The short answer

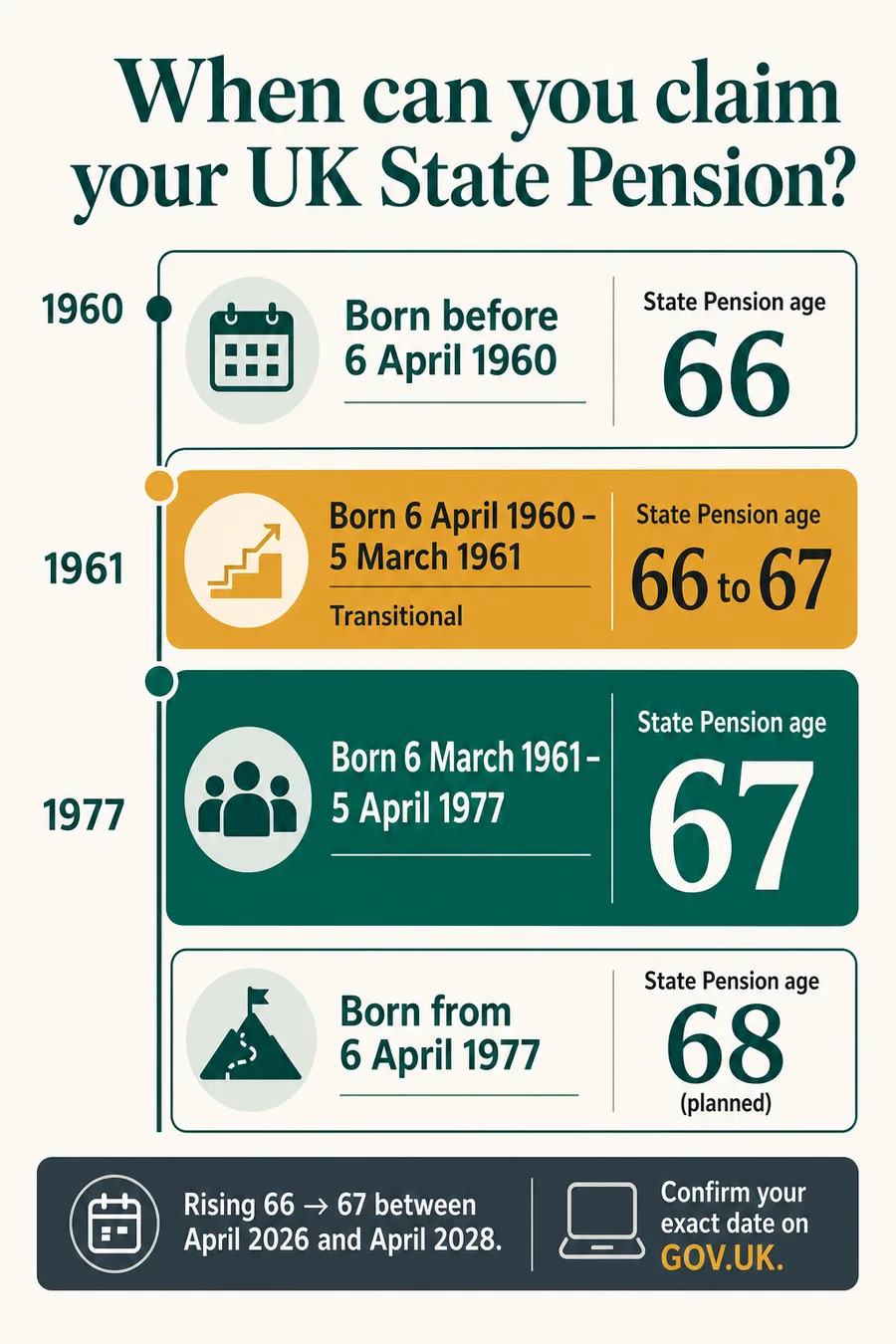

Your State Pension age in the UK depends only on your date of birth. As of today (16 May 2026) there are four scenarios. If you were born before 6 April 1960, your State Pension age was 66 and you have already reached it. If you were born between 6 April 1960 and 5 March 1961, you are in the transitional cohort - your State Pension age is somewhere between 66 years 1 month and 66 years 11 months, and you will reach it between 6 May 2026 and 5 February 2028. If you were born between 6 March 1961 and 5 April 1977, your State Pension age is 67. If you were born from 6 April 1977 onwards, the planned State Pension age is 68, currently legislated to apply between 2044 and 2046 - but a future review could move that date.

Find your age in 5 seconds

Use the decision tree below. Each branch ends in your State Pension age under the legislation in force today.

- 1 Born before 6 April 1960→ State Pension age 66. You have already reached it. If you have not yet claimed, you can claim now and backdate up to 12 months, or carry on deferring at ~5.8% a year.

- 2 Born between 6 April 1960 and 5 March 1961→ You are in the transitional band. Your State Pension age is between 66 years 1 month and 66 years 11 months. Use the table below to find your exact month, or the inline calculator.

- 3 Born between 6 March 1961 and 5 April 1977→ State Pension age 67. You will reach it on your 67th birthday.

- 4 Born between 6 April 1977 and 5 April 1978→ You are in the second transitional band under the Pensions Act 2007. Your State Pension age is between 67 and 68, with the exact date set by the GOV.UK timetable - for example, born 6 April 1977 → 6 May 2044; born 6 March 1978 → 6 March 2046.

- 5 Born on or after 6 April 1978→ Planned State Pension age 68. The 2023 government review kept the existing 2044-2046 timetable for the rise to 68, but a further review is due in the current Parliament. If you are in your 40s today, plan for a State Pension age of at least 68.

Inline calculator

Enter your date of birth for an exact answer. For a fuller version with sharing and printing, use the full State Pension age calculator.

Full 66 to 67 transition table

This is the table most competitors leave out. It is the birth-date-band detail for the transitional cohort, reproduced from the GOV.UK State Pension age timetable (originally legislated in the Pensions Act 2014). The bands follow tax-year boundaries (6th of one month to 5th of the next). If your birthday lands on the boundary day, read carefully - a single day can move you by a whole month.

| Date of birth | State Pension age | First payment from (approx.) |

|---|---|---|

| 6 April 1960 - 5 May 1960 | 66 years and 1 month | 6 April 2026 onward |

| 6 May 1960 - 5 June 1960 | 66 years and 2 months | 6 May 2026 onward |

| 6 June 1960 - 5 July 1960 | 66 years and 3 months | 6 June 2026 onward |

| 6 July 1960 - 5 August 1960 | 66 years and 4 months | 6 July 2026 onward |

| 6 August 1960 - 5 September 1960 | 66 years and 5 months | 6 August 2026 onward |

| 6 September 1960 - 5 October 1960 | 66 years and 6 months | 6 September 2026 onward |

| 6 October 1960 - 5 November 1960 | 66 years and 7 months | 6 October 2026 onward |

| 6 November 1960 - 5 December 1960 | 66 years and 8 months | 6 November 2026 onward |

| 6 December 1960 - 5 January 1961 | 66 years and 9 months | 6 December 2026 onward |

| 6 January 1961 - 5 February 1961 | 66 years and 10 months | 6 January 2027 onward |

| 6 February 1961 - 5 March 1961 | 66 years and 11 months | 6 February 2027 onward |

| 6 March 1961 - 5 April 1977 | 67 | Your 67th birthday |

For example, someone born on 5 December 1960 falls into the band 6 November 1960 - 5 December 1960 and reaches State Pension age at 66 years and 8 months - that is, 5 August 2027.

Three real scenarios

Situation: Turned 65 last December, hoping to stop work but caught in the 66 → 67 transitional band.

Under the 66 → 67 timetable Marcus’s State Pension age is 66 years and 8 months - he can first claim on 5 August 2027.

Three jobs he should do this month:

Request a State Pension forecast on GOV.UK and check whether any missing National Insurance years are worth buying - voluntary Class 3 contributions cost around £907 for a full year in 2026/27 and can add ~£329 a year to his pension for life.

Check whether his workplace pension can bridge the 20-month gap between 65 and 66 years 8 months - drawdown or a fixed-term annuity are the usual options.

Wait for the DWP letter (it arrives about four months before SPA) to confirm the exact day, because Marcus’s birthday is right on the boundary.

Situation: One partner already drawing State Pension, the other three years short.

Janet is 67 and already drawing the full new State Pension (£241.30 per week from April 2026). David is 64 and won’t reach State Pension age until his 67th birthday in 2029.

They cannot start a new Pension Credit claim as a couple until David also reaches State Pension age - under the "mixed-age couples" rule introduced in May 2019, David must claim Universal Credit instead if their household income is low enough to qualify. The IFS estimates this rule costs affected couples around £5,900 a year.

Practical step: model both incomes for the next three years together (Janet’s State Pension + any private pensions + David’s earnings or UC) so they don’t stumble into a tax-credit cliff or miss out on Council Tax Reduction, which they can still claim from their local council.

Situation: State Pension age was 66, reached in 2023, but she never got round to claiming.

Three things to check:

Backdating - she can backdate a claim by up to 12 months, so applying now captures payments from May 2025 onward.

Deferral uplift - for the months before that 12-month window she has been deferring; under the new State Pension this adds 1% for every nine weeks of deferral (~5.8% a year) for life. She has to choose between backdating (lump sum) and a higher weekly rate going forward - usually the higher weekly rate wins if she expects to live more than around 17 years.

Pension Credit gateway - once she claims, she becomes eligible to apply for Pension Credit if her income is below £227.10 a week (single, 2026/27). Even a £1 a week award unlocks council tax help, the Winter Fuel Payment and a free TV licence at 75.

What about 68?

Current legislation (the Pensions Act 2014 amending the Pensions Act 2007) moves State Pension age from 67 to 68 between 6 April 2044 and 5 April 2046. That timetable applies to people born from 6 April 1977 onward. In March 2023 the second independent review of State Pension age, led by Baroness Neville-Rolfe, recommended bringing this forward - she proposed a rise to 68 between 2041 and 2043, with a long-term principle of keeping people in retirement for "up to 31%" of adult life and capping State Pension spending at "up to 6% of GDP".

The government did not accept the Neville-Rolfe recommendation. Its 2023 report said the reviewer "was not able to take into account the long-term impact of recent significant external challenges, including the COVID-19 pandemic and recent global inflationary pressures", and that "the government does not intend to change the existing legislation prior to the conclusion of the next review". The next review is due "within two years of the next Parliament" - meaning by 2026-2027. As of today (May 2026) it has not reported, and the 2044-2046 timetable is what is on the statute book.

Practical reading: if you were born in the late 1970s or later, expect to plan around 68. If you were born in the 1980s, also plan for the possibility of 68 arriving a few years earlier than 2044, because future reviews can and do change the timetable. The age at which you can access a private pension (currently 55, rising to 57 in 2028) is a separate, earlier number you can rely on more.

Life expectancy at State Pension age

The ONS National Life Tables for 2022-2024 (published 10 December 2025) show how long people reaching State Pension age can expect to live on average.

At 67 - the State Pension age most people on this page will reach - the figure is roughly two years lower, so a woman reaching State Pension age in 2027 can on average expect to live another 19 years, a man another 16-and-a-half years. Half will live longer; a significant minority will live well past 90.

Two implications competitors gloss over. First, the "right" answer to "should I take my State Pension immediately or defer" depends partly on this number - deferral pays off if you live longer than around 17 years past your State Pension age, which is the average for women but a closer call for men. Second, healthy life expectancy (ONS data on years lived in "good" health) is materially lower than total life expectancy, which is why the 2023 review put weight on the proportion of adult life spent in retirement, not just the headline age.

State Pension age vs minimum pension age - don’t confuse them

These are two completely different numbers and people lose money by mixing them up:

- State Pension age - the earliest you can claim the State Pension. Set by Parliament. Depends on date of birth. Currently 66, rising to 67 by April 2028.

- Normal Minimum Pension Age (NMPA) - the earliest you can normally take money from a workplace or personal pension. Set by HMRC tax rules. Currently 55, rising to 57 from 6 April 2028. Affects people born on or after 6 April 1971 most.

People with a protected pension age under their scheme rules - common in older uniformed-services and some legacy pensions - may have a lower minimum age that is preserved through the 2028 change. HMRC's Pensions Tax Manual (PTM062100) sets out the protected pension age rules in detail. If you have any pension that pre-dates 6 April 2006, ask the scheme administrator whether you have a protected age before you do anything else.

Frequently asked questions

- Is the State Pension age 67 now?

- Not for everyone. The UK State Pension age is in the middle of a phased rise from 66 to 67, running from 6 April 2026 to 5 April 2028 under the Pensions Act 2014. If you were born before 6 April 1960 you reached State Pension age at 66. If you were born between 6 April 1960 and 5 March 1961 your age is somewhere between 66 years 1 month and 66 years 11 months, depending on your exact birth month. Anyone born from 6 March 1961 to 5 April 1977 has a State Pension age of 67.

- Can I retire before State Pension age?

- Yes. State Pension age is the earliest you can claim the State Pension, not the earliest you can stop work. You can normally access a workplace or personal pension from age 55, rising to 57 from 6 April 2028 (HMRC). You can also fund a gap year or two with ISAs, savings or part-time work. If ill health stops you working, look at New Style ESA, Universal Credit and Personal Independence Payment. None of these are reduced versions of the State Pension - they are separate benefits.

- Will the State Pension age rise to 68?

- Under current legislation (Pensions Act 2007) State Pension age rises from 67 to 68 between 6 April 2044 and 5 April 2046. The 2023 government review confirmed that timetable and chose not to bring it forward, despite Baroness Neville-Rolfe’s independent review recommending 2041-2043. The government said it will hold a further review "within two years of the next Parliament" to reconsider. So 68 is the planned age for anyone born from 6 April 1978, but the date it applies could move.

- Does State Pension age depend on my National Insurance record?

- No. State Pension age depends only on your date of birth. Your National Insurance record decides how much State Pension you actually get when you reach it. You normally need 10 qualifying years to get any new State Pension and around 35 years for the full new State Pension. You can check both your forecast and your NI record with the GOV.UK Check your State Pension forecast service. Filling NI gaps with voluntary Class 3 contributions can be one of the highest-return moves in UK personal finance.

- Do women have a different State Pension age?

- No, not any more. Women’s State Pension age was equalised with men’s at 65 by the Pensions Acts 1995 and 2011, completing in November 2018. Since then everyone has had the same State Pension age regardless of sex. Women born in the 1950s who were affected by the equalisation timetable have been the subject of the WASPI campaign and a Parliamentary Ombudsman finding on maladministration, but the underlying age rules are the same for men and women today.

- What if I was born on 5 April or 6 April?

- The legislated bands run from the 6th of one month to the 5th of the next, matching the UK tax year. If you were born on 5 April 1960 you fall just inside the "before 6 April 1960" group and reached State Pension age at 66. If you were born on 6 April 1960 you fall into the very first transitional band - State Pension age of 66 years and 1 month, which means you reach it on 6 May 2026. A one-day difference in birth date can move your claim date by a full month, so check the GOV.UK timetable carefully.

- What if my partner is older or younger than me?

- Each of you has your own State Pension age based on your own date of birth - you cannot pool them or claim on a spouse’s record under the new State Pension. The bigger issue is Pension Credit: since 15 May 2019, "mixed age couples" (one over State Pension age, one under) cannot start a new Pension Credit claim. The under-age partner must claim Universal Credit until they too reach State Pension age. The Institute for Fiscal Studies estimates this rule costs affected couples around £5,900 a year.

- Can the State Pension age change after I have reached it?

- No. Once you are entitled to the State Pension, that entitlement does not get withdrawn by a future timetable change. Reviews change the age future cohorts will reach, not the status of people already past it. The annual amount can still change - usually it rises each April under the triple lock - and the rules for deferral or backdating can be reformed, but your right to draw the State Pension itself is locked in once you cross your personal State Pension age.

- How do I check my exact State Pension date?

- Use the official GOV.UK "Check your State Pension age" tool. It tells you three things: when you will reach State Pension age, your Pension Credit qualifying age (the same date for almost everyone), and when you will be eligible for free bus travel (which differs by nation - England matches State Pension age, Scotland and Wales 60, Northern Ireland 60). Our calculator gives the same answer for the simple cases; the GOV.UK tool is the authoritative source for the exact transitional day.

- Does the State Pension start automatically on my birthday?

- No. You have to claim it. The Department for Work and Pensions writes to you about four months before you reach State Pension age with an invitation to claim online, by phone or by post. If you miss that invitation the pension does not start by itself - but you can backdate a claim by up to 12 months when you do apply. If you do nothing for longer, you are automatically deferring, which adds about 5.8% to your pension for every full year of deferral.