Should you drawdown or buy an annuity?

The first £25,000 of a £100,000 pot is tax-free either way. The question is what to do with the other £75,000. The four branches below cover the situations where the answer is reasonably clear. Pension Wise - the free, government-backed guidance service delivered by MoneyHelper - is the right first stop before doing anything irreversible.

- 1 I want a guaranteed lifetime income, no surprises→ An annuity may suit - even partial annuitisation. You give up flexibility and inheritance for certainty. Shop around: rates between providers vary by 10-20%.

- 2 I want flexibility and to leave money to my family→ Drawdown - but watch out for sequence-of-returns risk. Under current rules, a defined-contribution pot passes to beneficiaries tax-free if you die before 75, taxed as their income if after.

- 3 I'm worried about running out of money but want some flexibility→ Consider a hybrid: annuitise enough to cover essentials when added to the State Pension, drawdown the rest. PLSA's £13,400 'Minimum' line is a useful target for the guaranteed leg.

- 4 I have health conditions (smoker, diabetes, heart, BMI)→ Get enhanced annuity quotes - rates can be 13-20%+ higher than standard. Nearly half of all annuity sales in 2024/25 were enhanced (FCA data).

The 25% tax-free cash

Whatever you do with the rest of the pot, you can take up to 25% of a £100,000 pension as a tax-free lump sum - the pension commencement lump sum (PCLS), defined in HMRC's Pensions Tax Manual at PTM063210. The cap across all your pensions combined is the Lump Sum Allowance, currently £268,275; the £25,000 from a £100k pot is comfortably inside it. You can take this from age 55 today, rising to 57 from 6 April 2028.

The £75,000 funds either drawdown (you keep it invested and withdraw an income) or buys an annuity (you swap it for a guaranteed income for life). The £25,000 is yours: clear a mortgage, top up an ISA, pay for a long-awaited trip, or - most boringly but often best - leave it in a savings account as your emergency buffer.

Year-by-year drawdown projection - the 4% rule on £100k

Starting pot £100,000. Withdraw £4,000 in year 1 (the 4% rule); withdrawals rise with inflation at 2.5% a year. Remaining balance after each withdrawal grows at 5% a year. Withdrawals are taken at the start of each year, growth applies to what's left. These are illustrative assumptions - real returns are bumpier and the order matters (see "sequence-of-returns risk" below).

| Year | Starting pot | Withdrawal | Growth on remainder | Closing pot |

|---|---|---|---|---|

| 1 | £100,000 | £4,000 | £4,800 | £100,800 |

| 5 | £102,786 | £4,415 | £4,919 | £103,289 |

| 10 | £104,319 | £4,995 | £4,966 | £104,289 |

| 15 | £102,744 | £5,652 | £4,855 | £101,947 |

| 20 | £96,741 | £6,395 | £4,517 | £94,863 |

| 25 | £84,559 | £7,235 | £3,866 | £81,190 |

| 30 | £63,899 | £8,186 | £2,786 | £58,499 |

Under these central assumptions the pot is still worth roughly £58,499 at the end of year 30 - almost back to its starting value in nominal terms, but heavily eroded in real (inflation-adjusted) terms. With these settings the pot would not deplete inside 30 years; it would run out at around year 38 if conditions held.

Why sequence-of-returns risk matters more than average returns

The single biggest hazard for a drawdown retiree is the order in which good and bad investment years arrive - not the long-run average return. Two retirees with the same starting pot, the same withdrawal rate and the same average return over 30 years can end up with very different outcomes if one retires into a market crash and the other does not. A 30% market fall in your first two retirement years means every withdrawal you take is locking in losses, and the smaller pot then has less to compound back on the way up.

Three practical defences for a £100k pot in drawdown:

- Keep 1-2 years of withdrawals in cash. If markets fall, draw from the cash buffer for 12-24 months instead of selling fund units at depressed prices. Top up the cash buffer in good years.

- Use guardrails, not a fixed percentage. Start at 4% but cut withdrawals by 10% after a year where the pot falls by more than 15%. Restore the original level when the pot recovers. This simple rule materially extends pot longevity in the bad-case scenarios that worry retirees most.

- Annuitise enough to cover essentials. If your State Pension plus a small annuity covers food, energy and council tax, your drawdown pot only has to fund discretionary spending. That changes the psychology of a market fall - you don't have to sell.

Today's annuity rates - £100,000 pot

The figures below are from Hargreaves Lansdown's "Best annuity rates" table, generated using HL's online quote tool comparing the UK's leading annuity providers. The quote date is 7 May 2026. Quotes assume an average postcode and payment monthly in advance. Joint-life quotes assume a spouse three years younger.

| Annuity type | Age 65 | Age 67 (interp.) | Age 70 |

|---|---|---|---|

| Single life, level, no guarantee | £7,891 | £8,181 | £8,616 |

| Single life, level, 5-year guarantee | £7,830 | £8,100 | £8,506 |

| Joint life 50%, level, no guarantee | £7,322 | £7,608 | £8,038 |

| Single life, RPI-linked, 5-year guarantee | £5,437 | £5,782 | £6,300 |

| Joint life 50%, 3% escalation, no guarantee | £5,332 | £5,654 | £6,136 |

| Enhanced (smoker, single life level) | £9,100 | £9,430 | £9,930 |

Indicative rates from Hargreaves Lansdown - Best annuity rates, quote date 7 May 2026. Age-67 figures are linearly interpolated from HL's published age-65 and age-70 quotes - treat them as indicative. The "Enhanced" row is a typical smoker rate (~15% higher than standard, single-life level); your own quote will depend on the specific conditions disclosed. The "Joint life 50% with 3% escalation" line is HL's published proxy for an inflation-style joint-life product - RPI-linked joint-life is offered by fewer providers and pricing is similar.

Get matched with a regulated pension adviser

Pension drawdown is a high-stakes, irreversible decision. Speak to an FCA-regulated specialist before you commit.

Inline calculator: what income could you get?

Default 67 - the State Pension age from April 2028.

4% is the classic "Bengen" rule; Morningstar UK's 2025 figure is 3.9%.

Your estimated total annual income before tax is £15,548. That's £3,000 from the pot plus the full new State Pension of ££12,547.6 for 2026/27.

Compare with the PLSA Retirement Living Standards: Minimum single £13,400, Moderate £31,700, Comfortable £43,900 (2025/26 figures). Income tax of around £596 applies at basic rate on the income above your £12,570 personal allowance.

Approximate. Annuity figures based on HL best-buy rates 7 May 2026, interpolated between ages 65 and 70 (single-life level, no guarantee). Drawdown is a steady percentage withdrawal, not a guarantee. Always confirm with MoneyHelper's annuity comparison tool before buying.

Three real scenarios

Situation: Just hit State Pension age. Wants to clear the last £15k of her mortgage and have a small income on top of the State Pension.

Jean takes the £25,000 tax-free cash. £15,000 clears her remaining mortgage payments; £10,000 goes into a Cash ISA as an emergency buffer. The £75,000 stays in drawdown invested in a balanced multi-asset fund. She withdraws 4% in year one - £3,000 - rising with inflation.

- State Pension: £12,547.60/yr (2026/27)

- Drawdown: £3,000/yr starting

- Total: £15,547.60/yr before tax

- Income tax: personal allowance £12,570 → £2,977.60 taxable at 20% = roughly £596/yr

- Net: ~£14,952/yr (~£1,246/month)

This lands her about £1,500 above the PLSA "Minimum" single line (£13,400) and £16,000 below "Moderate" (£31,700). Mortgage-free with a buffer ISA is the unsung win: by removing a fixed cost, Jean has effectively raised her standard of living more than another £1,500 a year of drawdown would have done.

Situation: Cautious. Geoff has a heart condition. They want certainty, not flexibility.

They take the £25,000 tax-free (split as a household). With the remaining £75,000 they buy a joint-life 50% RPI-linked annuity. On HL's May 2026 best-buy table the comparable joint-life 50% with 3% escalation pays £5,332/yr at age 65 per £100k, so on £75,000 that's roughly £4,000/yr guaranteed for life, indexed.

- State Pensions: 2 × £12,547.60 = £25,095/yr

- Annuity: £4,000/yr starting, rising with inflation

- Total: ~£29,095/yr before tax, fully inflation-protected

Geoff applies for an enhanced joint-life annuity because of his heart condition. The same £75k could buy 13-20% more income - meaning £4,500-£4,800/yr instead of £4,000. The enhanced uplift on joint-life rates is usually smaller than on single-life (because both lives are priced), but always worth quoting. If Geoff dies first, Anne keeps 50% of the annuity income for life. They're a few hundred pounds short of the PLSA "Minimum" two-person figure of £21,600, but well within range - and they've eliminated the longevity worry.

Situation: Just been made redundant. £100k pot, seven years to State Pension age. Tempted to take the £25k tax-free now.

Taking the £25,000 tax-free at 60 feels safe - it's tax-free either way, right? But the remaining £75,000 then can't grow inside the pension wrapper for another seven years before Ravi reaches State Pension age. The maths:

- If Ravi leaves the full £100,000 invested for 7 years at 5% real growth, the pot grows to ~£140,710. He could then take 25% (£35,178) tax-free at 67.

- If he takes £25,000 now and the remaining £75,000 grows for 7 years at 5%, that £75k becomes ~£105,533. There's no more tax-free cash to take - he already used his 25%.

- Net difference: ~£10,000 less tax-free cash later, plus the £25k he took early is now sitting in a savings account earning maybe 4% (and being taxed on the interest) instead of compounding tax-free.

There are reasons to take the cash early - clearing high-interest debt, a genuine emergency, or a one-off purchase that genuinely improves the next decade. But "I might need it" usually means it ends up in a Cash ISA earning less than the pension would have. The emergency tax hit on Ravi's first taxable drawdown can also be ugly: he might have to reclaim £2,000+ via HMRC's P55 form. Before touching the pension, book a free Pension Wise session and check redundancy pay structure (the first £30,000 is income-tax-free).

Where £100k + State Pension lands you (PLSA standards)

The Pensions and Lifetime Savings Association (PLSA) publishes the Retirement Living Standards each year - the income needed to fund three different lifestyles in retirement, researched with Loughborough University. The 2025/26 figures assume housing costs are already covered.

| Lifestyle | One-person household | Two-person household |

|---|---|---|

| Minimum | £13,400 | £21,600 |

| Moderate | £31,700 | £43,900 |

| Comfortable | £43,900 | £60,600 |

A £100k pot funding £4,000 of drawdown plus the full new State Pension (£12,548) gives a single retiree ~£16,548/yr - comfortably clearing "Minimum" but ~£15,000 short of "Moderate". A level annuity bumps this to ~£20,440, still well short of Moderate single (£31,700). To reach Moderate single, you'd need roughly a £475,000 pot drawing at 4% on top of the State Pension. See our £500k pot guide for that maths.

How drawdown is taxed

The 25% tax-free cash is tax-free - it does not use your personal allowance. Everything else you withdraw from the pension is taxable as income in the year you take it, on top of any other income including the State Pension. The State Pension is paid gross but is taxable; HMRC usually collects the tax on it by adjusting your PAYE tax code on your private pension.

- State Pension: £12,547.60

- Drawdown income (4% of £75k): £3,000

- Total taxable income: £15,547.60

- Less personal allowance (£12,570): taxable at 20% on £2,977.60

- Income tax: ~£596/yr (~£50/month) - collected via PAYE on the private-pension stream

Take £4,000 of drawdown instead and you're at £16,547.60 total, with ~£796/yr in tax. Take larger lump sums (UFPLS or full encashment) and the tax bill jumps quickly because the withdrawal stacks on your other income. Full guide: how drawdown is taxed.

Shopping around for annuities - the FCA data

If you're going down the annuity route, treat it like buying a car: the difference between the best and worst quotes is real money, and most providers will not give you their best rate unless you compare. The FCA's Retirement Income Market Data 2024/25 shows that 62% of annuities are now bought away from the consumer's existing pension provider - the highest share since the data series began, and that enhanced annuities now account for 48% of guaranteed-income-for-life sales (up from 38% six years ago).

The fastest free way to get quotes from every annuity provider on the market is MoneyHelper's annuity comparison tool. Pair it with a Pension Wise session - also free, government-backed, by phone or video - before signing anything. Annuities are an irreversible decision; once bought you cannot unwind them.

What people actually do with the £25,000 tax-free cash

The £25,000 PCLS is the most-misused number in UK retirement planning. The default move - take it because you can - is often the wrong one. Five better-than-average uses, roughly in order of how often they make sense:

- Clear high-interest debt. Credit cards or unsecured loans at 20%+ APR outweigh almost any pension return. Clearing a £15k credit card balance is a guaranteed 20% "return" on that £15k for as long as you'd have carried it. Mortgage debt at 4-5% is a much closer call - see (3).

- Build an emergency buffer in a Cash ISA. 3-6 months of essential spending in a separate account, untouched. Inside an ISA the interest is also tax-free. This single move is what stops people having to sell drawdown fund units at the worst moment.

- Clear the last of a mortgage. Removing a fixed monthly cost is a quiet but powerful raise in living standard. The maths is closer than people think - if your mortgage rate is below your expected pension growth, leaving the money invested may win - but the peace-of-mind argument for a fully owned home in retirement is real.

- Top up an ISA in slices. The £25,000 can move from pension to ISA across two tax years (£20,000 ISA limit per year). Inside the ISA it grows tax-free, comes out tax-free, and unlike the pension it does not count toward your taxable income - useful for managing the personal allowance.

- Bridge to State Pension age. If you're retiring at 60-63 and your State Pension doesn't start for four to seven years, the £25k can fund part of the gap, letting you delay both drawdown and State Pension (which earns a ~5.8%-per-year deferral uplift).

The bottom-of-the-list use is "moving £25,000 from a tax-advantaged wrapper into a current account because that feels safer". A balanced fund inside the pension grows tax-free and (under current rules) passes IHT-free to beneficiaries if you die before 75. Cash in a current account does neither.

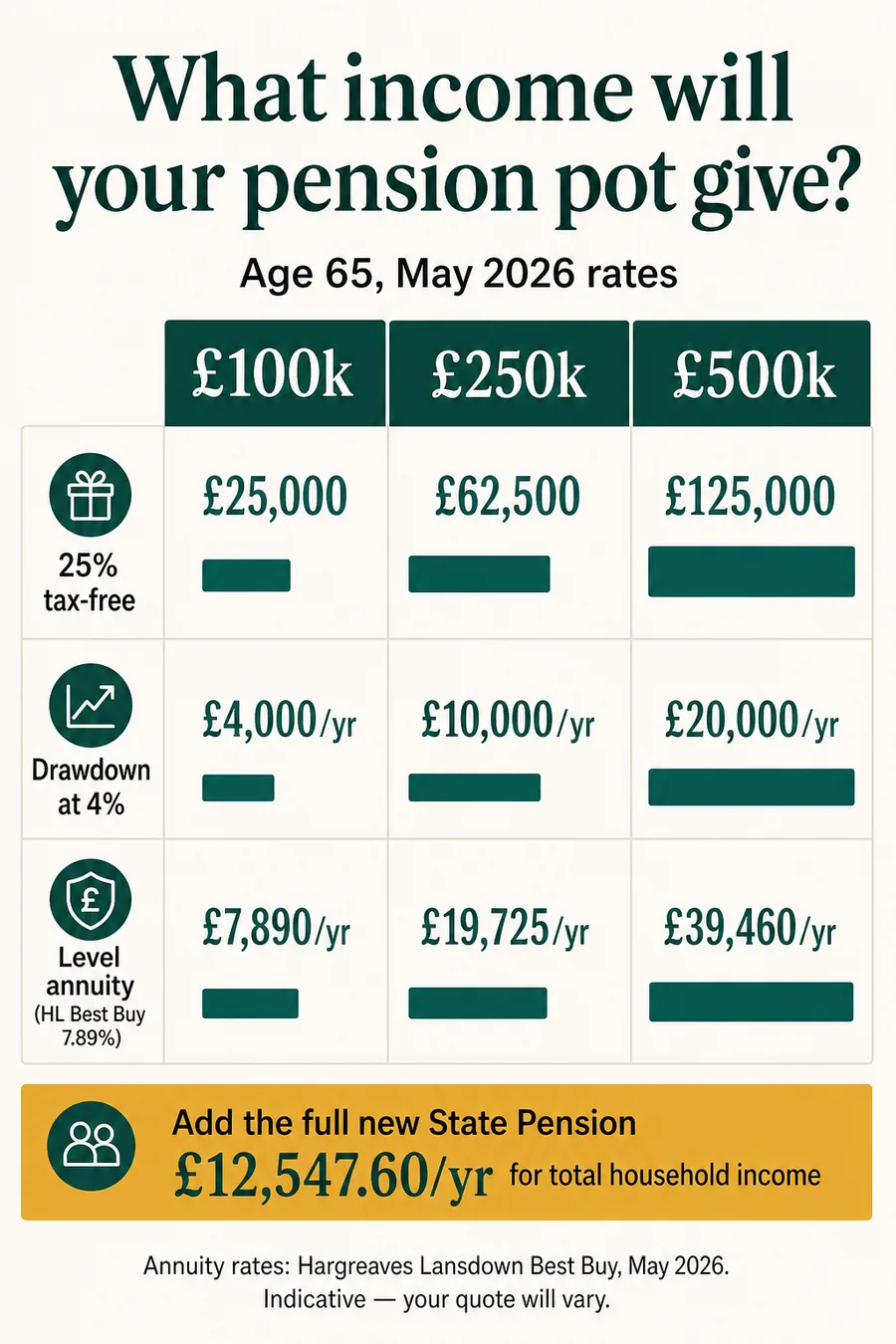

Compare with £150k and £250k pots

A bigger pot moves you up the PLSA ladder. The same 4% rule and the same annuity rates applied to larger pots produce:

Frequently asked questions

- How much income will a £100k pension pot give me?

- On its own, around £4,000 a year in flexible drawdown using the 4% rule, or about £7,891 a year (May 2026 best-buy rate from Hargreaves Lansdown) from a level single-life annuity at 65. Add the full new State Pension of £12,547.60 in 2026/27 and you get roughly £16,500 a year from drawdown or £20,400 a year from a level annuity, before tax. Inflation-linked annuity options pay less to start (around £5,400 a year) but rise each year with prices.

- Is £100k enough to retire on UK?

- On its own, no. Combined with the full new State Pension, a £100,000 pot covers the PLSA "Minimum" Retirement Living Standard for a single retiree (£13,400 a year in 2025/26 figures), but falls well short of "Moderate" (£31,700) and miles below "Comfortable" (£43,900). For a couple sharing one £100k pot plus two State Pensions, you would clear "Minimum" (£21,600 for a two-person household) but still be £15,000+ a year short of "Moderate". A £100k pot is best thought of as a useful top-up, not a complete retirement plan.

- How long will a £100k pension last me?

- On the classic 4% rule - £4,000 a year rising with inflation, with the rest invested in a balanced fund returning ~5% a year - a £100k pot lasts around 30 years in the central case. Morningstar's 2025 research found that 3.9% is the highest "safe" inflation-adjusted starting rate for a 30-year horizon at 90% confidence. Take 5% a year and the pot is more likely to run out in 23-25 years; take 6% and it may not see 20 years. Real-world outcomes depend heavily on the order of investment returns in the early years (sequence-of-returns risk).

- What annuity will I get for £100k?

- On Hargreaves Lansdown's best-buy rates dated 7 May 2026, a £100,000 pension buys a healthy 65-year-old a single-life level annuity paying £7,891 a year for life, or £8,616 a year at 70. An inflation-linked (RPI) version pays £5,437 a year at 65 to start, rising each year. Joint-life 50% (spouse three years younger) pays £7,322 a year at 65 on a level basis or £5,332 a year on an escalating basis. Enhanced annuity rates for smokers or those with qualifying medical conditions can be 13-20%+ higher.

- Should I take my pension as cash at 55?

- You can - from age 55 (rising to 57 from 6 April 2028 under HMRC rules) - but only the first 25% (up to £25,000 from a £100k pot) is tax-free, capped at £268,275 across all your pensions. The remaining £75,000 is taxed as income. Taking it all in one tax year would push you well into higher-rate tax. Most people are better off taking only the 25% tax-free cash, leaving the rest invested in drawdown, or laddering withdrawals over several tax years. Also note: HMRC almost always applies an emergency tax code to first taxable withdrawals, so you may need to reclaim a refund via P55 or P53Z.

- Can I have a £100k pension and the State Pension?

- Yes. Your private pension and your State Pension are entirely separate. The State Pension is based on your National Insurance record (you need around 35 qualifying years for the full new rate of £241.30 a week in 2026/27). It is paid in addition to any workplace or personal pension, with no means-test on your savings. The only complication is tax: both are taxed as income, so once your combined income passes the £12,570 personal allowance, the excess is taxed at 20% (basic rate).

- What's the 25% tax-free amount on a £100k pension?

- On a £100,000 defined contribution pension, you can take 25% (£25,000) as a tax-free lump sum from age 55 (57 from April 2028). This is officially the "pension commencement lump sum" (PCLS), and it sits within the £268,275 Lump Sum Allowance that applies across all your pensions combined. You can take it in one go or in slices alongside taxable income (a phased "uncrystallised funds pension lump sum" or UFPLS). The £75,000 left behind then either stays in drawdown or buys an annuity.

- How is income from a £100k pension taxed?

- The 25% tax-free cash (£25,000) is paid free of UK income tax and does not use your personal allowance. The remaining £75,000 is taxed as income whenever you draw from it. On a typical drawdown setup paying £4,000 a year, plus the £12,547.60 State Pension, your taxable income is £16,547.60. The first £12,570 is covered by the personal allowance and you pay 20% on the remaining £3,978 - about £796 a year in income tax. Living in Scotland changes the rates slightly. Pension income is paid through PAYE.

- Is a £100k pot taxed if I die?

- Under current rules, if you die before age 75 your remaining defined-contribution pension passes to your nominated beneficiary tax-free, whether they take it as a lump sum or as income. If you die at or after age 75, the beneficiary pays income tax at their marginal rate on whatever they withdraw. This is one of the biggest reasons drawdown is often more tax-efficient on death than an annuity, which usually ends with you unless you bought a joint-life or guaranteed-period version. From April 2027 the government plans to bring most unused pensions inside inheritance tax - check the latest HMRC guidance before planning around death benefits.

- Should I drawdown or buy an annuity with £100k?

- Neither is universally right. Drawdown gives flexibility, growth potential and money left to family - but income is not guaranteed and the pot can run out. Annuity gives a guaranteed income for life - but no flexibility, and (unless you bought joint-life or a guarantee period) nothing left to beneficiaries. A common middle path is to annuitise enough to cover essentials when added to the State Pension, then keep the rest in drawdown. Pension Wise (free, government-backed) is the right first call. If you have any qualifying medical conditions, get enhanced annuity quotes - rates can be 13-20%+ higher.

Get matched with a regulated pension adviser

Pension drawdown is a high-stakes, irreversible decision. Speak to an FCA-regulated specialist before you commit.

- FCA-regulated advisers, vetted for retirement specialism

- First call is free — no obligation to proceed

- Drawdown, annuity and hybrid strategies compared

RetirementExpert is not a financial adviser. Introductions are made to firms authorised and regulated by the Financial Conduct Authority.