How State Pension deferral works in 2026/27

Deferring just means not claiming your State Pension on the day you reach State Pension age. You do not need to apply, fill in a form or tell anyone. GOV.UK puts it bluntly: "If you do not claim your State Pension at State Pension age, it automatically defers. You do not have to do anything." In exchange for waiting, the government adds an uplift to your weekly amount when you eventually claim, and that higher rate is paid for the rest of your life and rises each April with the triple lock.

The mechanics are very different depending on whether you reached State Pension age before or after 6 April 2016:

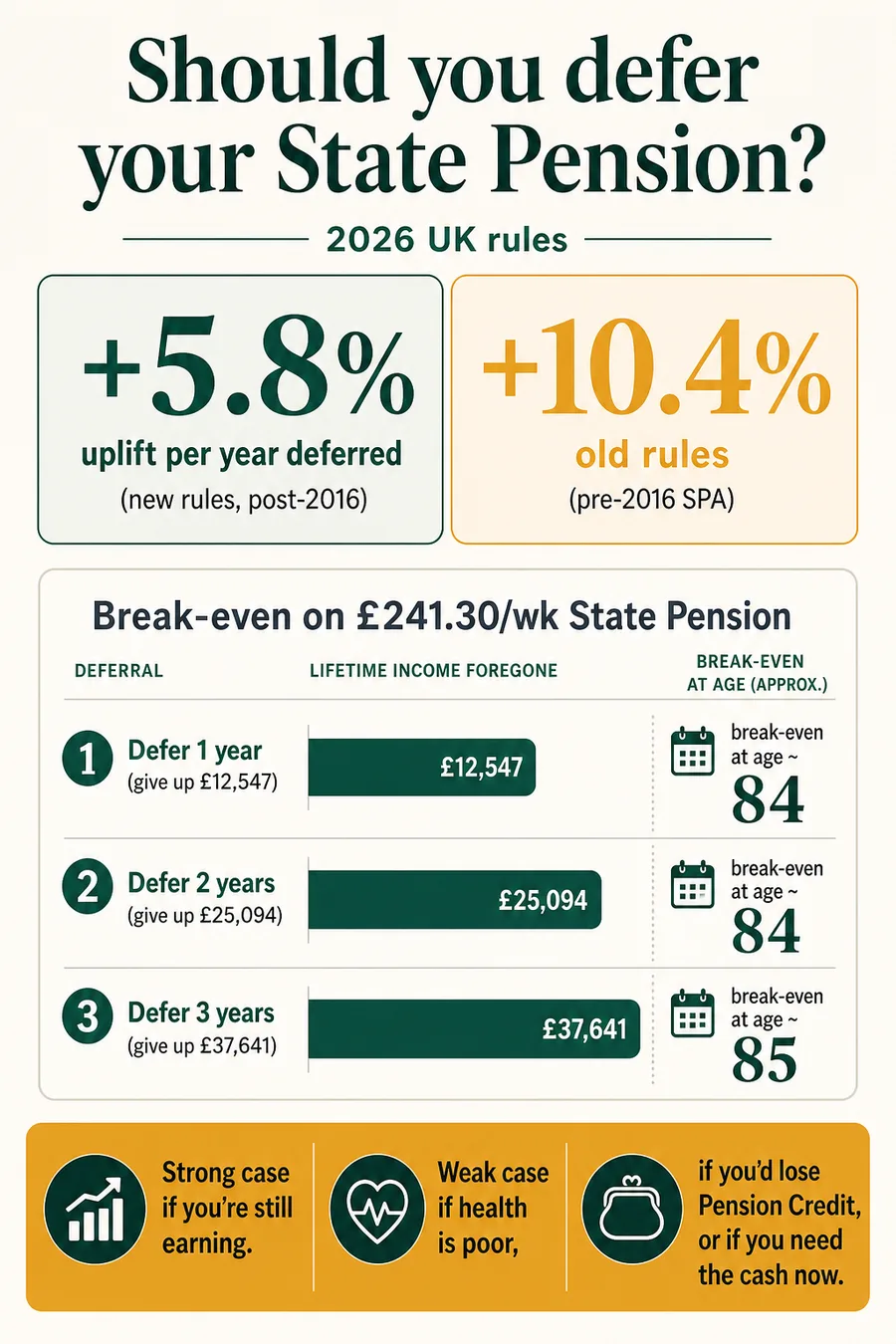

- New State Pension (SPA from 6 April 2016 onwards). You earn 1% extra for every 9 weeks you defer - just under 5.8% for a full year. You must defer for at least 9 weeks to get anything. There is no lump-sum option. You can only take the higher weekly amount.

- Old (basic) State Pension (SPA before 6 April 2016). You earn 1% extra for every 5 weeks deferred - 10.4% a year. You can take the deferred pension as a lump sum if you defer for at least 12 consecutive months. As the Low Incomes Tax Reform Group explains, the lump sum equals the deferred weekly pension plus compound interest at the Bank of England base rate + 2%.

On 2026/27 numbers, the new full State Pension of £241.30 a week (£12,547.60 a year) becomes around £255.24 a week after a year of deferral, £269.18 after two years, and £283.13 after three years - a roughly 17% uplift you keep for life, ratcheting up with the triple lock each April. You forgo a year, two years or three years of payments to get there.

Should you defer? A 30-second decision

Before the maths, sanity-check whether deferral is even the right question for you. The four branches below cover the situations where the answer is obvious one way or the other.

- 1 Already retired, no other income, claiming Pension Credit→ Don't defer - you'd lose more in benefits than you'd gain. Pension Credit, Housing Benefit and Council Tax Reduction treat you as having your State Pension already, so deferring earns no uplift and may cost you cash.

- 2 Still working, higher-rate taxpayer right now, expecting income to drop at 70+→ Strong case to defer - uplift is taken in retirement when you'll likely be a basic-rate taxpayer. The tax saving alone can shave years off the break-even point.

- 3 Reached SPA before 6 April 2016, want flexibility→ Old-rules lump sum option may suit you - uncommon but valuable. You can defer for 12 months and take the deferred pension as a single payment with interest at Bank rate + 2%.

- 4 Health condition or family history of shorter life expectancy→ Probably don't defer - you may not live long enough to break even. Claim as soon as you reach State Pension age.

The break-even table - full new State Pension, 2026/27

Worked from the confirmed 2026/27 figure of £241.30 a week (£12,547.60 a year). Uplift is calculated under the new rules: floor(weeks ÷ 9) × 1%, applied to the weekly base. Income foregone = weeks deferred × £241.30. "Tax-adjusted" break-even assumes you deferred while in higher-rate work (40%) and draw the uplift later as a basic-rate taxpayer (20%). Break-even ignores triple-lock rises, which apply equally to both options.

| Deferral period | Income foregone | Annual uplift after deferral | Break-even (years) | Break-even, tax-adjusted |

|---|---|---|---|---|

| 6 months | £6,274 | £251 (2.0%) | 25.0 | 18.7 |

| 1 year | £12,548 | £627 (5.0%) | 20.0 | 15.0 |

| 2 years | £25,095 | £1,380 (11.0%) | 18.2 | 13.6 |

| 3 years | £37,643 | £2,133 (17.0%) | 17.6 | 13.2 |

| 5 years | £62,979 | £3,639 (29.0%) | 17.3 | 13.0 |

Notice the gross break-even is essentially flat at around 17 years regardless of how long you defer. That is the point most general-audience pages miss: under the new rules deferral is a fixed-rate annuity - you are buying inflation-linked income at a yield of ~5.8%. The decision is not "how long should I defer", it is "do I expect to live more than 17 years past my State Pension age, and is the tax angle in my favour?".

Deferral break-even calculator

104 weeks · uplift = 11.0%

Assumes you draw the uplifted pension later as a basic-rate taxpayer.

If you live around 18.2 years past your State Pension age, deferring pays off.

That's roughly age 85 if you reach State Pension age at 67. On the 2022-2024 ONS National Life Tables, a 65-year-old woman has an average 21.2 years left and a man 18.7 - half of women, and just over half of men, beat that.

Approximate, before triple-lock effects. The uplifted pension and the foregone payments both rise each April, so the ratio is broadly stable. Always confirm with the official GOV.UK guide before deciding.

Three named scenarios

Situation: Has £30,000 a year from a final-salary pension and a paid-off mortgage. Doesn't need the State Pension cash.

Margaret considers deferring for three years, claiming at 69.

- Income foregone: 3 × £12,547.60 = £37,642.80. After 20% tax (her marginal rate sits comfortably in basic rate once stacked on her final-salary pension), the net amount she actually misses out on is roughly £30,114.

- Uplift: 156 weeks ÷ 9 = 17 whole 9-week blocks = 17%. £241.30 × 1.17 ≈ £282.32 a week, or about £14,680 a year. Annual uplift over the base: £2,132.

- Break-even: £37,643 ÷ £2,132 ≈ 17.7 years. She'd need to live to roughly 84 to break even on a gross basis. On the 2022-2024 National Life Tables, life expectancy at 66 for a woman is around 20 years - so on average she beats it, with some margin.

The catch: her surviving husband cannot inherit her new-State-Pension uplift on death. If she dies at 75, the family loses the full £30k of foregone income for just six years of uplifted payments. Deferral on the new rules is a single-life annuity.

Situation: Earning £55,000 in a job he likes. Plans to work to 69, defer State Pension while still in higher-rate work.

Tom reaches State Pension age at 67 in 2028. If he claims at 67 while still on his £55k salary, the State Pension stacks on top of his earnings and is taxed at 40%: from his £12,548 he keeps roughly £7,529.

- Defer for 2 years to age 69, when he plans to retire. Income foregone: £25,095. While he was higher-rate-taxed anyway, the net amount he misses out on is about £15,057 - the rest would have gone in tax.

- Uplift: 104 weeks ÷ 9 = 11 blocks = 11%. £241.30 × 1.11 = £267.84 a week. Annual uplift: £1,381. In retirement on basic-rate tax, he keeps £1,105 of that a year.

- Tax-adjusted break-even: £15,057 ÷ £1,105 ≈ 13.6 years - meaningfully better than the gross 17-year figure. Tom should expect to break even around age 83, which on current life tables is well below average life expectancy at 67.

This is the cleanest case for deferral: you swap a chunk of 40%-taxed income for the same money 20%-taxed, and you collect an inflation-linked uplift on top.

Situation: Already deferred for 18 months. Trying to choose between the higher weekly amount and the lump sum.

Diane is on the old basic State Pension. Her pre-deferral full rate was around £184.90 a week in 2026/27 (the current basic rate). For 78 weeks of deferral she has earned a 15.6% uplift (78 ÷ 5 = 15.6 × 1%).

- Option A - higher weekly: £184.90 × 1.156 ≈ £213.74 a week for life, an extra £1,500 a year.

- Option B - lump sum: Roughly £184.90 × 78 weeks + interest at Bank rate + 2% (Bank rate was 3.75% in May 2026 → ~5.75% effective). Approximate lump sum: £15,200, taxed at her highest marginal rate but crucially not pushing her into a higher band.

Pension Credit warning. Diane should check whether she qualifies for Pension Credit at her current weekly income. If she does, taking the lump sum could disqualify her in the year it's paid; taking the higher weekly amount may also disqualify her permanently. On the old rules the lump sum is the more common choice in normal Bank rate environments, because the higher weekly takes ~10 years to break even on a like-for-like basis. With Bank rate at 3.75%, the interest leg is unusually generous.

New rules vs old rules - side by side

| Feature | New rules (SPA from 6 April 2016) | Old rules (SPA before 6 April 2016) |

|---|---|---|

| Deferral rate | 1% per 9 weeks (~5.8% pa) | 1% per 5 weeks (~10.4% pa) |

| Minimum deferral period | 9 weeks | 5 weeks (12 months for lump sum) |

| Lump sum option | No - higher weekly only | Yes, with interest at Bank rate + 2% |

| Tax of lump sum | n/a | Marginal rate but doesn't push into a higher band |

| Pension Credit interaction | No accrual while you (or partner) claim PC | No accrual while you (or partner) claim PC |

| Surviving spouse inherits uplift? | No - single-life annuity | Yes - extra weekly amount or lump sum, subject to rules |

| Break-even (headline) | ~17.2 years (100 ÷ 5.8) | ~9.6 years (100 ÷ 10.4) |

Deferring while you carry on working

Most people who genuinely benefit from deferring are people who carry on earning past State Pension age. That changes the maths in three concrete ways, all of them in your favour:

- You stop paying National Insurance from your State Pension age - Class 1 if you are employed, Class 2 and Class 4 if you are self-employed - even if you keep working. That's an immediate ~8% pay rise on earnings between the primary threshold and the upper earnings limit. Your employer carries on paying employer's NI on your wages. Show your employer proof of age, or ask HMRC for a confirmation letter, so deductions stop on time.

- The State Pension stacks on top of your earnings at your highest marginal tax rate. On a £55,000 salary plus £12,548 State Pension, you push £5,118 of pension over the £50,270 higher-rate threshold and lose 40% of it to HMRC. Deferring means none of that pension is taxed at 40% during the working years, and the uplifted version is taxed at 20% once you stop work.

- Bigger pension contribution headroom. Wages count as relevant earnings for pension tax relief; State Pension does not. Drawing it earlier doesn't expand your relief cap; deferring keeps your earnings clean for SIPP or workplace contributions.

The trade-off is liquidity. If you're foregoing £12,548 a year of after-tax-at-20% income later in life so you can earn 5.8% more on it forever, the implicit cost is genuine - that money is not available for emergencies, large repairs or a year of long-term care fees. If your post-SPA work is patchy or insecure, the case for deferral weakens regardless of the tax angle.

Deferral vs buying voluntary NI years

People sometimes ask whether they should defer or, instead, plug NI gaps with voluntary Class 3 contributions. They are not really competing - they apply at different points in your life - but the comparison is worth doing because both move the same number on your forecast.

- Voluntary Class 3 (£18.40/week, £956.80/year in 2026/27): buys 1/35th of the full new State Pension per year, currently £358.50 a year of extra income for life. Break-even ≈ 2.7 years from State Pension age.

- Deferral (~5.8% pa under the new rules): buys roughly £725 a year of extra income on the full base, in exchange for foregoing a full year of payments (£12,548). Break-even ≈ 17 years.

Voluntary contributions are one of the highest-return moves in UK personal finance because the denominator (£957) is small. Deferral is a much bigger bet because the denominator (a full year of foregone pension) is much larger. If you have NI gaps to fill, fill them first; defer only after you've maxed your forecast to £241.30 a week.

When deferring is a bad idea

- You currently claim or could claim Pension Credit. You accrue no deferral uplift while you, or your partner, are receiving Pension Credit, Housing Benefit, Universal Credit, Income Support or Carer's Allowance. Worse, Pension Credit treats you as if you were drawing the State Pension already, so deferral doesn't even boost your PC award.

- You have health conditions that may shorten life expectancy. Break-even is ~17 years on the new rules. If life expectancy is materially below average, that 17% uplift may never pay back the 3 years of payments you skipped.

- You need the cash flow for day-to-day living. Forgoing £12,548 a year is real money. Drawing it down from an ISA, SIPP or savings to fund the gap usually kills the deferral case.

- You'd lose passported benefits like Council Tax Reduction. A higher income later can disqualify you from means-tested help in retirement that you'd otherwise have been entitled to.

- You're worried about leaving income to a surviving spouse. Under the new State Pension, deferral is a single-life annuity. If you die soon after claiming, the family loses both the foregone payments and the uplift.

How to defer - practical steps

- Don't claim. The Department for Work and Pensions writes to you about four months before your State Pension age with an invitation to claim. Ignoring the letter (or actively choosing not to claim) is how you defer - there is no separate deferral form.

- To start drawing later, make a claim through gov.uk/get-state-pension, by phone on the State Pension claim line (0800 731 7898), or by post.

- Backdating: you can backdate a claim by up to 12 months on the new rules. The backdated payment is a single arrears amount with no interest, and it reduces the ongoing uplift accordingly. You usually have to choose between backdating and keeping the full deferred weekly rate going forward.

- One window. Once you start drawing, you cannot stop and re-defer on the new rules. You get a single deferral window per entitlement.

- National Insurance: you stop paying Class 1, 2 and 4 NI from the day you reach State Pension age regardless of whether you claim - confirm with your employer and show proof of age so they stop deducting it.

Life expectancy reality check

The "break-even" maths only makes sense set against how long you can actually expect to live. The most recent ONS National Life Tables (2022-2024), published 10 December 2025, put life expectancy at age 65 at 21.2 years for women and 18.7 years for men in the UK. At State Pension age 67 the figures are roughly two years lower - call it ~19.4 years for a woman and ~16.9 years for a man.

Two practical implications. First, for a woman the average outcome comfortably beats new-rules break-even; for a man it's close to the line, with tax angle often being the deciding factor. Second, half of people will live past the average, sometimes well past - so deferral is also a hedge against living a long time, which (along with very long-term care costs) is one of the bigger risks in UK retirement planning.

Frequently asked questions

Frequently asked questions

- Is deferring my State Pension worth it?

- Maths-only, it pays off if you live around 17 years past State Pension age on the new rules (~10 years on the pre-2016 rules). On the 2022-2024 ONS National Life Tables a 65-year-old woman has 21.2 years left on average and a man 18.7 - so the average woman beats break-even with a margin, the average man only just does. But personal factors swing it: claim Pension Credit and you cannot accrue a deferral uplift; pay 40% tax now and 20% later, deferral gets materially better; have a health condition and it gets worse.

- How much extra do I get if I defer my State Pension?

- Under the new State Pension your weekly amount goes up by 1% for every 9 weeks you defer - just under 5.8% for a full year. On the 2026/27 full new State Pension of £241.30 a week, a year of deferral adds about £13.94 a week for life (~£725 a year) and three years adds about 17%. There is no lump-sum option on the new rules. If you reached State Pension age before 6 April 2016 the rate is much higher: 1% for every 5 weeks deferred, ~10.4% a year.

- Can I take my deferred State Pension as a lump sum?

- Only if you reached State Pension age before 6 April 2016 and you defer for at least 12 consecutive months. The lump sum is the deferred weekly pension plus interest, compounded weekly at the Bank of England base rate plus 2%. People on the new State Pension - anyone who reached SPA on or after 6 April 2016 - cannot choose a lump sum. They can only take the higher weekly amount. A backdated single payment of up to 12 months is sometimes called a "lump sum" by claimants, but it accrues no interest and reduces your ongoing deferred uplift.

- Does deferring my State Pension affect Pension Credit?

- Yes - and in a way that usually kills the case for deferral. If you, or your partner, claim Pension Credit, Housing Benefit, Universal Credit, Income Support or several other means-tested benefits, you do not accrue any extra State Pension for the weeks those benefits are in payment. Worse: Pension Credit treats you as if you were receiving your State Pension even while you defer, so deferring does not boost your Pension Credit award. If you are anywhere near Pension Credit territory, claim rather than defer.

- How long does it take to break even on a deferred State Pension?

- On the new rules, the headline break-even is about 17.2 years of higher payments - calculated as 100 ÷ 5.8 = 17.24. If you defer for one year, you forgo £12,548 in 2026/27 and gain about £725 a year for life; £12,548 / £725 ≈ 17.3 years. The maths is the same whether you defer 1 year or 5 - break-even depends on the percentage uplift, not the length of deferral. Tax can shift this materially: deferring while higher-rate-taxed and drawing later at basic rate cuts break-even closer to 12 years.

- Can I keep working past State Pension age without deferring?

- Yes. State Pension age, claim date and retirement are three separate things. You can claim your State Pension and carry on working - the State Pension is paid in addition to your wages, and is taxable. You can also work and defer - the default if you do nothing is automatic deferral. Many people do this for a year or two to avoid a chunk of higher-rate tax: while still earning £55,000+, the State Pension would be taxed at 40%; deferring it and claiming at 70, when wages have stopped, taxes it at 20% (and adds the deferral uplift on top).

- Do I pay National Insurance after State Pension age?

- No - not as an employee or self-employed person. You stop paying Class 1 (employee), Class 2 (self-employed) and Class 4 National Insurance from the day you reach State Pension age, whether you claim the State Pension or defer it. You may need to show your employer proof of age (passport or birth certificate) to make sure they stop deducting NI; if you would rather not, HMRC will send you a letter to give them instead. Your employer still pays employer NI on your wages even after you reach SPA. Voluntary Class 3 contributions can still be made after SPA to fill earlier gaps if those gaps will improve your forecast.

- Will my surviving spouse inherit my higher deferred State Pension?

- On the new State Pension (you reached SPA on or after 6 April 2016) your surviving spouse or civil partner cannot inherit your standard new State Pension or the deferral uplift on it. They can inherit half of any "protected payment" from your pre-2016 Additional State Pension. On the old basic State Pension, the rules are more generous: a surviving spouse can inherit extra State Pension built up through deferral, and if you deferred for at least 12 months and died before claiming, they can usually choose between a weekly inheritance or a lump sum. This is one of the biggest hidden risks of deferring on the new rules.

- Can I change my mind after I start deferring?

- Yes, at any point. There is no formal "deferral" application - you defer simply by not claiming. To start drawing your State Pension you make a claim through GOV.UK, by phone (0800 731 7898) or by post. You can also backdate a claim by up to 12 months: choose between (a) the higher deferred weekly rate going forward, or (b) a single backdated payment covering up to 12 months and a smaller ongoing uplift. Once you claim, you cannot go back into deferral on the same entitlement - under the new rules each person gets one window.

- Is the deferred State Pension taxed?

- Yes. The higher weekly amount is taxable as income in the same way as a normal State Pension - paid gross, with HMRC adjusting your tax code on other PAYE income to collect it. On the old-rules lump sum option, special tax treatment applies: the lump sum is taxed at the highest marginal rate that applies to your other income that tax year, but does not itself push you into a higher band. Quoting LITRG: "A deferred state pension lump sum will not be added to any other income … you will not be pushed into a higher tax bracket as a result of taking the lump sum."