum.

Situation: They want to give £100k to each of two adult children for house deposits. Tempted by equity release.

At the younger applicant's age (65) max LTV is ~36% - so a £200,000 release is achievable. At 6.63% MER fixed for life, no repayments:

- Year 10 debt: ~£380,000

- Year 20 debt: ~£722,000

- Year 25 debt: ~£995,000 - likely exceeding home value unless it appreciates ~3.4%/yr

The harder case. The gift would be a Potentially Exempt Transfer - they need to survive seven years for full IHT exemption. Better alternatives: gift smaller amounts each year from surplus income (the "normal expenditure out of income" exemption is immediately IHT-free), downsize, or take pension tax-free cash and gift from that. Equity release at 65 rarely wins.

Situation: Owns outright for 20 years. State Pension plus small DB pension. Wants a wet room, insulation and a new boiler.

Max LTV at 72 is ~44%; she only needs ~9%, so well within reach. She takes a drawdown lifetime mortgage: £15,000 initial plus £20,000 reserve. At 6.63% on the £15,000:

- Year 5 debt: ~£20,700

- Year 20 debt (assuming a further £10k drawn in year 5): ~£81,500

Residual equity stays above £300,000 at year 20 even on a flat house price. But Margaret should first check her local council's Disabled Facilities Grant (up to £30,000 in England for the wet room) and any ECO4 home energy grant eligibility. Free money beats borrowed money every time.

What equity release does NOT give you

- Your inheritance. The NNEG stops you owing more than your home is worth, but does not preserve what you leave behind. Most of the equity can be eaten up by interest over a long retirement - see the cost table above.

- Means-tested benefits. Released cash in a bank account counts as savings. Pension Credit, Council Tax Reduction, Housing Benefit and Universal Credit are reduced above £6,000 and most are cut off above £16,000. The £127,414 average lump sum will eliminate most means-tested entitlements unless spent quickly on a non-savings purpose.

- Early Repayment Charges if you change your mind. Within the early years (typically 5-15) you can face ERCs of 10%+ outside the penalty-free repayment limit. Fixed ERCs taper; gilt-linked ERCs are capped at 25%. ERCs are waived on death, second death (joint plan) and permanent move into long-term care under Council standards from May 2025.

- Set-up costs. Expect £1,500-£3,000+ on top of the loan: arrangement fee, valuation, legal fees and adviser fees. Compare on headline rate plus all-in costs, not freebies.

- The ability to take it back. Once the cash is released and spent, it is spent. Selling and downsizing flexibility is gone. Hard to unwind without an ERC and harder still if you have gifted to family.

Alternatives to consider first - your adviser is required to

- Downsize. Selling and moving realises cash without borrowing or compounding interest. SDLT, agent fees and moving costs typically total 3-8% of the new property price - small compared to 20+ years of compounding.

- Retirement interest-only (RIO) mortgage. You pay monthly interest from income; the capital stays fixed until you die or move. Preserves much more equity if you can afford the payments.

- Standard older-borrower mortgage on regular repayment terms, if you have provable retirement income.

- Pension tax-free cash. 25% of a DC pension is tax-free from age 55 (57 from April 2028). May cost nothing in interest at all.

- Family loan or formal IOU at zero or low interest, documented by a solicitor. Beware family dynamics.

- Unclaimed benefits. An estimated £2.2bn of Pension Credit goes unclaimed each year. A successful claim opens the door to Council Tax Reduction, Housing Benefit, free TV licence (75+) and the Winter Fuel Payment. For many pensioners this is worth more annually than equity release would release.

A regulated equity release adviser is required by the FCA to consider and document why alternatives are not appropriate before recommending a plan. If you cannot remember being shown alternatives, your advice may not have been compliant.

The April 2027 inheritance tax angle

From 6 April 2027, most unused defined contribution pensions and pension death benefits will be included in your estate for inheritance tax (HM Treasury, July 2025 consultation response). The OBR estimates an extra 10,500 estates will fall into IHT in 2027/28 alone.

Equity release reduces the value of your estate because the debt is repaid before anything passes to beneficiaries - so it can offset some of the new pension-IHT exposure. But the maths rarely stacks up unless the IHT savings outweigh the compounding cost. A £200,000 release at age 70 at 6.63% becomes ~£723,000 of debt after 20 years; you would need to be saving more than £500,000 in IHT for the trade to be net positive.

For most people the simpler moves are: spend pension first (it'll be in the estate from 2027 anyway), gift from surplus income (the "normal expenditure out of income" exemption is immediately IHT-free), use the £3,000 annual gift allowance, and consider downsizing. See our full guide to inheritance tax on pensions from April 2027.

Today's equity release rates - May 2026

Always get at least three quotes from a whole-of-market adviser. The cheapest plan depends on age, LTV, property and plan shape.

| Benchmark | May 2026 | Source |

|---|---|---|

| Lowest advertised rate | 6.63% MER | moneyrelease.co.uk live tracker |

| Market average advertised rate | ~7.24% | ERC Summer 2025 Market Report |

| Typical fixed-period ERC, year 1 | 8-10% | Fixed-ERC structure, tapering to zero |

| Voluntary repayment allowance | Up to 10%/yr | ERC standard 5 - penalty-free |

| Average new lump-sum plan size, Q4 2025 | £127,414 | Equity Release Council Q4 2025 |

| Q1 2026 total lending | £574m | ERC Q1 2026 lending bulletin (-9% QoQ) |

The Equity Release Council's Q1 2026 lending figures (published May 2026) frame the same picture: lending of £574m was a 9% quarterly drop, new plans fell to 4,868, lifetime mortgages still accounted for more than 99% of activity, and returning drawdown customers declined only 2%. The Council noted that 45% of firms reported a rise in enquiries and 38% an increase in applications - demand remains intact beneath the headline numbers.

Frequently asked questions

- What is equity release and how does it work?

- Equity release lets UK homeowners aged 55+ access some of the value tied up in their home as tax-free cash without moving. The dominant product (over 99% of new plans in 2025) is the lifetime mortgage - a loan secured against your home that is usually only repaid when you die or move into long-term care. Interest rolls up and compounds unless you make voluntary repayments; the loan plus all interest is repaid from the eventual sale of the property, with anything left over going to your estate. The other product, home reversion, involves selling part of your home to a provider at below market value in exchange for tax-free cash, while continuing to live there rent-free for life.

- What is the current equity release interest rate in 2026?

- In May 2026 the lowest advertised equity release rate is around 6.63% MER, according to industry tracker moneyrelease.co.uk. The Equity Release Council's most recent Market Report put the average advertised rate at 7.24%. Your own rate depends on age, LTV, property type and provider. Rates are quoted as either MER (monthly compounding) or AER (annual compounding) - always compare like with like. Almost all new plans are fixed for life under Equity Release Council standards.

- How much can I borrow with equity release?

- The maximum loan-to-value (LTV) is driven mainly by age. As an industry guide: ~20-25% at 55, ~30% at 60, ~36% at 65, ~42% at 70 and over 50% at 80. The older you are, the more you can release because the lender expects to recover the loan sooner. The average new lump-sum plan in Q4 2025 was £127,414 (Equity Release Council). Joint plans use the age of the younger applicant.

- Is equity release safe?

- Equity release is regulated by the FCA under MCOB 8 (advising) and MCOB 9 (product disclosure). Plans from Equity Release Council members carry five product safeguards including a no-negative-equity guarantee, fixed/capped rates for life and the right to remain in your home for life. You must take regulated advice and use a solicitor. The risks regulation does not eliminate are economic: interest compounds for decades so long-run cost is high; the loan can wipe out most of the inheritance; and it can affect means-tested benefits like Pension Credit if you keep the cash in the bank.

- What is the no-negative-equity guarantee?

- The no-negative-equity guarantee (NNEG) is the headline consumer protection on any plan from an Equity Release Council member. It promises that, provided the property is sold for the best price reasonably obtainable and the terms of the loan have been met, neither you nor your estate will ever owe more than the property sells for. Any shortfall is the lender's loss. The NNEG caps your loss at the home value but does not preserve any inheritance for beneficiaries.

- What are the alternatives to equity release?

- Before recommending equity release, a regulated adviser is required to consider alternatives: downsizing, a retirement interest-only (RIO) mortgage where you pay interest monthly from income, a standard older-borrower mortgage if you have provable income, family loans, using cash savings or taking pension tax-free cash first, and claiming any unclaimed benefits like Pension Credit, Attendance Allowance or Council Tax Reduction. For many households a Pension Credit claim is worth more annually than equity release would ever release.

- Will equity release affect my inheritance?

- Usually significantly. Because interest compounds, a small loan grows into a much larger debt over typical retirement timeframes. £100,000 borrowed at 6.63% with no repayments grows to ~£190,000 after 10 years, ~£361,000 after 20 years and ~£686,000 after 30. That debt is repaid from your estate before anything passes to beneficiaries. Voluntary partial repayments (up to 10%/yr penalty-free), drawdown plans and downsizing-protection clauses all help reduce the impact.

- Can I repay equity release early?

- Yes, but most plans charge an Early Repayment Charge (ERC) in the first 5-15 years outside agreed limits. Fixed ERCs taper down (e.g. 10% in year 1, 9% in year 2, zero by year 10). Gilt-linked ERCs vary with gilt yields and are typically capped at 25% of the loan. Under Equity Release Council Standards 2.0 (May 2025), ERCs are waived if you move permanently into long-term care or on second death of a joint plan. All ERC-compliant plans allow penalty-free voluntary partial repayments, typically up to 10% of the loan a year.

- Will equity release affect my State Pension or benefits?

- It does not affect the State Pension (not means-tested). But it can affect Pension Credit, Council Tax Reduction, Housing Benefit and Universal Credit. Released cash counts as savings once in your bank - the first £6,000 is ignored, between £6,000 and £16,000 reduces benefits by £1/week per £500, and savings over £16,000 disqualify you from Pension Credit. The fix is to spend the cash promptly on a non-savings purpose (paying off a mortgage, home improvements) or take a drawdown plan that releases small tranches as needed.

- Should I use a drawdown lifetime mortgage instead of a lump sum?

- A drawdown plan gives you an initial cash sum plus a reserve facility you can draw from in tranches later. The huge advantage: interest only accrues on the money you have actually taken - the headroom sits free of interest until used. For most retirees wanting a buffer for future home repairs, care needs or family help, drawdown costs much less over time than a lump sum. The trade-off is that future drawdowns may be at the prevailing rate at the time, not the rate on your original plan.

Speak to an FCA-regulated equity release adviser

Compare lifetime mortgages and alternatives with a qualified later-life lending specialist. No fee unless you proceed.

- Free, no-pressure first chat, typically by phone or video

- Whole-of-market comparison across FCA-regulated lenders

- You stay in control and decide if you take it any further

RetirementExpert is an information service, not an adviser. By submitting this form you consent to being contacted by an FCA-regulated equity release specialist.