What Pension Credit actually is

Pension Credit is a means-tested benefit administered by the Department for Work and Pensions that tops up the weekly income of people over State Pension age. It is the safety-net benefit for pensioners - the rough equivalent of Universal Credit for working-age adults - and it sits alongside, not instead of, the State Pension. It pays directly into your bank account, is not taxable, and once awarded it usually continues automatically as long as your circumstances stay the same.

There are two elements. Guarantee Credit is the main one: it lifts your weekly income to a minimum level set by Parliament each April. Savings Credit is a small legacy top-up worth up to about £18 a week, only available to people who reached State Pension age before 6 April 2016. Most new claimants only see the Guarantee element.

The single most powerful feature of Pension Credit, however, is not the money itself but the passporting mechanism: an award of even £1 a week of Guarantee Credit unlocks a chain of other benefits that together are typically worth £2,000-£3,500 a year. Skip to the gateway-benefits table if that is the part you came for.

Could you qualify? A 60-second decision tree

The Pension Credit calculation is more generous than most people assume. Work through these four questions before you write yourself off:

- 1 Are you over State Pension age?→ If yes, continue. If you are in a couple and your partner is under SPA, see the mixed-age couples rule - you may need to claim Universal Credit instead.

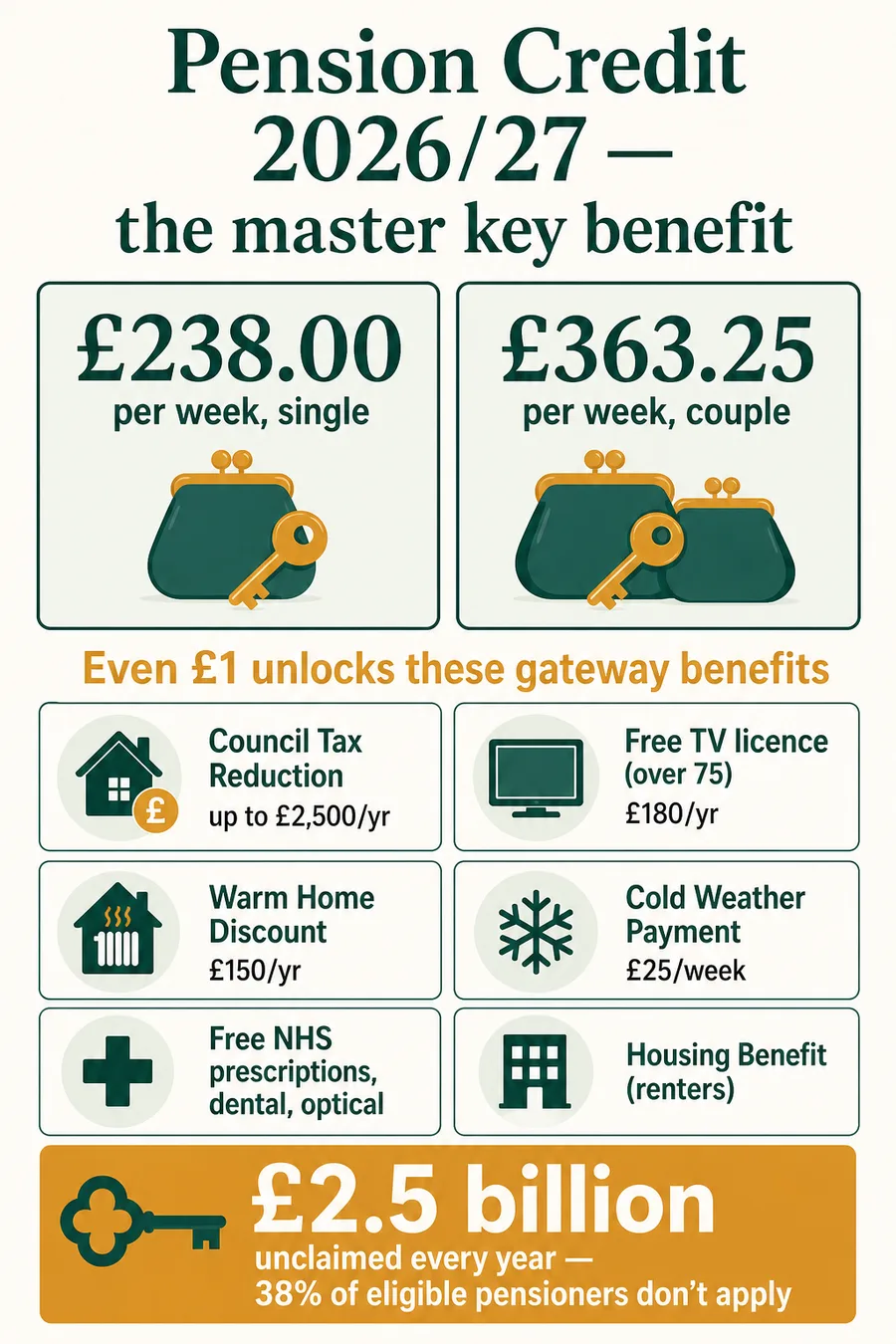

- 2 Is your weekly income below £238 (single) or £363.25 (couple)?→ Income includes State Pension, private pensions, earnings, and most other benefits - but not Attendance Allowance, PIP, DLA, Housing Benefit or the first £10 of a War Widow’s pension. If yes, you are very likely to qualify for some Pension Credit.

- 3 Even if income is slightly above the threshold:→ if you receive Attendance Allowance, PIP daily living, are a carer, or have housing costs, additional amounts can lift your "applicable" minimum above the headline figure - so apply anyway.

- 4 What about savings?→ the first £10,000 is ignored. Above £10,000, you are treated as having £1 of weekly income per full or part £500. There is no upper capital limit - even with £50,000 in savings, you might still qualify if your income is low enough.

Rule of thumb: if your weekly income (excluding disability benefits) is anywhere within about £30/week of the threshold, apply. The official GOV.UK Pension Credit calculator gives the definitive answer, and the calculator below gives you a fast first check.

Pension Credit quick-check calculator

Enter your weekly income, savings and whether you are single or in a couple. The calculator applies the 2026/27 Guarantee Credit figures and the £10,000 capital disregard. This is a rough estimate - it does not include additional amounts for severe disability, carers or housing costs, which can increase your entitlement.

Roughly £12,376.00 a year in Pension Credit - and you would also likely qualify for:

- Council Tax Reduction (often a full discount)

- Free NHS dental treatment, eye tests and prescriptions

- Warm Home Discount (£150)

- Free TV licence if anyone in the household is aged 75 or over

- Cold Weather Payments

- Christmas Bonus (£10)

- Possibly full Housing Benefit if you rent

Estimate only. Apply at gov.uk/pension-credit to find out for certain.

The 2026/27 rates in detail

Guarantee Credit - Standard Minimum Guarantee

- Single: £238.00/week (up from £227.10 in 2025/26)

- Couple: £363.25/week (up from £346.60 in 2025/26)

These figures rise by 4.8% in April 2026, in line with the earnings element of the "triple lock" used for State Pension uprating. Confirmed in the Statutory Review of State Pension and Benefit Rates 2026/27 and the DWP's Benefit and pension rates 2026/27.

Savings Credit (legacy element)

Only people who reached State Pension age before 6 April 2016 can claim Savings Credit. For 2026/27:

- Savings Credit threshold: £208.07/week single, £329.75/week couple

- Maximum Savings Credit: £17.96/week single, £20.10/week couple

The mechanic: for every £1 of qualifying income above the threshold, you receive 60p of Savings Credit, up to the cap. It is gradually being phased out as the eligible cohort ages.

Additional amounts

- Severe disability addition: £86.05/week (single rate) or £172.10/week (couple rate, where both qualify). Available if you receive AA, PIP daily living, DLA care (middle or high rate) or ADP, nobody is paid Carer's Allowance for looking after you, and you live alone (or no non-dependent adult lives with you).

- Carer addition: £48.15/week. Available if you have an underlying entitlement to Carer's Allowance - even if you are not paid it because your State Pension is higher.

- Housing costs: ground rent, certain service charges, site rents for park homes can be included. Mortgage interest is no longer covered through Pension Credit; you would need the separate Support for Mortgage Interest (SMI) loan.

Capital and savings rules

The capital rules are the same whether you are single or in a couple - there is one £10,000 disregard for the household, not £10,000 each. This is one of the most misunderstood points of the Pension Credit rules, and the main reason couples with shared ISAs walk away thinking they are not eligible when in fact they are. Above the disregard:

- Every £500 (or part of £500) of capital generates £1/week of deemed income.

- £15,000 → £10/week deemed. £20,000 → £20/week deemed. £30,000 → £40/week deemed.

- No upper capital limit - unlike Universal Credit, there is no £16,000 cliff.

- "Capital" includes cash, current accounts, savings accounts, ISAs, premium bonds, NS&I products, shares, fund holdings, and most investments. It does not include the home you live in, personal possessions, the surrender value of life-insurance policies, or (crucially) a pension pot you have not yet started to draw.

That last point matters: if you have a defined-contribution pension worth £40,000 that you have not yet touched, the capital is ignored entirely. The DWP only treats it as income if you draw it, or - if you are over SPA and could draw it but don't - it can be treated as "notional income" at the level you could reasonably take. In practice, leaving a pot untouched while claiming Pension Credit is permitted and common.

For more worked examples see our companion guide on Pension Credit and savings.

The gateway: what £1 of Pension Credit unlocks

This is the single most important fact about Pension Credit, and the reason almost everyone potentially eligible should apply: a successful claim for even £1/week of Guarantee Credit passports you to a chain of other benefits that are often worth more than the Pension Credit itself.

| Gateway benefit | Approx. annual cash value (2026/27) |

|---|---|

| Council Tax Reduction (often full discount) | £1,500-£2,500+ |

| Full Housing Benefit (if you rent) | Up to local rent in full |

| Free NHS dental treatment, eye tests, prescriptions, wigs & fabric supports | £200-£600 (varies) |

| Free TV licence (household with someone aged 75+) | £180 (from 1 April 2026) |

| Warm Home Discount (Core Group 1) | £150 |

| Cold Weather Payment (per qualifying week) | £25 per spell of cold weather |

| Christmas Bonus | £10 (one-off, but everyone gets it) |

| Carer's Allowance underlying entitlement (for someone caring for you) | Up to £4,331/yr for the carer |

| Typical household total (excluding Housing Benefit) | ~£2,000-£3,500/year on top of Pension Credit |

Note: from 2025/26 the Winter Fuel Payment was restored to a near-universal basis for pensioner households (recovered through the tax system above £35,000 of taxable income), so it is no longer strictly "unlocked" by Pension Credit - but Pension Credit remains the most reliable gateway in case eligibility narrows again. See the GOV.UK Winter Fuel Payment page for the current rules.

Three worked examples

Situation: Lives alone in a flat she owns. She has £180/week of State Pension and no private pension or savings.

- Assessed income: £180/week

- Guarantee Credit top-up: £238.00 − £180 = £58/week (about £3,016/year)

- Passports to: Council Tax Reduction (probably full), free NHS dental and eye tests, Warm Home Discount £150, free TV licence (over 75? not yet - she gets it from age 75), Christmas Bonus.

- Total annual gain: ~£4,500-£5,500 once gateway benefits are included.

Situation: Between them they receive £350/week of State Pension (£200 + £150). They hold £18,000 in a cash ISA.

- Deemed income from savings: £18,000 − £10,000 = £8,000 → £8,000 ÷ £500 = £16/week

- Assessed income: £350 + £16 = £366/week

- Guarantee Credit top-up: £363.25 − £366 = £0 (£2.75 above the headline minimum)

- But: if either receives Attendance Allowance, the severe disability addition of £86.05/week lifts their applicable minimum to £449.30/week, producing ~£83/week of Pension Credit and passporting them to full Council Tax Reduction and the rest of the gateway. The lesson: don't stop at the headline figure.

Situation: Bill (67) and Carol (64) have State Pension of £180/week (Bill only) and Carol has small earnings of £80/week. Under the pre-2019 rules they could have claimed Pension Credit as a couple. Since 15 May 2019 they cannot.

- They must claim Universal Credit instead, where the couple standard allowance is much lower than Pension Credit's £363.25/week minimum - a gap of roughly £140/week, or around £7,000/year.

- If they were already claiming Pension Credit as a mixed-age couple before 15 May 2019 they may be on transitional protection. New claims are not allowed.

- They should re-check Pension Credit on the day Carol reaches SPA - the application will need to be made fresh.

For more on the trap see Independent Age's briefing.

What counts as income, and what does not

The means test compares your assessed weekly income against the Standard Minimum Guarantee. Not everything counts. Here is the working list:

- Counts as income: State Pension (including any deferred amount you could have drawn), private/occupational pensions, earnings (after tax/NI and allowable disregards), most social security benefits, certain regular charitable payments, deemed income from capital above £10,000, maintenance payments, and rental income net of allowable expenses.

- Does NOT count as income: Attendance Allowance, Personal Independence Payment (both components), Disability Living Allowance care/mobility, Adult Disability Payment, Armed Forces Independence Payment, Christmas Bonus, Winter Fuel Payment, Cold Weather Payments, Housing Benefit, social fund payments, the first £10 of certain War Widow(er)'s pensions, and most one-off lottery/gambling winnings (which become capital instead).

The list of disregarded benefits is the reason so many disabled pensioners qualify even with seemingly "high" headline income. £100/week of Attendance Allowance disappears completely from the income test - but each AA claim simultaneously creates entitlement to the severe disability addition, so the maths tilts twice in the claimant's favour.

The underclaimed billions

The DWP's most recent Income-related benefits: estimates of take-up release (financial year ending 2024, published 2025) is sobering:

- 62% caseload take-up - down from 65% a year earlier.

- 71% expenditure take-up - down from 78% a year earlier.

- Up to 910,000 families entitled to Pension Credit are not claiming.

- Around £2.5 billion of Pension Credit is going unclaimed each year.

- Average loss per non-claimant household: £2,600/year - before gateways.

If there is any doubt at all, apply. The official GOV.UK calculator takes 5 minutes, or call 0800 99 1234 - the call is free.

The reasons people don't claim are well documented: they assume they earn too much, are put off by the means test, don't realise they qualify with savings, or simply find the application daunting. None of these reasons is a good reason. If you are unsure, use the official calculator or call 0800 99 1234. The call is free; the calculator takes 5 minutes.

Two facts most often quoted in the press deserve scepticism. The first is that "1 in 3 eligible pensioners don't claim" - true for the caseload measure but the expenditure measure is 29%, suggesting non-claimants miss out on smaller amounts on average than claimants receive. The second is the headline "£3 billion unclaimed" figure that appeared in coverage in late 2024; the DWP's own central estimate is now closer to £2.5 billion for FYE 2024, with a wide confidence band. Either way, the policy direction is clear: take-up has gone backwards in the last two years, not forward, despite government campaigns. That is partly because the cost-of- living one-off Pension Credit boosts attracted claims that were not then renewed.

How to apply - three routes

There are three routes: online at gov.uk (fastest if you already get State Pension), by phone on 0800 99 1234 (Mon-Fri 8am-6pm - staff complete the form for you), or in person with help from Citizens Advice, Age UK or Independent Age. Backdating of up to three months is automatic where you were entitled.

1. Online (fastest)

Apply at gov.uk/pension-credit/how-to-claim. You can apply online if you already receive a State Pension and your claim does not include children. You will need your National Insurance number, bank/building society details, income details, and a summary of your savings.

2. By phone

Call the Pension Credit claim line on 0800 99 1234, Monday to Friday 8am-6pm. Staff fill in the form for you over the phone - this is the most popular route for first-time claimants. Have your NI number, partner's details, pension and savings figures ready. Use Relay UK 18001 then 0800 99 1234 if you cannot hear or speak on the phone.

3. With help from a charity

Citizens Advice, Age UK and Independent Age all offer free help to complete a claim. Their advisers know the rules far better than the average online form and routinely uncover entitlement that people had dismissed.

Backdating

Successful claims can be backdated by up to three months, provided you were entitled during that period. Apply now even if you only think you might qualify - a delay of three months means the back end of the backdating window starts to fall off.

What can go wrong

Deemed income mistakes on the application

The most common rejection is people declaring savings income as actual earned interest rather than letting the DWP apply the deemed-income rule (£1 per £500 above £10,000). If you write down the actual interest your ISA paid, the DWP will use the higher deemed figure anyway - but if you fail to declare the capital itself, the claim can be reassessed later with a penalty for non-disclosure.

Pension Credit is a "passported" benefit, which means HMRC and DWP cross-check. If your savings rise above the £10,000 threshold and you don't tell the DWP, you can be overpaid for months before being landed with a recovery demand. Report any change of £500 or more.

Mixed-age couple confusion

If your partner is under State Pension age, you cannot start a new Pension Credit claim - you must claim Universal Credit. People who try to claim Pension Credit anyway are routinely rejected, then assume they aren't entitled to anything. UC eligibility is separate; check it via gov.uk/universal-credit.

State Pension age timetable and Pension Credit

Since 15 May 2019, a couple where one partner is under State Pension age cannot start a new Pension Credit claim. The household must claim Universal Credit instead - which pays roughly £7,000/year less for a couple in this situation. Pre-2019 claimants may have transitional protection, but any break in the claim is usually final.

You can only claim Pension Credit once you reach State Pension age (the rules also require both members of a couple to be over SPA - see above). The SPA is currently 66 but rises in stages between April 2026 and April 2028 to 67. People born between 6 April 1960 and 5 March 1961 reach SPA at 66-and-a-handful-of-months; people born from 6 March 1961 onwards reach it at 67.

For some people this delays Pension Credit eligibility by up to 12 months. If your income is low during that gap, check Universal Credit instead - it can bridge the period until you reach SPA. See our full State Pension age timetable guide.

Frequently asked questions

- What is the income limit for Pension Credit in 2026/27?

- For 2026/27, Guarantee Credit tops your weekly income up to £238.00 if you are single and £363.25 if you are part of a couple. If your weekly income is below those figures, you are likely to qualify for some Pension Credit. The test is more generous than it looks because deemed income from savings under £10,000 is zero, and some pension contributions and disability benefits do not count as income. Apply even if you are slightly above - the calculation is rarely what people expect.

- Can I get Pension Credit if I have savings?

- Yes. The first £10,000 of savings, ISAs and investments is ignored entirely. Above £10,000, every full or part £500 is treated as giving you £1 per week of "deemed income". So £20,000 in savings gives you £20 a week of deemed income - not zero, but nowhere near what the savings actually represent. There is no upper savings cap for Pension Credit, unlike some other means-tested benefits.

- Is Pension Credit means tested?

- Yes. Pension Credit is means tested on your income (from State Pension, private pensions, earnings and most benefits) and your capital (savings, investments, ISAs, premium bonds). Your main home, personal possessions and the value of any pension pot you have not yet drawn are ignored. Some income - including Attendance Allowance, PIP, DLA and Housing Benefit - is fully disregarded for the means test.

- How long does Pension Credit take to come through?

- DWP aims to process new Pension Credit claims within around 6 to 8 weeks, although straightforward online applications are sometimes faster. Your first payment usually includes any backdated entitlement (up to three months) as a lump sum. If you are claiming to unlock Winter Fuel Payment, get your application in well before the qualifying week each September.

- Can I claim Pension Credit and the State Pension at the same time?

- Yes - and most people who get Pension Credit also receive a State Pension. Pension Credit is designed to top up low State Pension income. Your State Pension counts as income for the means test, but it does not stop you claiming. If you defer your State Pension, the DWP will still treat you as having the income you would have received, so deferring does not get you more Pension Credit.

- What is the difference between Guarantee Credit and Savings Credit?

- Guarantee Credit is the main element of Pension Credit. It tops everyone over State Pension age up to the minimum income level (£238/week single, £363.25/week couple in 2026/27). Savings Credit is a small extra payment of up to £17.96/week (single) or £20.10/week (couple) for people who reached State Pension age before 6 April 2016 and have modest income above the Savings Credit threshold of £208.07/week (single) or £329.75/week (couple). Anyone who reached SPA after that date cannot claim Savings Credit.

- Is Pension Credit backdated?

- Yes. Pension Credit can be backdated by up to three months, provided you were entitled during that period. That means a successful claim can result in a one-off lump sum worth several hundred pounds before your weekly payments start. If you think you might have been entitled for a while, apply now - every day you delay risks losing entitlement at the back end of that three-month window.

- Can I claim Pension Credit if I own my home?

- Yes. Home-ownership has no effect on Pension Credit. The value of the property you live in is not counted as capital. You may even get an additional amount for housing costs such as service charges or ground rent, although mortgage interest is no longer covered (the Support for Mortgage Interest loan scheme replaced that). Many homeowners with a small private pension are eligible and never claim.

- Does Pension Credit affect my partner if they are under State Pension age?

- Since 15 May 2019, mixed-age couples (where one partner is over State Pension age and one is under) cannot make a new Pension Credit claim until both reach SPA. The younger partner must instead claim Universal Credit for the household, which pays far less. This rule has been criticised for costing affected couples up to roughly £7,000 a year. If you were already claiming Pension Credit before 15 May 2019 you may keep it under transitional protection.

- How much could I be missing out on?

- The DWP estimates around 910,000 households entitled to Pension Credit do not claim it, leaving up to £2.5 billion unclaimed each year (FYE 2024 statistics). The average non-claimant is missing roughly £2,600 a year - and that is before counting gateway benefits like Council Tax Reduction, free TV licence for over-75s and the Warm Home Discount, which can add another £1,500 to £3,000 of value annually.